McDonalds 2010 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2010 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

|

|

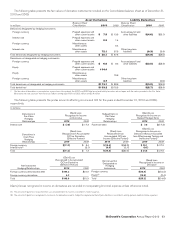

• Fair Value Hedging Strategy

The Company enters into fair value hedges to reduce the

exposure to changes in the fair values of certain liabilities. The

fair value hedges the Company enters into consist of interest rate

exchange agreements which convert a portion of its fixed-rate

debt into floating-rate debt. All of the Company’s interest rate

exchange agreements meet the shortcut method requirements.

Accordingly, changes in the fair values of the interest rate

exchange agreements are exactly offset by changes in the fair

value of the underlying debt. No ineffectiveness has been

recorded to net income related to interest rate exchange agree-

ments designated as fair value hedges for the year ended

December 31, 2010. A total of $2.3 billion of the Company’s

outstanding fixed-rate debt was effectively converted to floating-

rate debt resulting from the use of interest rate exchange

agreements.

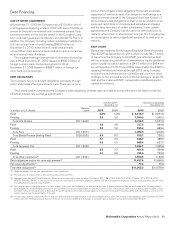

• Cash Flow Hedging Strategy

The Company enters into cash flow hedges to reduce the

exposure to variability in certain expected future cash flows. The

types of cash flow hedges the Company enters into include

interest rate exchange agreements, forward foreign currency

exchange agreements and foreign currency options.

To protect against the reduction in value of forecasted foreign

currency cash flows (such as royalties denominated in foreign

currencies), the Company uses forward foreign currency

exchange agreements and foreign currency options to hedge a

portion of anticipated exposures.

When the U.S. dollar strengthens against foreign currencies,

the decline in present value of future foreign denominated royal-

ties is offset by gains in the fair value of the forward foreign

currency exchange agreements and/or foreign currency options.

Conversely, when the U.S. dollar weakens, the increase in the

present value of future foreign denominated royalties is offset by

losses in the fair value of the forward foreign currency exchange

agreements and/or foreign currency options.

Although the fair value changes in the foreign currency

options may fluctuate over the period of the contract, the

Company’s total loss on a foreign currency option is limited to the

upfront premium paid for the contract. However, the potential

gains on a foreign currency option are unlimited as the settle-

ment value of the contract is based upon the difference between

the exchange rate at inception of the contract and the spot

exchange rate at maturity. In limited situations, the Company uses

foreign currency option collars, which limit the potential gains and

lower the upfront premium paid, to protect against currency

movements.

The hedges typically cover the next 12-15 months for certain

exposures and are denominated in various currencies. As of

December 31, 2010, the Company had derivatives outstanding

with an equivalent notional amount of $434.4 million that were

used to hedge a portion of forecasted foreign currency denomi-

nated royalties.

The Company excludes the time value of foreign currency

options, as well as the discount or premium points on forward

foreign currency exchange agreements, from its effectiveness

assessment on its cash flow hedges. As a result, changes in the

fair value of the derivatives due to these components, as well as

the ineffectiveness of the hedges, are recognized in earnings

currently. The effective portion of the gains or losses on the

derivatives is reported in the deferred hedging adjustment

component of OCI in shareholders’ equity and reclassified into

earnings in the same period or periods in which the hedged

transaction affects earnings.

The Company recorded after tax adjustments related to cash

flow hedges to the deferred hedging adjustment component of

accumulated OCI in shareholders’ equity. The Company recorded

a net decrease of $1.5 million and $31.5 million for the years

ended December 31, 2010 and 2009, respectively. Based on

interest rates and foreign currency exchange rates at

December 31, 2010, no significant amount of the $15.0 million

in cumulative deferred hedging gains, after tax, at December 31,

2010, will be recognized in earnings over the next 12 months as

the underlying hedged transactions are realized.

• Hedge of Net Investment in Foreign Operations

Strategy

The Company primarily uses foreign currency denominated debt

to hedge its investments in certain foreign subsidiaries and affili-

ates. Realized and unrealized translation adjustments from these

hedges are included in shareholders’ equity in the foreign cur-

rency translation component of OCI and offset translation

adjustments on the underlying net assets of foreign subsidiaries

and affiliates, which also are recorded in OCI. As of

December 31, 2010, a total of $3.5 billion of the Company’s

outstanding foreign currency denominated debt was designated

to hedge investments in certain foreign subsidiaries and affiliates.

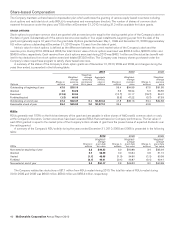

• Credit Risk

The Company is exposed to credit-related losses in the event of

non-performance by the counterparties to its hedging instru-

ments. The counterparties to these agreements consist of a

diverse group of financial institutions. The Company continually

monitors its positions and the credit ratings of its counterparties

and adjusts positions as appropriate. The Company did not have

significant exposure to any individual counterparty at

December 31, 2010 and has master agreements that contain

netting arrangements. Some of these agreements also require

each party to post collateral if credit ratings fall below, or

aggregate exposures exceed, certain contractual limits. At

December 31, 2010, neither the Company nor its counterparties

were required to post collateral on any derivative position, other

than on hedges of certain of the Company’s supplemental benefit

plan liabilities where its counterparties were required to post col-

lateral on their liability positions.

INCOME TAX UNCERTAINTIES

The Company, like other multi-national companies, is regularly

audited by federal, state and foreign tax authorities, and tax

assessments may arise several years after tax returns have been

filed. Accordingly, tax liabilities are recorded when, in

management’s judgment, a tax position does not meet the more

34 McDonald’s Corporation Annual Report 2010