Target 2002 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2002 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

our lowest expense rate division. In 2001, our operating expense

rate improved compared to 2000, principally benefiting from the

mix impact of growth at Target.

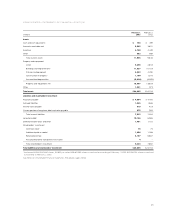

Pre-tax Segment Profit

Pre-tax segment profit increased 16.7 percent in 2002 to $3,461

million, compared with $2,965 million in 2001. The increase was

driven by growth at Target, which delivered 89 percent of

consolidated pre-tax segment profit. Marshall Field’s pre-tax segment

profit was essentially equal to last year, while Mervyn’s experienced

a decline in pre-tax segment profit compared to last year. Target’s

full-year profit margin rate increased to 8.4 percent of revenues in

2002 from 7.8 percent in 2001.

In 2001, pre-tax segment profit increased 10.6 percent to $2,965

million, compared with $2,682 million in 2000. The increase was

driven by growth at Target, which delivered 86 percent of

consolidated pre-tax segment profit. Mervyn’s also experienced an

increase in pre-tax segment profit, while Marshall Field’s experienced

a decline compared to 2000. Target’s full-year profit margin rate

increased to 7.8 percent of revenues in 2001 from 7.6 percent

in 2000.

We define pre-tax segment profit as earnings before interest,

last-in, first-out (LIFO) provision, securitization effects, other expense

and unusual items. A reconciliation of pre-tax segment profit to pre-

tax earnings is provided in the Notes to Consolidated Financial

Statements on page 35. Our segment disclosures may not be

consistent with disclosures of other companies in the same line

of business.

Pre-tax Segment Profit and as a Percent of Revenues

Pre-tax Segment Profit As a Percent of Revenues

(millions) 2002 2001 2000 2002 2001 2000

Target $3,088 $2,546 $2,223 8.4% 7.8% 7.6%

Mervyn’s 238 286 269 6.2 7.1 6.5

Marshall Field’s 135 133 190 5.0 4.8 6.4

Total pre-tax

segment

profit $3,461 $2,965 $2,682 8.0% 7.5% 7.4%

Net earnings $1,654 $1,368 $1,264

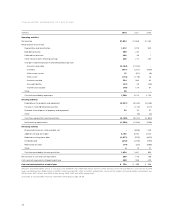

EBITDA

We provide the following EBITDA information derived from our

financial statements because we believe it provides a meaningful

aid to analysis of our performance by segment. We define segment

EBITDA as pre-tax segment profit before depreciation and

amortization expense. This presentation is not intended to be a

substitute for GAAP required measures of profitability and cash

flow. A reconciliation of pre-tax segment profit to pre-tax earnings

is provided in the Notes to Consolidated Financial Statements on

page 35. Our definition of EBITDA may differ from definitions used

by other companies.

EBITDA and as a Percent of Revenues

EBITDA As a Percent of Revenues

(millions) 2002 2001 2000 2002 2001 2000

Target $4,013 $3,330 $2,883 10.9% 10.2% 9.8%

Mervyn’s 360 412 400 9.4 10.2 9.6

Marshall Field’s 260 268 323 9.7 9.7 10.9

Total segment

EBITDA $4,633 $4,010 $3,606 10.7% 10.2% 9.9%

Segment depre-

ciation and

amortization (1,172) (1,045) (924)

Pre-tax segment

profit $3,461 $2,965 $2,682

Cash flows

provided by/

(used for):

Operating

activities $1,590 $2,012 $2,134

Investing

activities (3,189) (3,310) (2,692)

Financing

activities 1,858 1,441 694

Net increase in

cash and cash

equivalents $ 259 $ 143 $ 136

Depreciation and Amortization

In 2002, depreciation and amortization increased 12.4 percent to

$1,212 million compared to 2001. In 2001, depreciation and

amortization increased 14.8 percent to $1,079 million compared to

2000. The increase in both years is primarily due to new store

growth at Target.

Interest Expense

In 2002, interest expense was $588 million, $88 million higher than

the total of interest expense and interest equivalent in 2001. For

analytical purposes, the amounts that represented payments

accrued to holders of sold securitized receivables prior to August

22, 2001 (discussed in detail under Accounting for Accounts

Receivable on page 19) are considered as interest equivalent. After

that date such payments constituted interest expense. In 2002, $25

million of the increase in interest expense was due to the loss

resulting from the early call or repurchase of $266 million of debt.

The remaining $63 million increase in interest expense is attributable

to higher average funded balances, partially offset by the favorable

effect of lower average portfolio interest rates. The average portfolio

interest rate in 2002 was 5.6 percent compared with 6.4 percent in

2001, and 7.4 percent in 2000. In 2001, the total of interest expense

and interest equivalent was $24 million higher than in 2000 due to

higher average funded balances partially offset by the favorable

effect of lower average portfolio interest rates.

During 2002, we called or repurchased $266 million of debt

resulting in a loss of $34 million ($.02 per share). The debt called

or repurchased had a weighted average interest rate of 8.8 percent

and an average remaining life of 19 years. In 2001 and 2000, we

18