Starbucks 2014 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2014 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

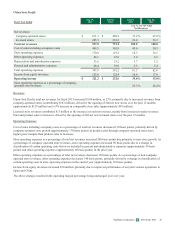

42 Starbucks Corporation 2014 Form 10-K

Property, Plant and Equipment and Other Definite-Lived Assets

We evaluate property, plant and equipment and other definite-lived assets for impairment when facts and circumstances indicate

that the carrying values of such assets may not be recoverable. When evaluating for impairment, we first compare the carrying

value of the asset to the asset’s estimated future undiscounted cash flows. If the estimated undiscounted future cash flows are

less than the carrying value of the asset, we determine if we have an impairment loss by comparing the carrying value of the

asset to the asset's estimated fair value and recognize an impairment charge when the asset’s carrying value exceeds its

estimated fair value. The adjusted carrying amount of the asset becomes its new cost basis and is depreciated over the asset's

remaining useful life.

Long-lived assets are grouped with other assets and liabilities at the lowest level for which identifiable cash flows are largely

independent of the cash flows of other assets and liabilities. For company-operated store assets, the impairment test is

performed at the individual store asset group level. The fair value of a store’s assets is estimated using a discounted cash flow

model. For other long-lived assets, fair value is determined using an approach that is appropriate based on the relevant facts and

circumstances, which may include discounted cash flows, comparable transactions, or comparable company analyses.

Our impairment calculations contain uncertainties because they require management to make assumptions and to apply

judgment to estimate future cash flows and asset fair values. Key assumptions used in estimating future cash flows and asset

fair values include projected revenue growth and operating expenses, as well as forecasting asset useful lives and selecting an

appropriate discount rate. For company-operated stores, estimates of revenue growth and operating expenses are based on

internal projections and consider the store’s historical performance, the local market economics and the business environment

impacting the store’s performance. The discount rate is selected based on what we believe a buyer would assume when

determining a purchase price for the store. These estimates are subjective and our ability to realize future cash flows and asset

fair values is affected by factors such as ongoing maintenance and improvement of the assets, changes in economic conditions,

and changes in operating performance.

During fiscal 2014, there were no significant changes in any of our estimates or assumptions that had a material impact on the

outcome of our impairment calculations. However, as we periodically reassess estimated future cash flows and asset fair values,

changes in our estimates and assumptions may cause us to realize material impairment charges in the future.

Goodwill and Indefinite-Lived Intangible Assets

We evaluate goodwill and indefinite-lived intangible assets (primarily trade names and trademarks) for impairment annually

during our third fiscal quarter, or more frequently if an event occurs or circumstances change that would indicate that

impairment may exist. When evaluating for impairment, we may first perform a qualitative assessment to determine whether it

is more likely than not that a reporting unit or intangible asset group is impaired. If we do not perform a qualitative assessment,

or if we determine that it is not more likely than not that the fair value of the reporting unit or intangible asset group exceeds its

carrying amount, we calculate the estimated fair value of the reporting unit or intangible asset group. Fair value is the price a

market participant would pay for the reporting unit or intangible asset and is typically calculated using an income approach,

such as a discounted cash flow or relief-from-royalty method. If the carrying amount of the reporting unit or intangible asset

group exceeds the estimated fair value, an impairment charge is recorded to reduce the carrying value to the estimated fair

value.

Our decision to perform a qualitative impairment assessment for an individual reporting unit in a given year is influenced by a

number of factors, inclusive of the size of the reporting unit's goodwill, the significance of the excess of the reporting unit's

estimated fair value over carrying value at the last quantitative assessment date, and the amount of time in between quantitative

fair value assessments. During fiscal 2014, as part of our annual goodwill impairment analysis, we performed the qualitative

assessment for approximately $104 million, or 12%, of our total goodwill balance of $856.2 million, the majority of which

resides in our China retail, US licensed and US consumer packaged goods reporting units.

As part of our ongoing operations, we may close certain stores within a reporting unit containing goodwill due to

underperformance of the store or inability to renew our lease, among other reasons. We may abandon certain assets associated

with a closed store, including leasehold improvements and other non-transferable assets. When a portion of a reporting unit that

constitutes a business is to be disposed of, the associated goodwill is included in the carrying amount when determining any

loss on disposal. Our evaluation of whether the portion of a reporting unit being disposed of constitutes a business occurs on

the date of abandonment. Although an operating store meets the accounting definition of a business prior to abandonment, it

does not constitute a business on the closure date because the remaining assets on that date do not constitute an integrated set of

assets that are capable of being managed for the purpose of providing a return to investors. As a result, when closing individual

stores, we do not include goodwill in the calculation of any loss on disposal of the related assets. If store closures are indicative

of potential impairment of goodwill at the reporting unit level, we perform an evaluation of our reporting unit goodwill when

such closures occur.