Target 2002 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2002 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

Measuring Value Creation

We measure value creation internally using a form of Economic

Value Added (EVA), which we define as after-tax segment profit

less a capital charge for all investment employed. The capital charge

is an estimate of our after-tax cost of capital adjusted for the age

of our stores, recognizing that mature stores inherently have higher

returns than newly opened stores. We estimate that the after-tax

cost of capital for our retail operations is approximately 9 percent,

while our credit card operations’ after-tax cost of capital is

approximately 5 percent as a result of their ability to support

higher debt levels. We expect to continue to generate returns in

excess of these costs of capital, thereby producing EVA.

EVA is used to evaluate our performance and to guide capital

investment decisions. A significant portion of executive incentive

compensation is tied to the achievement of targeted levels of annual

EVA generation. We believe that managing our business with a

focus on EVA helps achieve our objective of average annual earnings

per share growth of 15 percent or more over time. Earnings per

share before unusual items have grown at a compound annual rate

of 17 percent over the last five years.

Credit Card Operations

We offer credit to qualified guests in each of our business segments.

These credit card programs strategically support our core retail

operations and are an integral component of each business segment.

Our credit card products support earnings growth by driving sales

at our stores and through growth in credit card financial

performance. In addition to our proprietary credit card programs

that have been offered for many years, we began a national rollout

of the Target Visa credit card during 2001.

The following tables reflect the financial performance of our

credit card operations on a managed portfolio basis. Pre-tax credit

contribution reflects pre-tax profit before funding costs. See

discussion on Accounting for Accounts Receivable on page 19 for

additional information on the treatment of securitized receivables

in our consolidated financial statements.

The revenue from accounts receivable represents revenues

derived from finance charges, late fees and other revenues.

Intracompany merchant fees are fees charged to our retail

operations on a basis similar to fees charged by third-party credit

card issuers. These fees are eliminated in consolidation. Third-party

merchant fees are fees paid to us by merchants that have accepted

the Target Visa credit card, and are included in net credit card

revenues. Credit card expenses include marketing and account

service activities that support our credit card portfolio, as well as

bad debt expense.

In 2002, pre-tax contribution from credit card operations

increased approximately 20 percent over the prior year. This

performance was driven primarily by the substantial growth in

average receivables due to increases in the issuance and usage of

the Target Visa credit card.

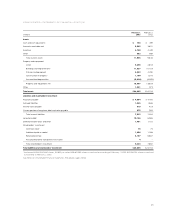

Credit Card Contribution to Segment Profit

(millions) 2002 2001 2000

Revenues:

Finance charges, late

fees and other revenues $1,126 $ 779 $ 653

Merchant fees

Intracompany 102 102 99

Third-party 69 18 1

Total revenues 1,297 899 753

Expenses:

Bad debt provision 460 230 148

Operations and marketing 305 224 205

Total expenses 765 454 353

Pre-tax credit card contribution $ 532 $ 445 $ 400

Receivables

(millions) 2002 2001 2000

Target

Target Visa $3,774 $1,567 $ 76

Guest Card 827 1,063 1,325

Mervyn’s 626 706 735

Marshall Field’s 737 756 769

Total year-end

receivables*$5,964 $4,092 $2,905

Delinquent receivables** 3.8% 3.2% 3.9

%

Total average receivables $4,841 $3,016 $2,604

*At year-end 2000, balance includes $800 million of publicly held

receivable-backed securities (see discussion under Accounting for

Accounts Receivable on page 19).

** Balances on accounts that are delinquent by 60 days or more as a percent

of total year-end receivables.

Allowance for Doubtful Accounts

(millions) 2002 2001 2000

Allowance at beginning of year $ 261 $ 211 $ 203

Bad debt provision 460 230 148

Net write-offs (322) (180) (140)

