Target 2002 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2002 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

|

|

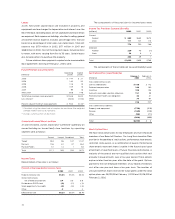

Cash Equivalents

Cash equivalents represent short-term investments with a maturity

of three months or less from the time of purchase.

Accounts Receivable and Receivable-backed Securities

Accounts receivable is recorded net of an allowance for expected

losses. The allowance, recognized in an amount equal to the

anticipated future write-offs based on historical experience and

other factors, was $399 million at February 1, 2003 and $261 million

at February 2, 2002.

Through our special purpose subsidiary, Target Receivables

Corporation (TRC), we transfer, on an ongoing basis, substantially

all of our receivables to the Target Credit Card Master Trust (the

Trust) in return for certificates representing undivided interests in

the Trust’s assets. TRC owns the undivided interest in the Trust’s

assets, other than the Trust’s assets securing the financing

transactions entered into by the Trust and the 2 percent of Trust

assets held by Retailers National Bank (RNB). RNB is a wholly owned

subsidiary of the Corporation that also services receivables. The

Trust assets and the related income and expenses are reflected in

each operating segment’s assets and operating results based on

the origin of the credit card giving rise to the receivable.

Concurrent with our August 22, 2001 issuance of receivable-

backed securities from the Trust, Statement of Financial Accounting

Standards (SFAS) No. 140 (which replaced SFAS No. 125 in its

entirety) became the accounting guidance applicable to such

transactions. Application of SFAS No. 140 resulted in secured

financing accounting for these transactions. This accounting

treatment results from the fact that the Trust is not a qualifying

special purpose entity under SFAS No. 140. While this accounting

requires secured financing treatment of the securities issued by the

Trust on our consolidated financial statements, the assets within

the Trust are still considered sold to our wholly owned, bankruptcy

remote subsidiary, TRC, and are not available to general creditors

of the Corporation.

Beginning on August 22, 2001, our consolidated financial

statements reflected the following accounting changes. First, we

reflected the obligation to holders of the $800 million (face value)

of previously sold receivable-backed securities (Series 1997-1 and

1998-1, Class A Certificates) as debt of TRC, and we recorded the

receivables at fair value in place of the previously recorded retained

interests related to the sold securities. This resulted in an unusual

pre-tax charge of $67 million ($.05 per share). Next, we reclassified

the owned receivable-backed securities to accounts receivable at

fair value. This reclassification had no impact on our consolidated

statements of operations because we had previously recorded

permanent impairments to our portfolio of owned receivable-backed

securities in amounts equal to the difference between face value

and fair value of the underlying receivables. On August 22, 2001,

the Trust’s entire portfolio of receivables was reflected on our

consolidated financial statements at its fair value, which was based

upon the expected performance of the underlying receivables

portfolio. At that point in time, fair value was equivalent in amount

to face value, net of an appropriate allowance. By the end of 2001,

a normalized relationship developed between the face value of

receivables and the allowance for doubtful accounts through

turnover of receivables within the portfolio. This process had no

impact on our consolidated financial statements. As a result, at

February 1, 2003 and at February 2, 2002, our allowance for doubtful

accounts is attributable to our entire receivables portfolio.

Prior to August 22, 2001, income on the receivable-backed

securities was accrued based on the effective interest rate applied

to its cost basis, adjusted for accrued interest and principal

paydowns. The effective interest rate approximates the yield on the

underlying receivables. We monitored impairment of receivable-

backed securities based on fair value. Permanent impairments were

charged to earnings through credit expense in the period in which

it was determined that the receivable-backed securities’ carrying

value was greater than their fair value. Permanent impairment

charges on the receivables underlying the receivable-backed

securities portfolio were $89 million in 2001 and $140 million in

2000. Permanent impairment charges in 2001 include only those

losses prior to the consolidation of our special purpose entity on

August 22, 2001.

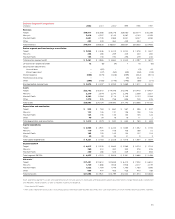

Inventory

We account for inventory and the related cost of sales under the

retail inventory accounting method using the last-in, first-out (LIFO)

basis. Inventory is stated at the lower of LIFO cost or market. The

cumulative LIFO provision was $52 million and $64 million at year-

end 2002 and 2001, respectively.

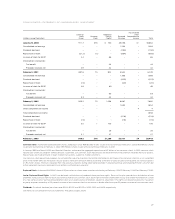

Inventory

February

1,

February

2,

(millions) 2003 2002

Target $3,748 $3,348

Mervyn’s 486 523

Marshall Field’s 324 348

Other 202 230

Total inventory $4,760 $4,449

Property and Equipment

Property and equipment are recorded at cost, less accumulated

depreciation. Depreciation is computed using the straight-line

method over estimated useful lives. Depreciation expense for the

years 2002, 2001 and 2000 was $1,183 million, $1,049 million and

$913 million, respectively. Accelerated depreciation methods are

generally used for income tax purposes.

Estimated useful lives by major asset category are as follows:

Asset Life (in years)

Buildings and improvements 8 – 50

Fixtures and equipment 4 – 8

Computer hardware and software 4

29