Microsoft 2003 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2003 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

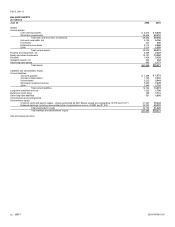

Part II, Item 7,

MSFT 2003 FORM 10-K

15 /

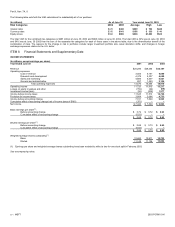

Cash flow from operations was $13.42 billion in fiscal 2001, an increase of $2.00 billion from the prior year. The increase was primarily attributable to the

growth in revenue and other changes in working capital, partially offset by a decrease in the stock option income tax benefit, reflecting decreased stock option

exercises by employees. Cash used for financing was $5.59 billion in fiscal 2001, an increase of $3.39 billion from the prior year. The increase primarily reflected

the repurchase of put warrants in fiscal 2001, compared to the sale of put warrants in the prior fiscal year, as well as an increase in common stock repurchased. All

outstanding put warrants were either retired or exercised during fiscal 2001. During fiscal 2001, we repurchased 178.1 million shares. Cash used for investing was

$8.73 billion in fiscal 2001, a decrease of $658 million from the prior year.

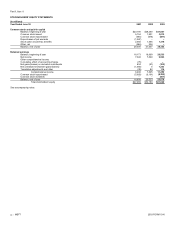

We have no material long-term debt. Stockholders’ equity at June 30, 2003 was $61.02 billion. We will continue to invest in sales, marketing, product support

infrastructure, and existing and advanced areas of technology. Additions to property and equipment will continue, including new facilities and computer systems for

R&D, sales and marketing, support, and administrative staff. Commitments for constructing new buildings were $117 million on June 30, 2003. We have not

engaged in any related party transactions or arrangements with unconsolidated entities or other persons that are reasonably likely to materially affect liquidity or

the availability of or requirements for capital resources.

We believe existing cash and short-term investments together with funds generated from operations should be sufficient to meet operating requirements. Our

philosophy regarding the maintenance of a balance sheet with a large component of cash and short-term investments, as well as equity and other investments,

reflects our views on potential future capital requirements relating to research and development, creation and expansion of sales distribution channels, investments

and acquisitions, share dilution management, legal risks, and challenges to our business model. We continuously assess our investment management approach in

view of our current and potential future needs.

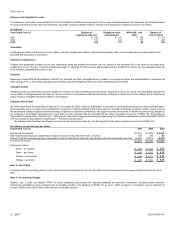

Off-balance sheet arrangements

We have operating leases for most U.S. and international sales and support offices and certain equipment. Rental expense for operating leases was $281 million,

$318 million, and $290 million in 2001, 2002, and 2003, respectively. Future minimum rental commitments under noncancellable leases, in millions of dollars, are:

2004, $218; 2005, $202; 2006, $172; 2007, $134; 2008, $116; and thereafter, $429.

We have unconditionally guaranteed the repayment of certain Japanese yen denominated bank loans and related interest and fees of Jupiter

Telecommunication, Ltd., a Japanese cable company (Jupiter). These guarantees arose on February 1, 2003 in conjunction with the expiration of prior financing

arrangements, including previous guarantees by us. The financing arrangements were entered into by Jupiter as part of financing its operations. As part of

Jupiter’s new financing agreement, we agreed to guarantee repayment by Jupiter of the loans of approximately $51 million. The estimated fair value and the

carrying value of the guarantees was $10.5 million and did not result in a charge to operations. The guarantees are in effect until the earlier of repayment of the

loans, including accrued interest and fees, or February 1, 2009. The maximum amount of the guarantees is limited to the sum of the total due and unpaid principal

amounts, accrued and unpaid interest, and any other related expenses. Additionally, the maximum amount of the guarantees, denominated in Japanese yen, will

vary based on fluctuations in foreign exchange rates. If we were required to make payments under the guarantees, we may recover all or a portion of those

payments upon liquidation of Jupiter’s assets. The proceeds from such liquidation cannot be accurately estimated due to the multitude of factors that would affect

the valuation and realization of the proceeds in the event of liquidation.

In connection with various operating leases, we issued residual value guarantees, which provide that if we do not purchase the leased property from the lessor

at the end of the lease term, then we are liable to the lessor for an amount equal to the shortage (if any) between the proceeds from the sale of the property and an

agreed value. As of June 30, 2003, the maximum amount of the residual value guarantees was approximately $271 million. We believe that proceeds from the sale

of properties under operating leases would exceed the payment obligation and therefore no liability to us currently exists.

We provide indemnifications of varying scope and size to certain customers against claims of intellectual property infringement made by third parties arising

from the use of our products. We evaluate estimated losses for such indemnifications under SFAS 5, Accounting for Contingencies, as interpreted by FIN 45. We

consider such factors as the degree of probability of an unfavorable outcome and the ability to make a reasonable estimate of the amount of loss. To date, we

have not encountered material costs as a result of such obligations and have not accrued any liabilities related to such indemnifications in our financial statements.

RECENTLY ISSUED ACCOUNTING STANDARDS

In January 2003, the FASB issued Interpretation 46, Consolidation of Variable Interest Entities. In general, a variable interest entity is a corporation, partnership,

trust, or any other legal structure used for business purposes that either (a) does not have equity investors with voting rights or (b) has equity investors that do not

provide sufficient financial resources for the entity to support its activities. Interpretation 46 requires a variable interest entity to be consolidated by a company if

that company is subject to a majority of the risk of loss from the variable interest entity’s activities or entitled to receive a majority of the entity’s residual returns or

both. The consolidation requirements of Interpretation 46 apply immediately to variable interest entities created after January 31, 2003. The consolidation

requirements apply to transactions entered into prior to February 1, 2003 in the first fiscal year or interim period beginning after June 15, 2003. Certain of the

disclosure requirements apply in all financial statements issued after January 31, 2003, regardless of when the variable interest entity was established. The

adoption of the Interpretation on July 1, 2003 did not have a material impact on our financial statements.

In April 2003, the FASB issued SFAS 149, Amendment of Statement 133 on Derivative Instruments and Hedging Activities, which amends and clarifies

accounting for derivative instruments, including certain derivative instruments embedded in other contracts, and for hedging activities under SFAS 133. The

Statement is effective (with certain exceptions) for contracts entered into or modified after June 30, 2003. We do not believe the adoption of this Statement will

have a material impact on our financial statements.

In May 2003, the FASB issued SFAS 150, Accounting for Certain Financial Instruments with Characteristics of both Liabilities and Equity. The Statement

establishes standards for how an issuer classifies and measures certain financial instruments with