Starbucks 2014 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2014 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

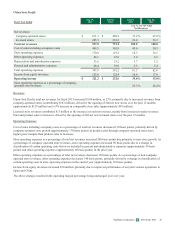

40 Starbucks Corporation 2014 Form 10-K

COMMODITY PRICES, AVAILABILITY AND GENERAL RISK CONDITIONS

Commodity price risk represents Starbucks primary market risk, generated by our purchases of green coffee and dairy products,

among other items. We purchase, roast and sell high-quality whole-bean arabica coffee and related products and risk arises

from the price volatility of green coffee. In addition to coffee, we also purchase significant amounts of dairy products to

support the needs of our company-operated stores. The price and availability of these commodities directly impacts our results

of operations and we expect commodity prices, particularly coffee, to impact future results of operations. For additional details

see Product Supply in Item 1, as well as Risk Factors in Item 1A of this 10-K.

FINANCIAL RISK MANAGEMENT

Market risk is defined as the risk of losses due to changes in commodity prices, foreign currency exchange rates, equity

security prices, and interest rates. We manage our exposure to various market-based risks according to a market price risk

management policy. Under this policy, market-based risks are quantified and evaluated for potential mitigation strategies, such

as entering into hedging transactions. The market price risk management policy governs how hedging instruments may be used

to mitigate risk. Risk limits are set annually and prohibit speculative trading activity. We also monitor and limit the amount of

associated counterparty credit risk. In general, hedging instruments do not have maturities in excess of three years.

The sensitivity analyses disclosed below provide only a limited, point-in-time view of the market risk of the financial

instruments discussed. The actual impact of the respective underlying rates and price changes on the financial instruments may

differ significantly from those shown in the sensitivity analyses.

Commodity Price Risk

We purchase commodity inputs, including coffee, dairy products and diesel that are used in our operations and are subject to

price fluctuations that impact our financial results. We use a combination of pricing features embedded within supply contracts

and financial derivatives to manage our commodity price risk exposure, such as fixed-price and price-to-be-fixed contracts for

coffee purchases.

The following table summarizes the potential impact as of September 28, 2014 to Starbucks future net earnings and other

comprehensive income ("OCI") from changes in commodity prices. The information provided below relates only to the

hedging instruments and does not represent the corresponding changes in the underlying hedged items (in millions):

Increase/(Decrease) to Net Earnings Increase/(Decrease) to OCI

10% Increase in

Underlying Rate 10% Decrease in

Underlying Rate 10% Increase in

Underlying Rate 10% Decrease in

Underlying Rate

Commodity hedges $ 4 $ (4) $ 3 $ (3)

Foreign Currency Exchange Risk

The majority of our revenue, expense and capital purchasing activities are transacted in US dollars. However, because a portion

of our operations consists of activities outside of the US, we have transactions in other currencies, primarily the Canadian

dollar, Japanese yen, Chinese renminbi, British pound, and euro. To reduce cash flow volatility from foreign currency

fluctuations, we enter into derivative instruments to hedge portions of cash flows of anticipated revenue streams and inventory

purchases in currencies other than our functional currency, the US dollar, as well as the translation risk of certain balance sheet

items. See Note 3, Derivative Financial Instruments, for further discussion.

The following table summarizes the potential impact as of September 28, 2014 to Starbucks future net earnings and other

comprehensive income ("OCI") from changes in the fair value of these derivative financial instruments due to a change in the

value of the US dollar as compared to foreign exchange rates. The information provided below relates only to the hedging

instruments and does not represent the corresponding changes in the underlying hedged items (in millions):

Increase/(Decrease) to Net Earnings Increase/(Decrease) to OCI

10% Increase in

Underlying Rate 10% Decrease in

Underlying Rate 10% Increase in

Underlying Rate 10% Decrease in

Underlying Rate

Foreign currency hedges $ 7 $ (7) $ 47 $ (47)