Starbucks 2014 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2014 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

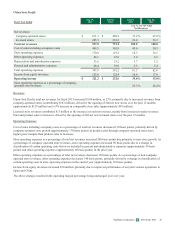

Starbucks Corporation 2014 Form 10-K 43

Our impairment calculations contain uncertainties because they require management to make assumptions and to apply

judgment when performing a qualitative assessment or when estimating future cash flows and asset fair values. Key

assumptions used in estimating future cash flows and asset fair values typically include projected revenue growth and operating

expenses related to existing businesses, product innovation and new store concepts, as well as selecting an appropriate discount

rate. For indefinite-lived intangible assets, management also makes assumptions around the royalty rate that could

hypothetically be charged by a licensor of the asset to an unrelated licensee. For a goodwill reporting unit, estimates of revenue

growth and operating expenses are based on internal projections considering the reporting unit’s past performance and

forecasted growth, strategic initiatives, local market economics and the local business environment impacting the reporting

unit’s performance. The discount rate is selected based on the estimated cost of capital for a retail operator to operate the

reporting unit in the region. For indefinite-lived intangible assets, estimates of revenue growth are based on internal projections

considering the intangible asset group's past performance and forecasted growth, and the royalty rate used is based on observed

market royalty rates for similar licensing arrangements, adjusted for our particular facts and circumstances. The discount rate is

selected based on the estimated cost of capital that reflects the risk profile of the related business. These estimates are highly

subjective judgments and our ability to realize the future cash flows used in our fair value calculations is affected by factors

such as the success of strategic initiatives, changes in economic conditions, changes in our operating performance, and changes

in our business strategies.

For fiscal 2014, we determined the fair value of our material reporting units and intangible asset groups were significantly in

excess of their carrying values. Accordingly, we did not recognize any material impairment charges during the current fiscal

year. During fiscal 2014, there were no significant changes in any of our estimates or assumptions that had a material impact on

the outcome of our impairment calculations. However, as we periodically reassess estimated future cash flows and asset fair

values, changes in our estimates and assumptions may cause us to realize material impairment charges in the future.

Income Taxes

We recognize deferred tax assets and liabilities based on the differences between the financial statement carrying amounts and

the respective tax bases of our assets and liabilities. Deferred tax assets and liabilities are measured using current enacted tax

rates expected to apply to taxable income in the years in which we expect the temporary differences to reverse. We routinely

evaluate the likelihood of realizing the benefit of our deferred tax assets and may record a valuation allowance if, based on all

available evidence, we determine that some portion of the tax benefit will not be realized. Changes in tax laws and rates may

affect recorded deferred tax assets and liabilities and our effective tax rate in the future; however, we do not expect changes

from recently enacted tax laws to be material to the consolidated financial statements.

In evaluating our ability to recover our deferred tax assets within the jurisdiction from which they arise, we consider all

available positive and negative evidence, including scheduled reversals of deferred tax liabilities, projected future taxable

income, tax-planning strategies, and results of recent operations. In projecting future taxable income, we consider historical

results and incorporate assumptions about the amount of future state, federal, and foreign pretax operating income adjusted for

items that do not have tax consequences. Our assumptions regarding future taxable income are consistent with the plans and

estimates we are using to manage the underlying businesses. In evaluating the objective evidence that historical results provide,

we consider three years of cumulative operating income/(loss).

In addition, our income tax returns are periodically audited by domestic and foreign tax authorities. These audits include review

of our tax filing positions, including the timing and amount of deductions taken and the allocation of income between tax

jurisdictions. We evaluate our exposures associated with our various tax filing positions and recognize a tax benefit only if it is

more likely than not that the tax position will be sustained upon examination by the relevant taxing authorities, including

resolutions of any related appeals or litigation processes, based on the technical merits of our position. For uncertain tax

positions that do not meet this threshold, we record a related liability. We adjust our unrecognized tax benefit liability and

income tax expense in the period in which the uncertain tax position is effectively settled, the statute of limitations expires for

the relevant taxing authority to examine the tax position, or when new information becomes available. There is a reasonable

possibility that our unrecognized tax benefit liability will be adjusted within 12 months due to the expiration of a statute of

limitations; however, we do not expect this change to be material to the consolidated financial statements.

We have generated income in certain foreign jurisdictions that has not been subject to US income taxes. We intend to reinvest

these earnings for the foreseeable future. While we do not expect to repatriate cash to the US to satisfy domestic liquidity

needs, if these amounts were distributed to the US, in the form of dividends or otherwise, we would be subject to additional US

income taxes, which could be material. Determination of the amount of unrecognized deferred income tax liabilities on these

earnings is not practicable because such liability, if any, is dependent on circumstances existing if and when remittance occurs.

Our income tax expense, deferred tax assets and liabilities, and liabilities for unrecognized tax benefits reflect management’s

best assessment of estimated current and future taxes to be paid. Deferred tax asset valuation allowances and our liabilities for

unrecognized tax benefits require significant management judgment regarding applicable statutes and their related

interpretation, the status of various income tax audits, and our particular facts and circumstances. Although we believe that the