Target 2002 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2002 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

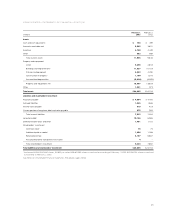

Additionally, we reduce inventory for estimates of vendor allowances,

such as rebates, volume allowances, shelving/slotting allowances

and exclusivity allowances. Vendor allowances are recognized in

the financial statements when we have fulfilled our performance

obligations. Inventory also includes a LIFO provision that is calculated

based on inventory levels, markup rates and internally generated

retail price indices.

Allowance for doubtful accounts When receivables are recorded,

an allowance for doubtful accounts in an amount equal to

anticipated future write-offs is recognized. The estimated future

write-offs are based on historical experience and other factors. The

allowance for doubtful accounts was $399 million or 6.7 percent of

year-end receivables at February 1, 2003, compared to $261 million

or 6.4 percent of year-end receivables at February 2, 2002.

Pension and postretirement health care accounting We fund and

maintain three qualified defined benefit pension plans and maintain

certain non-qualified plans as well. Our pension costs are determined

based on actuarial calculations using key assumptions including our

expected long-term rate of return on qualified plan assets, discount

rate and our estimate of future compensation increases. We also

maintain a postretirement health care plan for certain retired

employees. Postretirement health care costs are calculated based

on actuarial calculations using key assumptions including a discount

rate and health care cost trend rates. Our pension and postretirement

health care benefits are further described in the Notes to

Consolidated Financial Statements on page 34.

Insurance/self-insurance We retain a portion of the risk related to

certain general liability, workers’ compensation, property loss and

employee medical and dental claims. Liabilities associated with

these losses are calculated for claims filed, and claims incurred but

not yet reported, at our estimate of their ultimate cost, based upon

analysis of historical data and actuarial estimates. General liability

and workers’ compensation liabilities are then recorded at their net

present value. Our expected loss accruals are based on estimates,

and while we believe the amounts accrued are adequate, the

ultimate loss may differ from the amounts provided. We maintain

stop-loss coverage to limit the exposure related to certain risks.

Income taxes We pay income taxes based on the tax statutes,

regulations and case law of the various jurisdictions in which we

operate. Our effective income tax rate was 38.2 percent, 38.0 percent

and 38.4 percent in 2002, 2001 and 2000, respectively. The income

tax provision includes estimates for certain unresolved matters in

dispute with state and federal tax authorities.

Analysis of Financial Condition

Our financial condition remains

strong. Cash flow provided by

operations was $1,590 million in

2002, driven by net income before

depreciation and amortization

expense and is net of our

substantial growth in accounts

receivable. Internally generated

cash, along with our ability to

access a variety of financial

markets, provides capital for our

expansion plans. We expect to

continue to fund the growth in our

business through a combination

of internally generated funds

and debt.

During 2002, our total gross year-end receivables (which

includes all securitized receivables) increased 46 percent, or

$1,872 million, to $5,964 million. The growth in year-end receivables

was driven by continued growth in issuance and usage of the

Target Visa credit card. Average total receivables increased 61 percent

from 2001.

During 2002, inventory levels increased $311 million, or

7.0 percent. This growth was more than fully funded by the

$524 million increase in accounts payable over the same period.

