Microsoft 2003 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2003 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

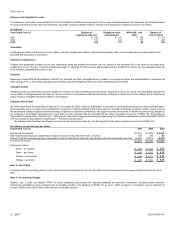

Part II, Item 7,

MSFT 2003 FORM 10-K

16 /

characteristics of both liabilities and equity. It requires that an issuer classify a financial instrument that is within its scope as a liability (or an asset in some

circumstances). It is effective for financial instruments entered into or modified after May 31, 2003, and otherwise is effective at the beginning of the first interim

period beginning after June 15, 2003. While we do not believe the adoption of this Statement will have a material impact on our financial statements, we continue

to assess the impact this Statement will have on certain of our share repurchase programs.

APPLICATION OF CRITICAL ACCOUNTING POLICIES

Our financial statements and accompanying notes are prepared in accordance with U.S. GAAP. Preparing financial statements requires management to make

estimates and assumptions that affect the reported amounts of assets, liabilities, revenue, and expenses. These estimates and assumptions are affected by

management’s application of accounting policies. Critical accounting policies for us include revenue recognition, impairment of investment securities, impairment of

goodwill, accounting for research and development costs, accounting for legal contingencies, and accounting for income taxes.

We account for the licensing of software in accordance with American Institute of Certified Public Accountants (AICPA) Statement of Position (SOP) 97-2,

Software Revenue Recognition. The application of SOP 97-2 requires judgment, including whether a software arrangement includes multiple elements, and if so,

whether vendor-specific objective evidence (VSOE) of fair value exists for those elements. End users receive certain elements of our products over a period of

time. These elements include free post-delivery telephone support and the right to receive unspecified upgrades/enhancements of Microsoft Internet Explorer on a

when-and-if-available basis, the fair value of which is recognized over the product’s estimated life cycle. Changes to the elements in a software arrangement, the

ability to identify VSOE for those elements, the fair value of the respective elements, and changes to a product’s estimated life cycle could materially impact the

amount of earned and unearned revenue. Judgment is also required to assess whether future releases of certain software represent new products or upgrades

and enhancements to existing products.

SFAS 115, Accounting for Certain Investments in Debt and Equity Securities, and Securities and Exchange Commission (SEC) Staff Accounting Bulletin (SAB)

59, Accounting for Noncurrent Marketable Equity Securities, provide guidance on determining when an investment is other-than-temporarily impaired. This

determination requires significant judgment. In making this judgment, we evaluate, among other factors, the duration and extent to which the fair value of an

investment is less than its cost; the financial health of and near-term business outlook for the investee, including factors such as industry and sector performance,

changes in technology, and operational and financing cash flow; and our intent and ability to hold the investment.

SFAS 142, Goodwill and Other Intangible Assets, requires that goodwill be tested for impairment at the reporting unit level (operating segment or one level

below an operating segment) on an annual basis (July 1st for Microsoft) and between annual tests in certain circumstances. Application of the goodwill impairment

test requires judgment, including the identification of reporting units, assigning assets and liabilities to reporting units, assigning goodwill to reporting units, and

determining the fair value of each reporting unit. Significant judgments required to estimate the fair value of reporting units include estimating future cash flows,

determining appropriate discount rates and other assumptions. Changes in these estimates and assumptions could materially affect the determination of fair value

and/or goodwill impairment for each reporting unit.

We account for research and development costs in accordance with several accounting pronouncements, including SFAS 2, Accounting for Research and

Development Costs, and SFAS 86, Accounting for the Costs of Computer Software to be Sold, Leased, or Otherwise Marketed. SFAS 86 specifies that costs

incurred internally in creating a computer software product should be charged to expense when incurred as research and development until technological

feasibility has been established for the product. Once technological feasibility is established, all software costs should be capitalized until the product is available

for general release to customers. Judgment is required in determining when technological feasibility of a product is established. We have determined that

technological feasibility for our products is reached shortly before the products are released to manufacturing. Costs incurred after technological feasibility is

established are not material, and accordingly, we expense all research and development costs when incurred.

We are subject to various legal proceedings and claims, the outcomes of which are subject to significant uncertainty. SFAS 5, Accounting for Contingencies,

requires that an estimated loss from a loss contingency should be accrued by a charge to income if it is probable that an asset has been impaired or a liability has

been incurred and the amount of the loss can be reasonably estimated. Disclosure of a contingency is required if there is at least a reasonable possibility that a

loss has been incurred. We evaluate, among other factors, the degree of probability of an unfavorable outcome and the ability to make a reasonable estimate of

the amount of loss. Changes in these factors could materially impact our financial position or our results of operations.

SFAS 109, Accounting for Income Taxes, establishes financial accounting and reporting standards for the effect of income taxes. The objectives of accounting

for income taxes are to recognize the amount of taxes payable or refundable for the current year and deferred tax liabilities and assets for the future tax

consequences of events that have been recognized in an entity’s financial statements or tax returns. Judgment is required in assessing the future tax

consequences of events that have been recognized in our financial statements or tax returns. Fluctuations in the actual outcome of these future tax consequences

could materially impact our financial position or our results of operations.

ISSUES AND UNCERTAINTIES

This Annual Report on Form 10-K contains statements that are forward-looking. These statements are based on current expectations and assumptions that are

subject to risks and uncertainties. Actual results could differ materially because of issues and uncertainties such as those listed below and elsewhere in this report,

which, among others, should be considered in evaluating our financial outlook.

Challenges to our Business Model

Since our inception, our business model has been based upon customers agreeing to pay a fee to license software developed and distributed by us. Under this

commercial software model, software developers bear the costs of converting original ideas into software products through investments in research and

development, offsetting these costs with the revenues received from the distribution of their products. We believe the commercial software model has had

substantial benefits for users of software, allowing them to rely on our expertise and the expertise of other software developers that have powerful incentives to

develop