Target 2002 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2002 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

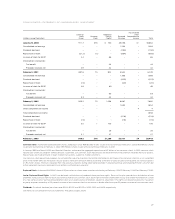

|

|

Number of Stores

February 2, February1,

2002

Opened

Closed 2003

Target 1,053 114 20 1,147

Mervyn’s 264 1 1 264

Marshall Field’s 64 0 0 64

Total 1,381 115 21 1,475

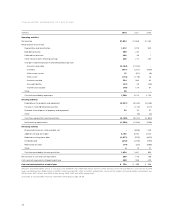

Other capital investments were for information system

hardware and software, distribution capacity and other infrastructure

to support store growth, primarily at Target.

In January 1999 and March 2000, our Board of Directors

authorized the aggregate repurchase of $2 billion of our common

stock. Since that time, we have repurchased a total of 41 million

shares of our common stock at a total cost of $1,199 million ($29.27

per share), net of the premium from exercised and expired put

options. In 2001, common stock repurchases were essentially

suspended. Consequently, common stock repurchases did not

have a material impact on our 2002 or 2001 net earnings and

financial position.

Our financing strategy is to ensure liquidity and access to

capital markets, to manage the amount of floating-rate debt and

to maintain a balanced spectrum of debt maturities. Within these

parameters, we seek to minimize our cost of borrowing.

A key to our access to liquidity and capital markets is

maintaining strong investment-grade debt ratings.

Credit Ratings

Standard

Moody’s and Poor’s Fitch

Long-term debt A2 A+ A

Commercial paper P-1 A-1 F1

Securitized receivables Aaa AAA N/A

We view interest coverage and debt ratio as important

indicators of our creditworthiness. In 2002, interest coverage

continued to improve to 5.1x and debt ratio remained constant at

52 percent.

Interest Coverage and Debt Ratio

2002 2001 2000

Interest coverage 5.1x 4.7x 4.4x

Debt ratio 52% 52% 52%

Interest coverage and debt ratio include the impact of any publicly held

receivable-backed securities and off-balance sheet operating leases as if

they were debt. Interest coverage represents the ratio of pre-tax earnings

before unusual items and fixed charges to fixed charges (interest expense

excluding loss on debt repurchase, interest equivalent and the interest portion

of rent expense). Debt ratio represents the ratio of debt (debt and debt

equivalents less cash equivalents) to total capitalization, including debt,

deferred income taxes and other, and shareholders’ investment.

Further liquidity is provided by $1.9 billion of committed lines

of credit obtained through a group of 30 banks. Of these credit

lines, a $1.1 billion credit facility matures in June 2003 but includes

a one-year term-out option to June 2004. The remaining $800

million credit facility matures in June 2005. There were no balances

outstanding at any time during 2002 or 2001 under these

agreements. No debt instrument contains provisions requiring

acceleration of payment upon a debt rating downgrade.

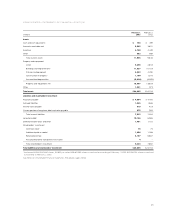

Commitments and Contingencies

At February 1, 2003, our debt and lease contractual obligations

were as follows:

Payments Due by Period

(millions) Less than 1-3 3-5 After 5

Contractual Obligations Total 1 Year Years Years Years

Long-term debt*$10,890 $ 965 $1,359 $2,075 $6,491

Capital lease

obligations** 244 21 39 36 148

Operating leases** 1,528 147 265 208 908

Total contractual

cash obligations $12,662 $1,133 $1,663 $2,319 $7,547

*Required principal payments only. Excludes SFAS No. 133, “Accounting for

Derivative Instruments and Hedging Activities,” adjustments recorded in

long-term debt.

**Total contractual lease payments.

Commitments for the purchase, construction, lease or

remodeling of real estate, facilities and equipment were

approximately $509 million at year-end 2002.

We are exposed to claims and litigation arising out of the

ordinary course of business. Management, after consulting with

legal counsel, believes the currently identified claims and litigation

will not have a material adverse effect on our results of operations

or our financial condition taken as a whole.

