Starbucks 2013 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2013 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

54

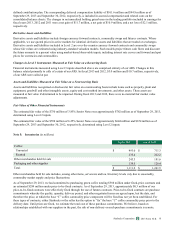

effect of dilutive potential common shares outstanding during the period, calculated using the treasury stock method. Dilutive

potential common shares include outstanding stock options and RSUs. Performance-based RSUs are considered dilutive when

the related performance criterion has been met.

Common Stock Share Repurchases

We may repurchase shares of Starbucks common stock under a program authorized by our Board of Directors, including

pursuant to a contract, instruction or written plan meeting the requirements of Rule 10b5-1(c)(1) of the Securities Exchange Act

of 1934. Under applicable Washington State law, shares repurchased are retired and not displayed separately as treasury stock

on the financial statements. Instead, the par value of repurchased shares is deducted from common stock and the excess

repurchase price over par value is deducted from additional paid-in capital and from retained earnings, once additional paid-in

capital is depleted.

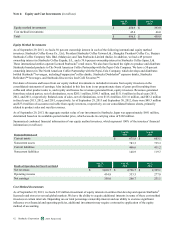

Recent Accounting Pronouncements

In July 2013, the FASB issued guidance on the financial statement presentation of an unrecognized tax benefit when a net

operating loss carryforward, a similar tax loss, or a tax credit carryforward exists. This guidance requires the unrecognized tax

benefit to be presented in the financial statements as a reduction to a deferred tax asset. When a deferred tax asset is not

available, or the asset is not intended to be used for this purpose, an entity should present the unrecognized tax benefit in the

financial statements as a liability and should not net the unrecognized tax benefit with a deferred tax asset. The guidance will

become effective for us at the beginning of our first quarter of fiscal 2015. We do not expect the adoption of this guidance will

have a material impact on our financial statements.

In March 2013, the FASB issued guidance on a parent's accounting for the cumulative translation adjustment upon

derecognition of certain subsidiaries or groups of assets within a foreign entity or of an investment in a foreign entity. This

guidance requires a parent to release any related cumulative translation adjustment into net income only if the sale or transfer

results in the complete or substantially complete liquidation of the foreign entity in which the subsidiary or group of assets had

resided. The guidance will become effective for us at the beginning of our first quarter of fiscal 2015. We do not expect the

adoption of this guidance will have a material impact on our financial statements.

In February 2013, the FASB issued guidance that adds additional disclosure requirements for items reclassified out of

accumulated other comprehensive income. This guidance requires the disclosure of significant amounts reclassified from each

component of accumulated other comprehensive income and the income statement line items affected by the reclassification.

The guidance will become effective for us at the beginning of our first quarter of fiscal 2014. The adoption of this guidance will

result in the disclosure of reclassifications from accumulated other comprehensive income by component in the consolidated

statements of comprehensive income either on the face of the consolidated statements of earnings or in the Notes.

In January 2013, the FASB issued guidance clarifying the scope of disclosure requirements for offsetting assets and liabilities.

The amended guidance limits the scope of balance sheet offsetting disclosures to derivatives, repurchase agreements, and

securities lending transactions to the extent that they are offset in the financial statements or subject to an enforceable master

netting arrangement or similar agreement. The guidance will become effective for us at the beginning of our first quarter of

fiscal 2014. We do not expect the adoption of this guidance will have a material impact on our financial statements.

In July 2012, the FASB issued guidance that revises the requirements around how entities test indefinite-lived intangible assets,

other than goodwill, for impairment. The guidance allows companies to perform a qualitative assessment before calculating the

fair value of the indefinite-lived intangible asset. If entities determine, on the basis of qualitative factors, that the fair value of

the indefinite-lived intangible asset is more likely than not greater than the carrying amount, a quantitative calculation would

not be needed. The guidance became effective for us at the beginning of our first quarter of fiscal 2013. The adoption of this

guidance did not have a material impact on our financial statements.

In June 2011, the FASB issued guidance that revises the manner in which entities present comprehensive income in their

financial statements. The guidance requires entities to report the components of comprehensive income in either a single,

continuous statement or two separate but consecutive statements. The guidance became effective for us at the beginning of our

first quarter of fiscal 2013. In adopting this guidance, we added the consolidated statements of comprehensive income

following our consolidated statements of earnings.

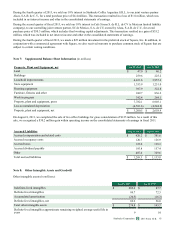

Reclassifications

Change in shared service allocations

Effective at the beginning of fiscal 2012, we implemented a strategic realignment of our organizational structure designed to

accelerate our global growth strategy. A president for each region, reporting directly to our chief executive officer, was

appointed to oversee the company-operated retail business working closely with both the licensed and joint-venture business

2013 10-K

Starbucks Corporation Form