McDonalds 2010 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2010 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

statements on a recurring basis (i.e., at least annually). The

Company adopted the required provisions related to debt and

derivatives as of January 1, 2008 and adopted the remaining

required provisions for non-financial assets and liabilities as of

January 1, 2009. The effect of adoption was not significant in

either period.

• Variable interest entities and consolidation

In June 2009, the FASB issued amendments to the guidance on

variable interest entities and consolidation, codified primarily in

the Consolidation Topic of the FASB ASC. This guidance modi-

fies the method for determining whether an entity is a variable

interest entity as well as the methods permitted for determining

the primary beneficiary of a variable interest entity. In addition,

this guidance requires ongoing reassessments of whether a

company is the primary beneficiary of a variable interest entity

and enhanced disclosures related to a company’s involvement

with a variable interest entity. The Company adopted this guid-

ance as of January 1, 2010.

On an ongoing basis, the Company evaluates its business

relationships such as those with franchisees, joint venture part-

ners, developmental licensees, suppliers, and advertising

cooperatives to identify potential variable interest entities. Gen-

erally, these businesses qualify for a scope exception under the

consolidation guidance. The Company has concluded that con-

solidation of any such entities is not appropriate for the periods

presented. As a result, the adoption did not have any impact on

the Company’s consolidated financial statements.

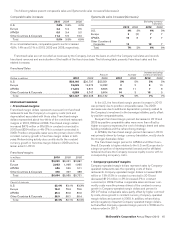

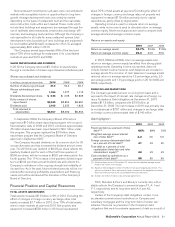

Cash Flows

The Company generates significant cash from its operations and

has substantial credit availability and capacity to fund operating

and discretionary spending such as capital expenditures, debt

repayments, dividends and share repurchases.

Cash provided by operations totaled $6.3 billion and

exceeded capital expenditures by $4.2 billion in 2010, while cash

provided by operations totaled $5.8 billion and exceeded capital

expenditures by $3.8 billion in 2009. In 2010, cash provided by

operations increased $591 million or 10% compared with 2009

primarily due to increased operating results. In 2009, cash pro-

vided by operations decreased $166 million or 3% compared

with 2008 despite increased operating results, primarily due to

higher income tax payments, higher noncash income items and

the receipt of $143 million in 2008 related to the completion of

an IRS examination.

Cash used for investing activities totaled $2.1 billion in 2010,

an increase of $401 million compared with 2009. This reflects

higher capital expenditures and lower proceeds from sales of

investments and restaurant businesses. Cash used for investing

activities totaled $1.7 billion in 2009, an increase of $31 million

compared with 2008. This reflects lower proceeds from sales of

investments, restaurant businesses and property, offset by lower

capital expenditures, primarily in the U.S.

Cash used for financing activities totaled $3.7 billion in 2010,

a decrease of $692 million compared with 2009, primarily due to

higher net debt issuances, higher proceeds from stock option

exercises and lower treasury stock purchases, partly offset by an

increase in the common stock dividend. Cash used for financing

activities totaled $4.4 billion in 2009, an increase of $307 million

compared with 2008, primarily due to lower net debt issuances,

an increase in the common stock dividend and lower proceeds

from stock option exercises, partly offset by lower treasury stock

purchases.

As a result of the above activity, the Company’s cash and

equivalents balance increased $591 million in 2010 to $2.4 bil-

lion, compared with a decrease of $267 million in 2009. In

addition to cash and equivalents on hand and cash provided by

operations, the Company can meet short-term funding needs

through its continued access to commercial paper borrowings

and line of credit agreements.

RESTAURANT DEVELOPMENT AND CAPITAL EXPENDITURES

In 2010, the Company opened 957 traditional restaurants and

35 satellite restaurants (small, limited-menu restaurants for which

the land and building are generally leased), and closed 406 tradi-

tional restaurants and 327 satellite restaurants. Of these

closures, there were over 400 in McDonald’s Japan due to the

strategic review of the market’s restaurant portfolio. In 2009, the

Company opened 824 traditional restaurants and 44 satellite

restaurants and closed 215 traditional restaurants and 142 satel-

lite restaurants. The majority of restaurant openings and closings

occurred in the major markets in both years. The Company closes

restaurants for a variety of reasons, such as existing sales and

profit performance or loss of real estate tenure.

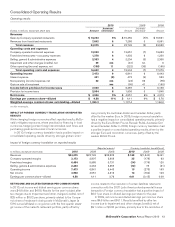

Systemwide restaurants at year end(1)

2010 2009 2008

U.S. 14,027 13,980 13,918

Europe 6,969 6,785 6,628

APMEA 8,424 8,488 8,255

Other Countries & Corporate 3,317 3,225 3,166

Total 32,737 32,478 31,967

(1) Includes satellite units at December 31, 2010, 2009 and 2008 as follows: U.S. –

1,112, 1,155, 1,169; Europe–239, 241, 226; APMEA (primarily Japan)–1,010,

1,263, 1,379; Other Countries & Corporate–470, 464, 447.

Approximately 65% of Company-operated restaurants and

about 80% of franchised restaurants were located in the major

markets at the end of 2010. About 80% of the restaurants at

year-end 2010 were franchised.

Capital expenditures increased $183 million or 9% in 2010

primarily due to higher investment in new restaurants. Capital

expenditures decreased $184 million or 9% in 2009 primarily

due to fewer restaurant openings, lower reinvestment in existing

restaurants in the U.S. and the impact of foreign currency trans-

lation. In both years, capital expenditures reflected the Company’s

commitment to grow sales at existing restaurants, including

reinvestment initiatives such as reimaging in many markets

around the world.

Capital expenditures invested in major markets, excluding

Japan, represented over 65% of the total in 2010, 2009 and

2008. Japan is accounted for under the equity method, and

accordingly its capital expenditures are not included in con-

solidated amounts.

Capital expenditures

In millions 2010 2009 2008

New restaurants $ 968 $ 809 $ 897

Existing restaurants 1,089 1,070 1,152

Other(1) 78 73 87

Total capital

expenditures $ 2,135 $ 1,952 $ 2,136

Total assets $31,975 $30,225 $28,462

(1) Primarily corporate equipment and other office-related expenditures.

20 McDonald’s Corporation Annual Report 2010