Target 2002 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2002 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

|

|

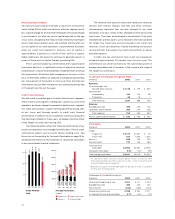

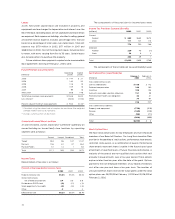

Long-term Debt and Notes Payable

At February 1, 2003 and February 2, 2002, $100 million of notes

payable were outstanding, representing financing secured by the

Target Credit Card Master Trust Series 1996-1 Class A variable funding

certificate. This certificate is debt of TRC and is classified in the

current portion of long-term debt and notes payable. The average

amount of secured and unsecured notes payable outstanding during

2002 was $170 million at a weighted average interest rate of

1.9 percent. The average amount of secured and unsecured notes

payable outstanding during 2001 was $658 million at a weighted

average interest rate of 4.4 percent.

In 2002, we issued $750 million of long-term debt maturing in

2009 at 5.38 percent, $1 billion of long-term debt maturing in 2012

at 5.88 percent, and $600 million of long-term debt maturing in

2032 at 6.35 percent. Also during 2002, the Trust issued $750 million

of floating rate debt secured by credit card receivables, bearing

interest at an initial rate of 1.99 percent maturing in 2007. We also

called or repurchased $266 million of long-term debt with an

average remaining life of 19 years and a weighted average interest

rate of 8.8 percent, resulting in a loss of $34 million ($.02 per share).

In 2001, we issued $550 million of long-term debt maturing in

2006 at 5.95 percent, $500 million of long-term debt maturing in

2007 at 5.50 percent, $750 million of long-term debt maturing in

2008 at 5.40 percent, and $700 million of long-term debt maturing

in 2031 at 7.00 percent. The Trust issued $750 million of floating

rate debt secured by credit card receivables, bearing interest at an

initial rate of 3.69 percent maturing in 2004. In addition, concurrent

with this transaction, on August 22, 2001 we reflected the obligation

to holders of the $800 million in previously sold receivable-backed

securities as debt of TRC (discussed in detail under Accounts

Receivable and Receivable-backed Securities on page 29). Also

during 2001, we called or repurchased $144 million of long-term

debt with an average remaining life of 7 years and a weighted

average interest rate of 9.2 percent, resulting in a loss of $9 million

($.01 per share).

Subsequent to year-end 2002, we issued $500 million of long-

term debt maturing in 2008 at 3.4 percent.

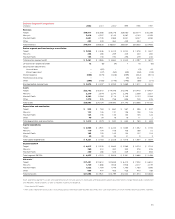

At year-end our debt portfolio was as follows:

Long-term Debt and Notes Payable

February 1, 2003 February 2, 2002

(millions) Rate*Balance Rate*Balance

Notes payable 1.4% $ 100 1.8% $ 100

Notes and debentures:

Due 2002-2006 3.7 3,072 4.0 3,806

Due 2007-2011 5.1 4,572 6.5 3,056

Due 2012-2016 6.0 1,060 9.4 27

Due 2017-2021 9.4 155 9.6 194

Due 2022-2026 8.0 358 8.2 557

Due 2027-2031 6.9 1,100 6.9 1,100

Due 2032 6.4 600 – –

Total notes payable,

notes and debentures** 5.2% $11,017 5.6% $8,840

Capital lease obligations 144 153

Less: current portion (975) (905)

Long-term debt and

notes payable $10,186 $8,088

*Reflects the weighted average stated interest rate as of year-end, including

the impact of interest rate swaps.

** The estimated fair value of total notes payable and notes and debentures,

using a discounted cash flow analysis based on our incremental interest

rates for similar types of financial instruments, was $11,741 million at

February 1, 2003 and $9,279 million at February 2, 2002.

Required principal payments on long-term debt and notes

payable over the next five years, excluding capital lease obligations,

are $965 million in 2003, $857 million in 2004, $502 million in 2005,

$752 million in 2006 and $1,323 million in 2007.

Derivatives

At February 1, 2003 and February 2, 2002, interest rate swap

agreements were outstanding in notional amounts totaling $1,450

million in both years. The swaps hedge the fair value of certain debt

by effectively converting interest from fixed rate to variable. During

the year, we entered into and terminated an interest rate swap with

a notional amount of $500 million. We also entered into an interest

rate swap with a notional amount of $400 million, and an interest

rate swap with a notional amount of $400 million matured. Any

hedge ineffectiveness related to our swaps is recognized in interest

expense. We have previously entered into rate lock agreements to

hedge the exposure to variability in future cash flows of forecasted

debt transactions. When the transactions contemplated by these

agreements occurred, the gain or loss was recorded as a component

of other comprehensive income and will be reclassified into earnings

in the periods during which the designated hedged cash flows affect

earnings. The fair value of our outstanding derivatives was $110

million and $44 million at February 1, 2003 and February 2, 2002,

respectively. These amounts are reflected in the Consolidated

Statements of Financial Position. Cash flows from hedging

transactions are classified consistent with the item being hedged.

31