Target 2002 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2002 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

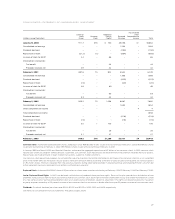

called or repurchased $144 million and $35 million of debt,

respectively, which resulted in losses of $9 million ($.01 per share)

and $5 million (less than $.01 per share), respectively. Also in 2000,

$371 million of puttable debt was put to us, resulting in a gain of

$4 million (less than $.01 per share).

In April 2002, the Financial Accounting Standards Board issued

Statement of Financial Accounting Standards (SFAS) No. 145,

“Rescission of FASB Statements No. 4, 44 and 64, Amendment of

FASB Statement No. 13, and Technical Corrections.” We elected to

early adopt this Statement in the first quarter of 2002. Previously,

all gains and losses from the early extinguishment of debt were

required to be aggregated and classified as an extraordinary item

in the Consolidated Results of Operations, net of the related tax

effect. Under SFAS No. 145, gains and losses from the early

extinguishment of debt are included in interest expense. Prior year

extraordinary items have been reclassified to reflect this change.

The adoption of SFAS No. 145 had no impact on current year or

previously reported net earnings, cash flows or financial position.

Accounting for Accounts Receivable

On August 22, 2001, Target Receivables Corporation (TRC) sold,

through the Target Credit Card Master Trust (the Trust), $750 million

of receivable-backed securities to the public. Prior to this transaction,

the accounting guidance applicable to our receivable-backed

securities transactions was SFAS No. 125, “Accounting for Transfers

and Servicing of Financial Assets and Extinguishments of Liabilities,”

resulting in sale accounting treatment. Concurrent with this

transaction, SFAS No. 140 (which replaced SFAS No. 125 in its

entirety) became the applicable accounting guidance. Application

of SFAS No. 140 resulted in secured financing accounting for all

outstanding transactions. This new accounting treatment results

from the fact that the Trust is not a qualifying special purpose entity

under SFAS No. 140.

Beginning on August 22, 2001, our consolidated financial

statements reflected the consolidation of these outstanding

obligations. We reflected the obligation to holders of the $800

million (face value) of previously sold receivable-backed securities

(Series 1997-1 and 1998-1, Class A Certificates) as debt of TRC, and

we recorded the receivables at fair value in place of the previously

recorded retained interests related to the sold securities. This resulted

in an unusual pre-tax charge of $67 million ($.05 per share) in 2001.

Our Consolidated Results of Operations did not include finance

charge revenues or loss provision related to the publicly held

receivable-backed securities until August 22, 2001. Payments

accrued to holders of our publicly held receivable-backed securities

prior to August 22, 2001 are included in our Pre-tax Earnings

Reconciliation on page 35 as interest equivalent. Interest equivalent

was $27 million in 2001 and $50 million in 2000.

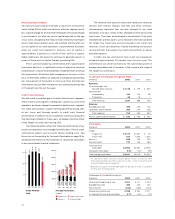

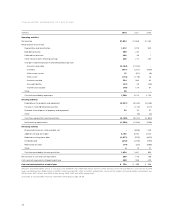

Fourth Quarter Results

Due to the seasonal nature of our business, fourth quarter operating

results typically represent a substantially larger share of total

year revenues and earnings due to the inclusion of the holiday

shopping season.

Fourth quarter 2002 net earnings were $688 million, compared

with $658 million in 2001. Earnings per share were $.75 for the

quarter, compared with $.72 in 2001. Total revenues increased 6.4

percent and 13-week comparable-store sales decreased 2.2 percent.

Our pre-tax segment profit increased 1.4 percent to $1,291 million,

driven by growth at Target, partially offset by declines at Mervyn’s

and Marshall Field’s.

Fourth Quarter Pre-tax Segment Profit and

Percent Change from Prior Year

(millions) 2002 2001 2000

Target $1,165 8.0% $1,078 20.9% $ 892 10.0%

Mervyn’s 75 (42.9) 131 20.8 108 57.7

Marshall Field’s 51 (18.9) 63 (20.2) 79 (34.4)

Total $1,291 1.4% $1,272 17.9% $1,079 7.9%

Net earnings $ 688 4.4% $ 658 19.3% $ 552 11.8%

Critical Accounting Estimates

Our analysis of operations and financial condition are based upon

our consolidated financial statements, which have been prepared

in accordance with GAAP. The preparation of these financial

statements requires us to make estimates and assumptions that

affect the reported amounts of assets and liabilities at the date of

the financial statements, the reported amounts of revenues and

expenses during the reporting period, and the related disclosures

of contingent assets and liabilities. In the Notes to Consolidated

Financial Statements, we describe our significant accounting policies

used in the preparation of the consolidated financial statements.

We evaluate our estimates on an ongoing basis. We base our

estimates on historical experience and on various other assumptions

that we believe to be reasonable under the circumstances. Actual

results could differ from these estimates under different assumptions

or conditions.

The following items in our consolidated financial statements

require significant estimation or judgment:

Inventory and cost of sales We account for inventory and the

related cost of sales under the retail inventory method using the

LIFO basis. Under the retail inventory method, inventory is stated

at cost, which is determined by applying a cost-to-retail ratio to

each similar merchandise grouping’s ending retail value. Since this

inventory value is adjusted regularly to reflect market conditions,

our inventory methodology reflects the lower of cost or market. We

also reduce inventory for estimated losses related to shortage, based

upon historical losses verified by prior physical inventory counts.

19