Target 2002 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2002 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

|

|

30

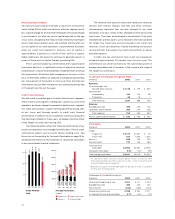

In 2001, the Financial Accounting Standards Board (FASB)

issued SFAS No. 144, “Accounting for the Impairment or Disposal

of Long-Lived Assets,” superseding SFAS No. 121 in its entirety and

the accounting and reporting provisions of Accounting Principles

Board (APB) Opinion No. 30 for disposals of segments of a business.

The statement retains the fundamental provisions of SFAS No. 121,

clarifies guidance related to asset classification and impairment

testing and incorporates guidance related to disposals of segments.

As required, we adopted SFAS No. 144 in the first quarter of

2002. All long-lived assets are reviewed when events or changes

in circumstances indicate that the carrying value of the asset may

not be recoverable. We review most assets at a store level basis,

which is the lowest level of assets for which there are identifiable

cash flows. The carrying amount of the store assets are compared

to the related expected undiscounted future cash flows to be

generated by those assets over the estimated remaining useful life

of the primary asset. Cash flows are projected for each store based

upon historical results and expectations. In cases where the expected

future cash flows and fair value are less than the carrying amount

of the assets, those stores are considered impaired and the assets

are written down to fair value. Fair value is based on appraisals or

other reasonable methods to estimate value. In 2002, impairment

losses are included in depreciation expense and resulted in a financial

statement impact of less than $.01 per share.

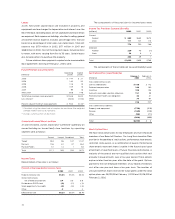

Goodwill and Intangible Assets

In 2001, the FASB issued SFAS No. 142, “Goodwill and Other

Intangible Assets,” which supersedes APB Opinion No. 17, “Intangible

Assets.” Under the new statement, goodwill and intangible assets

that have indefinite useful lives are no longer amortized but rather

reviewed at least annually for impairment. As required, we adopted

this statement in the first quarter of 2002. The adoption of this

statement reduced annual amortization expense by approximately

$10 million ($.01 per share). At February 1, 2003 and February 2,

2002, net goodwill and intangible assets were $376 million and

$250 million, respectively, including $155 million of goodwill and

intangible assets with indefinite useful lives in both years.

Goodwill and intangible assets are recorded within other long-

term assets at cost less accumulated amortization. Amortization is

computed on intangible assets with definite useful lives using the

straight-line method over estimated useful lives that range from

three to 15 years. Amortization expense for the years 2002, 2001

and 2000 was $29 million, $30 million and $27 million, respectively.

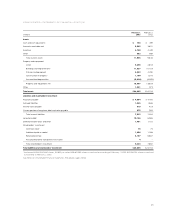

Accounts Payable

Outstanding drafts included in accounts payable were $1,125 million

and $958 million at year-end 2002 and 2001, respectively.

Lines of Credit

At February 1, 2003, two committed credit agreements totaling

$1.9 billion were in place through a group of 30 banks at specified

rates. There were no balances outstanding at any time during 2002

or 2001 under these agreements.

Commitments and Contingencies

At February 1, 2003, our obligations included notes payable, notes

and debentures of $11,017 million (discussed in detail under Long-

term Debt and Notes Payable on page 31) and the present value of

capital and operating lease obligations of $144 million and $924

million, respectively (discussed in detail under Leases on page 32).

In addition, commitments for the purchase, construction, lease

or remodeling of real estate, facilities and equipment were

approximately $509 million at year-end 2002.

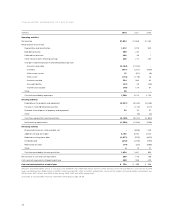

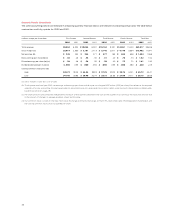

In July 2001, the FASB issued SFAS No. 143, “Accounting for

Asset Retirement Obligations.” SFAS No. 143 addresses the

accounting and reporting for obligations associated with the

retirement of tangible long-lived assets and the associated asset

retirement cost. SFAS No. 143 is effective for financial statements

issued for fiscal years beginning after June 15, 2002. The adoption

of SFAS No. 143 in the first quarter of 2003 will not have an impact

on current year or previously reported net earnings, cash flows or

financial position.

In July 2002, the FASB issued SFAS No. 146, “Accounting for

Costs Associated with Exit or Disposal Activities.” The provisions

of SFAS No. 146 are effective for exit or disposal activities that are

initiated after December 31, 2002. SFAS No. 146 requires that a

liability for a cost associated with an exit or disposal activity be

recognized when the liability is incurred instead of recognizing the

liability at the date of commitment to an exit plan as was previously

allowed. The adoption of SFAS No. 146 will not have an impact on

current year or previously reported net earnings, cash flows or

financial position.

We are exposed to claims and litigation arising out of the

ordinary course of business. Management, after consulting with

legal counsel, believes the currently identified claims and litigation

will not have a material adverse effect on our results of operations

or our financial condition taken as a whole.