McDonalds 2010 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2010 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

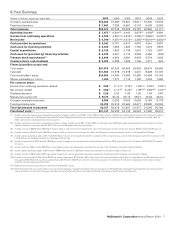

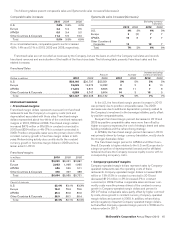

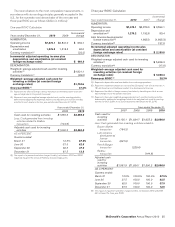

The following tables present comparable sales and Systemwide sales increases/(decreases):

Comparable sales increases

2010 2009 2008

U.S. 3.8% 2.6% 4.0%

Europe 4.4 5.2 8.5

APMEA 6.0 3.4 9.0

Other Countries & Corporate 11.3 5.5 13.0

Total 5.0% 3.8% 6.9%

On a consolidated basis, comparable guest counts increased

4.9%, 1.4% and 3.1% in 2010, 2009 and 2008, respectively.

Systemwide sales increases/(decreases)

Excluding currency

translation

2010 2009 2010 2009

U.S. 4% 3% 4% 3%

Europe 3(2) 77

APMEA 15 877

Other Countries &

Corporate 13 13 7

Total 7% 2% 6% 6%

Franchised sales are not recorded as revenues by the Company, but are the basis on which the Company calculates and records

franchised revenues and are indicative of the health of the franchisee base. The following table presents Franchised sales and the

related increases:

Franchised Sales

Amount Increase Increase excluding

currency translation

Dollars in millions 2010 2009 2008 2010 2009 2010 2009

U.S. $28,166 $26,737 $25,351 5% 5% 5% 5%

Europe 15,049 14,573 14,282 32810

APMEA 11,373 9,871 8,895 15 11 78

Other Countries & Corporate 6,559 5,747 5,604 14 315 9

Total $61,147 $56,928 $54,132 7% 5% 7% 7%

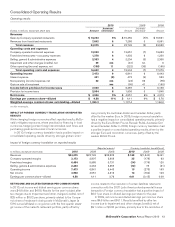

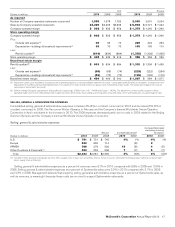

RESTAURANT MARGINS

• Franchised margins

Franchised margin dollars represent revenues from franchised

restaurants less the Company’s occupancy costs (rent and

depreciation) associated with those sites. Franchised margin

dollars represented about two-thirds of the combined restaurant

margins in 2010, 2009 and 2008. Franchised margin dollars

increased $479 million or 8% (8% in constant currencies) in

2010 and $254 million or 4% (7% in constant currencies) in

2009. Positive comparable sales were the primary driver of the

constant currency growth in franchise margin dollars in both

years. Refranchising activity also contributed to the constant

currency growth in franchise margin dollars in 2009 and to a

lesser extent in 2010.

Franchised margins

In millions 2010 2009 2008

U.S. $3,239 $3,031 $2,867

Europe 2,063 1,998 1,965

APMEA 686 559 511

Other Countries & Corporate 476 397 388

Total $6,464 $5,985 $5,731

Percent of revenues

U.S. 83.4% 83.1% 83.3%

Europe 78.2 78.3 78.6

APMEA 89.3 89.6 89.6

Other Countries & Corporate 86.0 86.1 86.4

Total 82.4% 82.1% 82.3%

In the U.S., the franchised margin percent increase in 2010

was primarily due to positive comparable sales. The 2009

decrease was due to additional depreciation primarily related to

the Company’s investment in the beverage initiative, partly offset

by positive comparable sales.

Europe’s franchised margin percent decreased in 2010 and

2009 as positive comparable sales were more than offset by

higher occupancy expenses, the cost of strategic brand and sales

building initiatives and the refranchising strategy.

In APMEA, the franchised margin percent decrease in 2010

was primarily driven by foreign currency translation, mostly due to

the stronger Australian dollar.

The franchised margin percent in APMEA and Other Coun-

tries & Corporate is higher relative to the U.S. and Europe due to

a larger proportion of developmental licensed and/or affiliated

restaurants where the Company receives royalty income with no

corresponding occupancy costs.

• Company-operated margins

Company-operated margin dollars represent sales by Company-

operated restaurants less the operating costs of these

restaurants. Company-operated margin dollars increased $366

million or 13% (12% in constant currencies) in 2010 and

decreased $101 million or 3% (increased 3% in constant

currencies) in 2009. Positive comparable sales and lower com-

modity costs were the primary drivers of the constant currency

growth in Company-operated margin dollars and percent in

2010. Positive comparable sales, partly offset by higher commod-

ity costs, drove growth in constant currency Company-operated

margin dollars and percent in 2009. In addition, refranchising

activity negatively impacted Company-operated margin dollars,

but benefited Company-operated margin percent in 2009 and to

a lesser extent in 2010.

McDonald’s Corporation Annual Report 2010 15