Verizon Wireless 2007 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2007 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

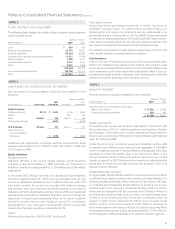

Notes to Consolidated Financial Statements continued

47

Employee Benefit Plans

Pension and postretirement health care and life insurance benefits earned

during the year as well as interest on projected benefit obligations are

accrued currently. Prior service costs and credits resulting from changes

in plan benefits are amortized over the average remaining service period

of the employees expected to receive benefits. Expected return on plan

assets is determined by applying the return on assets assumption to the

market-related value of assets.

As of July 1, 2006, Verizon management employees no longer earn

pension benefits or earn service towards the company retiree medical

subsidy (see Note 15).

In September 2006, the FASB issued SFAS No. 158, Employers’ Accounting

for Defined Benefit Pension and Other Postretirement Plans—an amendment

of FASB Statements No. 87, 88, 106, and 132(R) (SFAS No. 158). Effective

December 31, 2006, SFAS No. 158 requires the recognition of a defined

benefit postretirement plan’s funded status as either an asset or liability

on the balance sheet. SFAS No. 158 also requires the immediate recog-

nition of the unrecognized actuarial gains and losses and prior service

costs and credits that arise during the period as a component of other

accumulated comprehensive income, net of applicable income taxes.

Additionally, the fair value of plan assets must be determined as of the

Company’s year-end. We adopted SFAS No. 158 effective December

31, 2006, which resulted in a net decrease to shareowners’ investment

of $7,409 million. This included a net increase in pension obligations of

$2,007 million, an increase in Other Postretirement Benefits Obligations

of $10,828 million and an increase in Other Employee Benefit Obligations

of $31 million, offset by an increase in deferred taxes of $5,457 million.

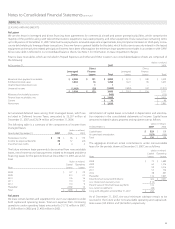

Derivative Instruments

We have entered into derivative transactions to manage our exposure to

fluctuations in foreign currency exchange rates, interest rates and com-

modity prices. We employ risk management strategies using a variety

of derivatives including foreign currency forwards and collars, equity

options, interest rate and commodity swap agreements and interest rate

locks. We do not hold derivatives for trading purposes.

In accordance with SFAS No. 133, Accounting for Derivative Instruments

and Hedging Activities (SFAS No. 133) and related amendments and inter-

pretations, we measure all derivatives, including derivatives embedded

in other financial instruments, at fair value and recognize them as either

assets or liabilities on our consolidated balance sheets. Changes in the fair

values of derivative instruments not qualifying as hedges or any ineffec-

tive portion of hedges are recognized in earnings in the current period.

Changes in the fair values of derivative instruments used effectively as fair

value hedges are recognized in earnings, along with changes in the fair

value of the hedged item. Changes in the fair value of the effective por-

tions of cash flow hedges are reported in other comprehensive income

(loss) and recognized in earnings when the hedged item is recognized

in earnings.

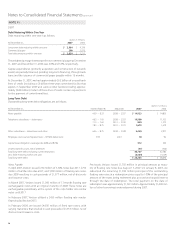

Recent Accounting Pronouncements

In December 2007, the FASB issued SFAS No. 141(R), Business Combinations

(Revised), (SFAS No. 141(R)), to replace SFAS No. 141, Business Combinations.

SFAS No. 141(R) requires the use of the acquisition method of accounting,

defines the acquirer, establishes the acquisition date and broadens the

scope to all transactions and other events in which one entity obtains

control over one or more other businesses. This statement is effective

for business combinations or transactions entered into for fiscal years

beginning on or after December 15, 2008. We are still evaluating the

impact of SFAS No. 141(R), however, the adoption of this statement is not

expected to have a material impact on our financial position or results

of operations.

In December 2007, the FASB issued SFAS No. 160, Noncontrolling Interests

in Consolidated Financial Statements – an amendment of ARB No. 51, (SFAS

No. 160). SFAS No. 160 establishes accounting and reporting standards

for the noncontrolling interest in a subsidiary and for the retained interest

and gain or loss when a subsidiary is deconsolidated. This statement is

effective for financial statements issued for fiscal years beginning on or

after December 15, 2008. Upon the initial adoption of this statement we

will change the classification and presentation of Noncontrolling Interest

in our financial statements, which we currently refer to as minority

interest. We are still evaluating the impact SFAS No. 160 will have, but

we do not expect a material impact on our financial position or results

of operations.

In February 2007, the FASB issued SFAS No. 159, The Fair Value Option for

Financial Assets and Financial Liabilities – Including an Amendment of SFAS

115 (SFAS No. 159), which permits but does not require us to measure

financial instruments and certain other items at fair value. Unrealized gains

and losses on items for which the fair value option has been elected are

reported in earnings. This statement is effective for financial statements

issued for fiscal years beginning after November 15, 2007. As we will not

elect to fair value any of our financial instruments under the provisions of

SFAS No.159, the adoption of this statement effective January 1, 2008 will

not have any impact on our financial statements.

In September 2006, the FASB issued SFAS No. 157, Fair Value Measurements

(SFAS No. 157). SFAS No. 157 defines fair value, establishes a framework

for measuring fair value in generally accepted accounting principles and

establishes a hierarchy that categorizes and prioritizes the sources to be

used to estimate fair value. SFAS No. 157 also expands financial state-

ment disclosures about fair value measurements. On February 12, 2008,

the FASB issued FASB Staff Position (FSP) 157-2 which delays the effective

date of SFAS No. 157 for one year, for all nonfinancial assets and non-

financial liabilities, except those that are recognized or disclosed at fair

value in the financial statements on a recurring basis (at least annually).

SFAS No. 157 and FSP 157-2 are effective for financial statements issued

for fiscal years beginning after November 15, 2007. We will elect a partial

deferral of SFAS No. 157 under the provisions of FSP 157-2 related to the

measurement of fair value used when evaluating goodwill, other intan-

gible assets, wireless licenses and other long-lived assets for impairment

and valuing asset retirement obligations and liabilities for exit or disposal

activities. The impact of partially adopting SFAS No. 157 effective January

1, 2008 will not be material to our financial statements.

In June 2006, the Emerging Issues Task Force (EITF) reached a consensus

on EITF No. 06-3, How Taxes Collected from Customers and Remitted to

Governmental Authorities Should Be Presented in the Income Statement (EITF

No. 06-3). EITF No. 06-3 permits that such taxes may be presented on

either a gross basis or a net basis as long as that presentation is used

consistently. The adoption of EITF No. 06-3 on January 1, 2007 did not

impact our financial statements. We present the taxes within the scope

of EITF No. 06-3 on a net basis.