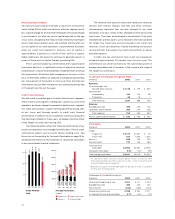

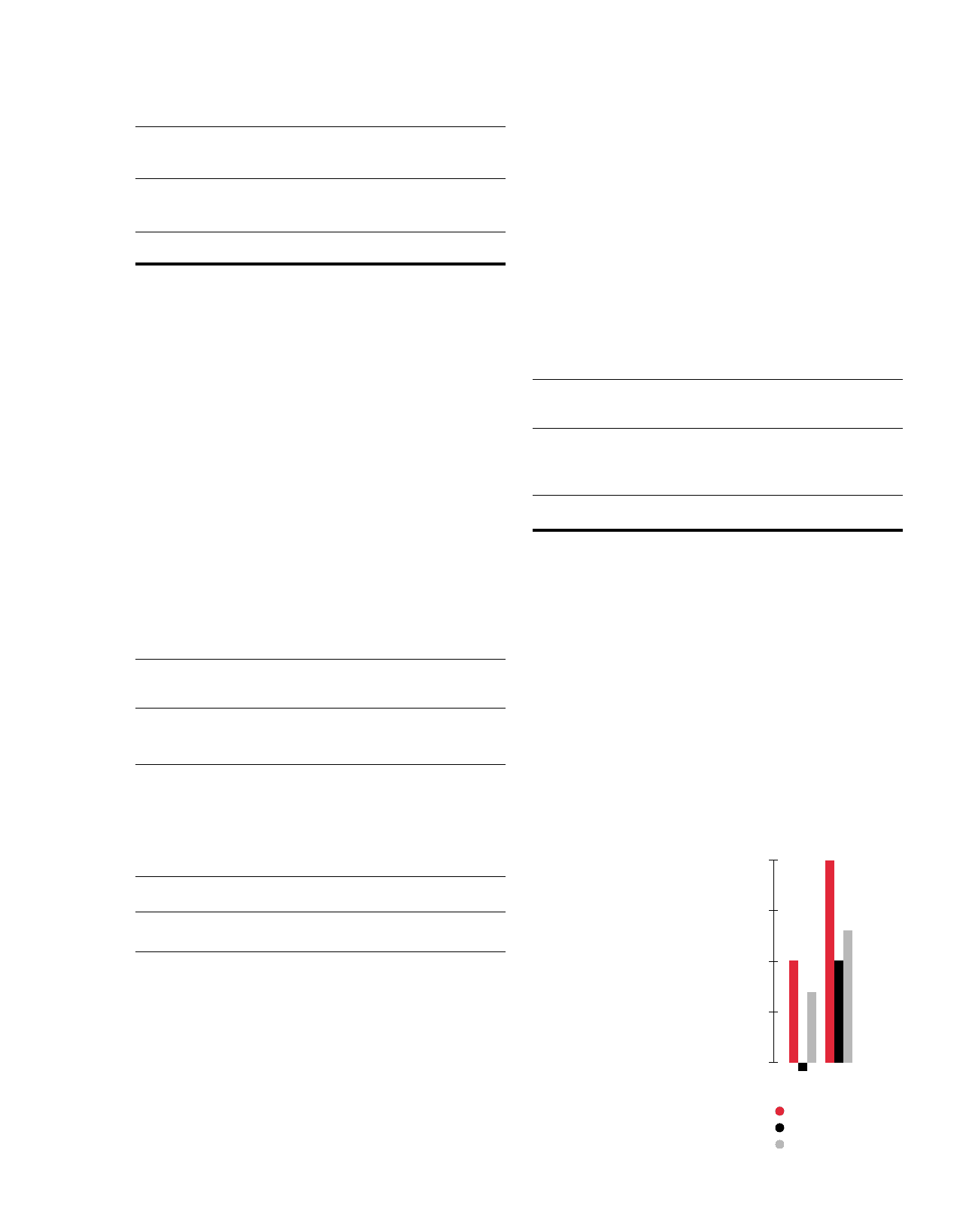

Performance Objectives

Shareholder Return

Our primary objective is to maxi-

mize shareholder value over time

through a combination of share

price appreciation and dividend

income while maintaining a

prudent and flexible capital

structure. Our total return to

shareholders (including reinvested

dividends) over the last five years

averaged 10.2 percent annually,

returning about $162 for each $100

invested in our stock at the

beginning of this period.

21

10%

-1%

7%

Total Annualized Return

Target

S&P 500

Proxy peer group

5Year 10Year

20%

10%

13%

20

15

10

5

0