Allowance at end of year $ 399 $ 261 $ 211

As a percent of year-end receivables 6.7

%

6.4

%

7.3

%

22

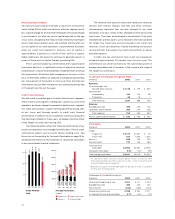

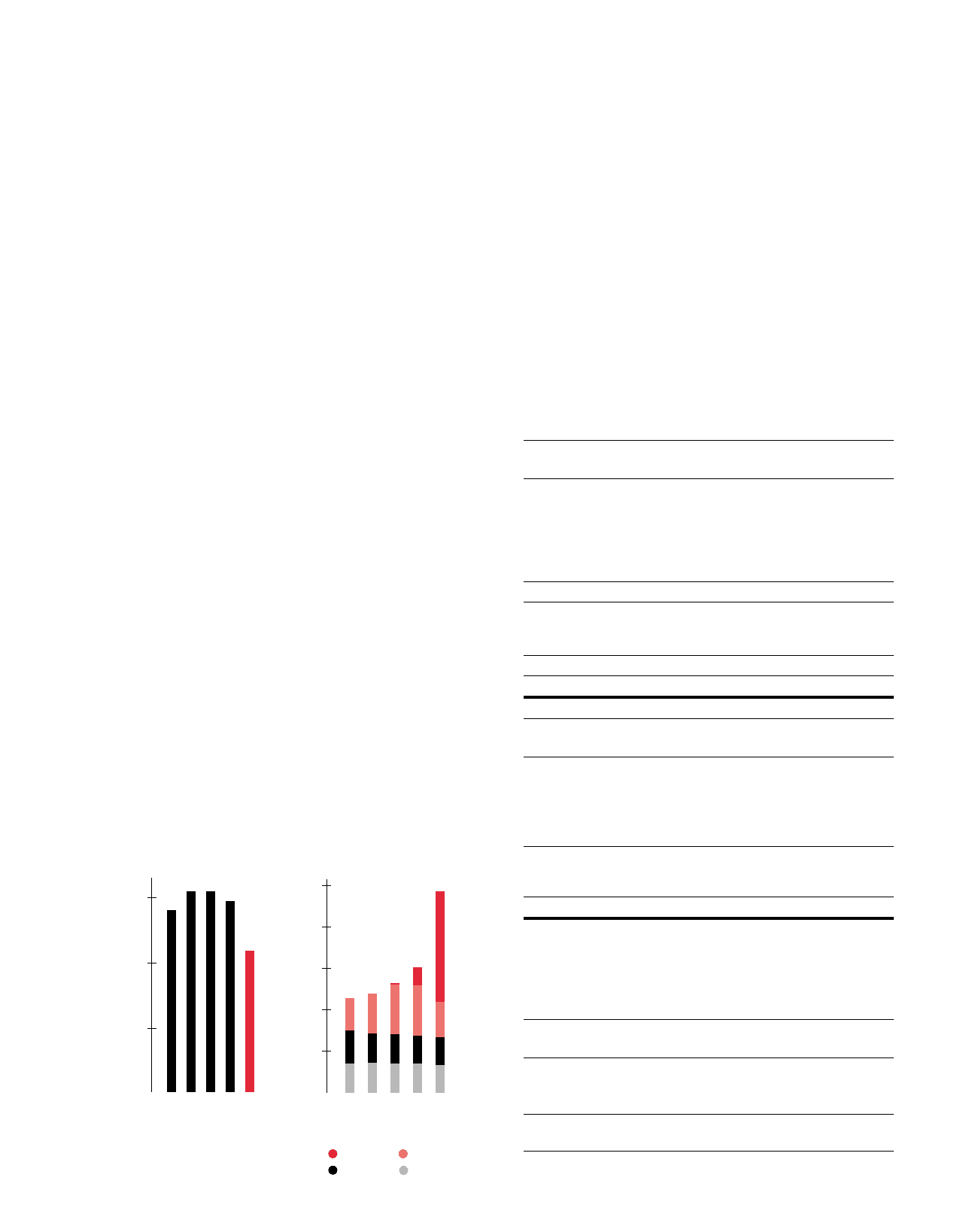

$764 $803$720

$719 $718 $974

Average Receivables

(millions)

Target Visa Target Guest Card

Mervyn’s Marshall Field’s

’98 ’99 ’00 ’01 ’02

$725 $697 $1,169 $13

$725 $673 $1,218 $400

$706 $620 $880 $2,635

5,000

4,000

3,000

2,000

1,000

15.4%

Credit Portfolio

Yield

’98 ’99 ’00 ’01 ’02

14.0%

15.4%

14.7%

11.0%

15%

10%

5%