Target 2002 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2002 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44

|

|

pension expense. We expect lower future expenses as a result of

these transactions because they were designed to be economically

neutral or slightly favorable to us.

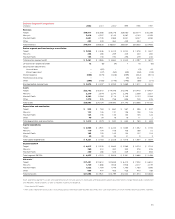

Pension and Postretirement Health Care Benefits

We have qualified defined benefit pension plans that cover all

employees who meet certain age, length of service and hours

worked per year requirements. We also have unfunded non-qualified

pension plans for employees who have qualified plan compensation

restrictions. Benefits are provided based upon years of service and

the employee’s compensation. Retired employees also become

eligible for certain health care benefits if they meet minimum age

and service requirements and agree to contribute a portion of the

cost. Additionally, as described above, certain non-qualified pension

and survivor benefits owed to current executives were exchanged

for deferrals in an existing non-qualified defined contribution

employee benefit plan.

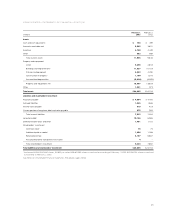

Change in Benefit Obligation

Pension Benefits Postretirement

Qualified Non-qualified Health Care

Plans Plans Benefits

(millions) 2002 2001 2002 2001 2002 2001

Benefit obligation

at beginning of

measurement period

$1,014 $ 863 $ 53 $ 54 $114 $ 99

Service cost

57 48 1222

Interest cost

72 65 3488

Actuarial (gain)/loss

59 88 –9214

Benefits paid

(50) (50) (5) (16) (10) (9)

Plan amendments

(74) –––––

Settlement

––(29) –––

Benefit obligation at end of

measurement period

$1,078 $1,014 $ 23 $ 53 $116 $114

Change in Plan Assets

Fair value of plan assets

at beginning of

measurement period

$1,033 $1,020 $ – $ – $ – $ –

Actual return on

plan assets

(79) (100) ––––

Employer contribution

154 163 516 10 9

Benefits paid

(50) (50) (5) (16) (10) (9)

Fair value of plan

assets at end of

measurement period

$1,058 $1,033 $ – $ – $ – $ –

Reconciliation of Prepaid/(Accrued) Cost

Funded status

$ (20) $ 19 $(23) $(53) $(116) $(114)

Unrecognized actuarial

loss/(gain)

530 292 621 711

Unrecognized prior

service cost

(73) 13712

Net prepaid/(accrued) cost

$437 $312 $(14) $(25) $(108) $(101)

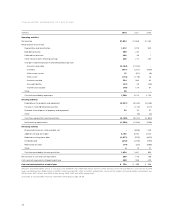

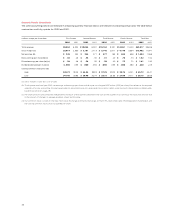

Net Pension and Postretirement Health Care

Benefits Expense

Postretirement

Pension Benefits HealthCare Benefits

(millions) 2002 2001 2000 2002 2001 2000

Service cost benefits

earned during the

period $58 $50 $47 $ 2 $ 2 $2

Interest cost on

projected benefit

obligation 75 69 63 88 7

Expected return

on assets (108) (89) (81) 1– –

Recognized gains

and losses 10 1 8 –– –

Recognized prior

service cost 11 1 –– –

Settlement/curtailment

charges (12) – – –– –

Total $24 $32 $38 $11 $10 $9

The amortization of any prior service cost is determined using

a straight-line amortization of the cost over the average remaining

service period of employees expected to receive benefits under

the plan.

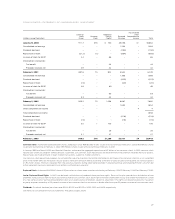

Actuarial Assumptions

Postretirement

Pension Benefits HealthCare Benefits

2002 2001 2000 2002 2001 2000

Discount rate 7

%

71⁄4

%

73⁄4

%

7

%

71⁄4

%

73⁄4

%

Expected long-term

rate of return on

plans’ assets 99 9 n/a n/a n/a

Average assumed

rate of compensation

increase 441⁄443⁄4n/a n/a n/a

Our rate of return on qualified plans’ assets has averaged

3.7 percent and 9.3 percent per year over the 5-year and 10-year

periods ending October 31, 2002 (our measurement date). After

that date, we reduced our expected long-term rate of return on

plans’ assets to 81

⁄

2percent per year.

An increase in the cost of covered health care benefits of 6.0

percent is assumed for 2003. The rate is assumed to remain at 6.0

percent in the future. The health care cost trend rate assumption

may have a significant effect on the amounts reported.

A one percent change in assumed health care cost trend rates

would have the following effects:

1% Increase 1% Decrease

Effect on total of service and

interest cost components

of net periodic postretirement

health care benefit cost $– $ –

Effect on the health care component

of the postretirement benefit

obligation $5 $(5)

34