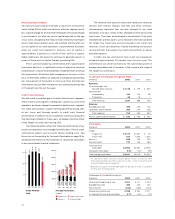

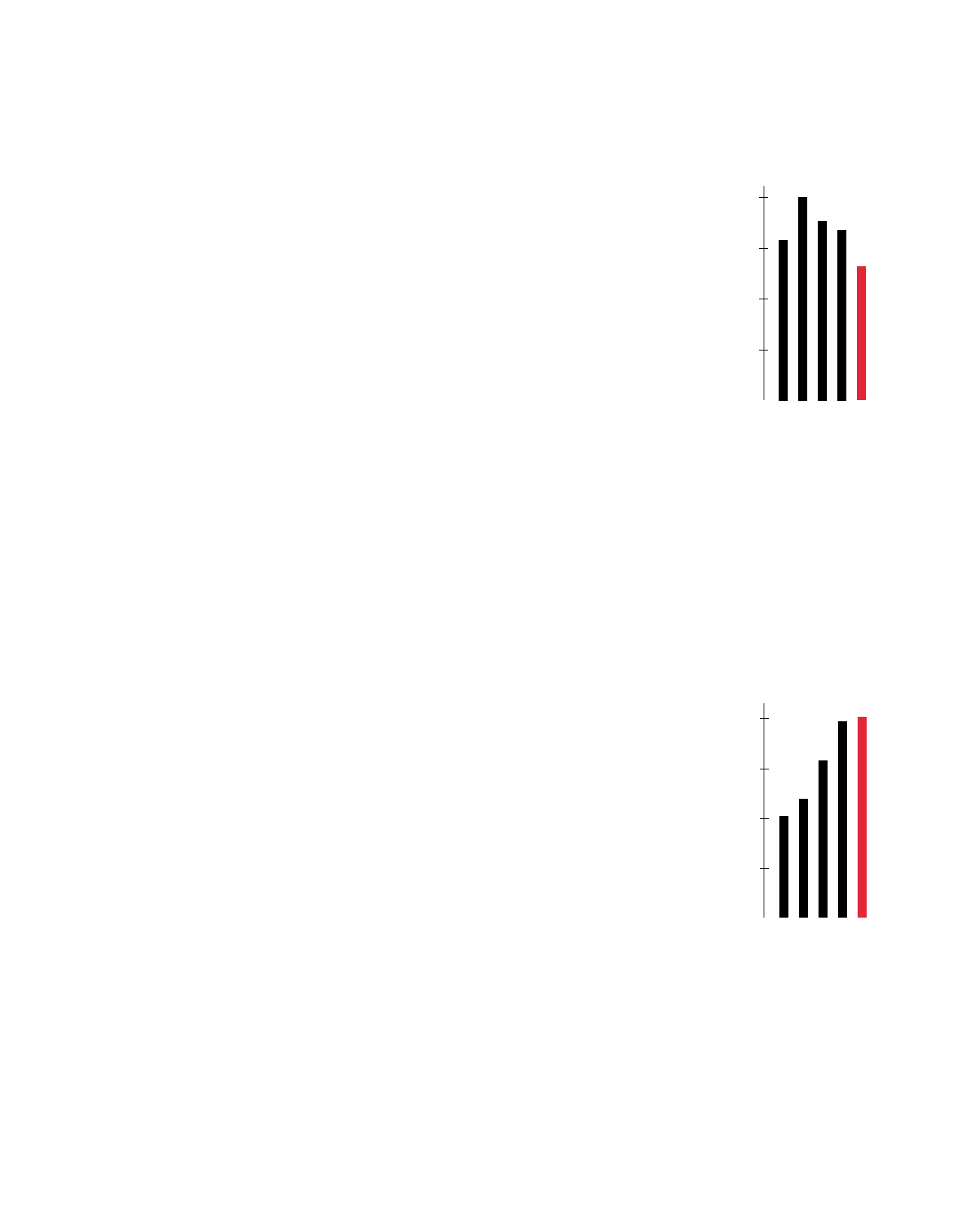

Capital expenditures were

$3,221 million in 2002, compared

with $3,163 million in 2001 and

$2,528 in 2000. Investment in

Target accounted for 92 percent of

capital expenditures in both 2002

and 2001, and 89 percent in 2000.

Net property and equipment

increased $1,774 million in 2002,

compared with an increase of

$2,115 in 2001. Over the past five

years, Target’s net retail square

footage has grown at a com-

pound annual rate of 10 percent,

consistent with our objective to

expand Target’s square footage

in the range of 8 to 10 percent

annually.

Approximately 66 percent of total expenditures in 2002 were

for new stores, expansions and remodels.

20

$1,918

Capital

Expenditures

(millions)

’98 ’99 ’00 ’01 ’02

$1,657

$2,528

$3,163

$3,221

3,200

2,400

1,600

800

$2,403

Cash Flow from

Operations

(millions)

’98 ’99 ’00 ’01 ’02

$1,891

$2,134

$2,012

$1,590

2,400

1,800

1,200

600