Microsoft 2003 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2003 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

|

|

Part II, Item 8

MSFT 2003 FORM 10-K

35 /

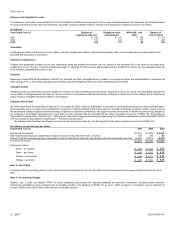

life). The $1,197 million of goodwill was assigned to the Microsoft Business Solutions segment. Of that total amount, approximately $900 million is expected to be

deductible for tax purposes.

Of the $75 million of acquired intangible assets in the Rare acquisition, $13 million was assigned to research and development assets that were written off in

accordance with FIN 4. Those write-offs are included in Research and Development expenses. The remaining $62 million of acquired intangible assets have a

weighted average useful life of approximately five years. The intangible assets that make up that amount include technology of $36 million (five-year weighted

average useful life), contracts of $16 million (five-year weighted average useful life), and marketing of $10 million (five-year weighted average useful life). The $281

million of goodwill was assigned to the Home and Entertainment segment. Of that total amount, approximately $270 million is expected to be deductible for tax

purposes.

The $30 million of acquired intangible assets in the Placeware acquisition have a weighted average useful life of approximately eight years. The intangible

assets that make up that amount include technology of $4 million (four-year weighted-average useful life), customers of $23 million (ten-year weighted-average

useful life), contracts of $1 million (six-year weighted-average useful life), and marketing of $2 million (one-year weighted average useful life). The $180 million of

goodwill was assigned to the Information Worker segment. None of the goodwill is expected to be deductible for tax purposes.

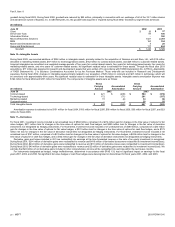

Note 19—Commitments and Guarantees

We have operating leases for most U.S. and international sales and support offices and certain equipment. Rental expense for operating leases was $281 million,

$318 million, and $290 million in 2001, 2002, and 2003. Future minimum rental commitments under noncancellable leases, in millions of dollars, are: 2004, $218;

2005, $202; 2006, $172; 2007, $134; 2008, $116; and thereafter, $429. We have committed $117 million for constructing new buildings.

In November 2002, the FASB issued Interpretation 45, Guarantor’s Accounting and Disclosure Requirements for Guarantees, Including Indirect Guarantees of

Indebtedness of Others (FIN 45). FIN 45 elaborates on previously existing disclosure requirements for most guarantees, including loan guarantees such as

standby letters of credit. It also clarifies that at the time a company issues a guarantee, the company must recognize an initial liability for the fair value, or market

value, of the obligations it assumes under the guarantee and must disclose that information in its interim and annual financial statements. The provisions related to

recognizing a liability at inception of the guarantee for the fair value of the guarantor’s obligations does not apply to product warranties or to guarantees accounted

for as derivatives. The initial recognition and initial measurement provisions apply on a prospective basis to guarantees issued or modified after December 31,

2002.

We have unconditionally guaranteed the repayment of certain Japanese yen denominated bank loans and related interest and fees of Jupiter

Telecommunication, Ltd., a Japanese cable company (Jupiter). These guarantees arose on February 1, 2003 in conjunction with the expiration of prior financing

arrangements, including previous guarantees by us. The financing arrangements were entered into by Jupiter as part of financing its operations. As part of

Jupiter’s new financing agreement, we agreed to guarantee repayment by Jupiter of the loans of approximately $51 million. The estimated fair value and the

carrying value of the guarantees was $10.5 million and did not result in a charge to operations. The guarantees are in effect until the earlier of repayment of the

loans, including accrued interest and fees, or February 1, 2009. The maximum amount of the guarantees is limited to the sum of the total due and unpaid principal

amounts, accrued and unpaid interest, and any other related expenses. Additionally, the maximum amount of the guarantees, denominated in Japanese yen, will

vary based on fluctuations in foreign exchange rates. If we were required to make payments under the guarantees, we may recover all or a portion of those

payments upon liquidation of the Jupiter’s assets. The proceeds from such liquidation cannot be accurately estimated due to the multitude of factors that would

affect the valuation and realization of the proceeds in the event of liquidation.

In connection with various operating leases, we issued residual value guarantees, which provide that if we do not purchase the leased property from the lessor

at the end of the lease term, then we are liable to the lessor for an amount equal to the shortage (if any) between the proceeds from the sale of the property and an

agreed value. As of June 30, 2003, the maximum amount of the residual value guarantees was approximately $271 million. We believe that proceeds from the sale

of properties under operating leases would exceed the payment obligation and therefore no liability to us currently exists.

We provide indemnifications of varying scope and size to certain customers against claims of intellectual property infringement made by third parties arising

from the use of our products. We evaluate estimated losses for such indemnifications under SFAS 5, Accounting for Contingencies, as interpreted by FIN 45. We

consider such factors as the degree of probability of an unfavorable outcome and the ability to make a reasonable estimate of the amount of loss. To date, we

have not encountered material costs as a result of such obligations and have not accrued any liabilities related to such indemnifications in our financial statements.

Our product warranty accrual reflects management’s best estimate of probable liability under its product warranties (primarily relating to the Xbox console). We

determine the warranty accrual based on known product failures (if any), historical experience, and other currently available evidence. Changes in the product

warranty accrual for the fiscal year ended June 30, 2003 were as follows (in millions):

Balance, beginning of period $ 8

Payments made –

Change in liability for warranties issued during the period 29

Change in liability for preexisting warranties (25)

Balance, end of period $ 12

Note 20—Contingencies

We are a defendant in U.S. v. Microsoft and New York v. Microsoft, companion lawsuits filed by the Antitrust Division of the U.S. Department of Justice (DOJ) and

a group of eighteen state Attorneys General alleging violations of the Sherman Act and various state antitrust laws. After the trial, the District Court entered

Findings of Fact and Conclusions of Law stating that we had violated Sections 1 and 2 of the Sherman Act and various state antitrust laws. A Judgment was

entered on June 7, 2000 ordering, among