Verizon Wireless 2007 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2007 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Notes to Consolidated Financial Statements continued

52

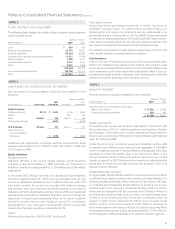

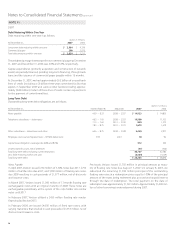

The following table summarizes the allocation of the cost of the merger

to the assets acquired, including cash of $2,361 million, and liabilities

assumed as of the close of the merger.

(dollars in millions)

Assets acquired

Current assets $ 6,001

Property, plant & equipment 6,453

Intangible assets subject to amortization

Customer relationships 1,162

Rights of way and other 176

Deferred income taxes and other assets 1,995

Goodwill 5,085

Total assets acquired $ 20,872

Liabilities assumed

Current liabilities $ 6,093

Long-term debt 6,169

Deferred income taxes and other non-current liabilities 1,720

Total liabilities assumed 13,982

Purchase price $ 6,890

The goodwill resulting from the merger with MCI is included in our

Wireline segment, which includes the operations of the former MCI. The

customer relationships are being amortized on a straight-line basis over

3-8 years based on whether the relationship is with a consumer or a busi-

ness customer since this correlates to the pattern in which the economic

benefits are expected to be realized.

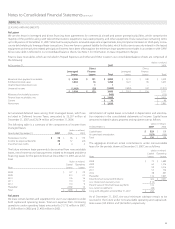

We recorded certain severance and severance-related costs and contract

termination costs in connection with the merger, pursuant to EITF Issue

No. 95-3, Recognition of Liabilities in Connection with a Purchase Business

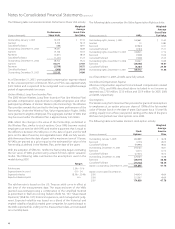

Combination. The following table summarizes the activity related to these

obligations during 2007:

(dollars in millions)

At December 31,

2006 Payments

At December 31,

2007

Severance costs and contract

termination costs $ 376 $ (340) $ 36

The remaining contract termination costs at December 31, 2007 are

expected to be paid over the remaining contract periods through 2008.

In 2007 and 2006, we recorded pretax charges of $178 million ($112

million after-tax) and $232 million ($146 million after-tax), respectively,

primarily associated with the MCI acquisition that were comprised of

advertising and other costs related to re-branding initiatives, facility exit

costs and systems integration activities.

NOTE 8

MERGER AND ACQUISITIONS

Completion of Merger with MCI

On January 6, 2006, after receiving the required state, federal and inter-

national regulatory approvals, Verizon completed the acquisition of 100%

of the outstanding common stock of MCI, Inc. (MCI) for a combination

of Verizon common shares and cash. MCI was a global communications

company that provided Internet, data and voice communication services

to businesses and government entities throughout the world and con-

sumers in the United States.

The merger was accounted for using the purchase method in accordance

with SFAS No. 141, and the aggregate transaction value was $6,890 mil-

lion, consisting of $5,829 million of cash and common stock issued at

closing, $973 million of consideration for the shares acquired from entities

controlled by Carlos Slim Helú, net of the portion of the special dividend

paid by MCI that was treated as a return of our investment, and closing

and other direct merger-related costs. The number of shares issued was

based on the “Average Parent Stock Price,” as defined in the merger agree-

ment. The consolidated financial statements include the results of MCI’s

operations from the date of the close of the merger.

Allocation of the cost of the merger

In accordance with SFAS No. 141, the cost of the merger was allocated

to the assets acquired and liabilities assumed based on their fair values

as of the close of the merger, with the amounts exceeding the fair value

being recorded as goodwill. The process to identify and record the fair

value of assets acquired and liabilities assumed included an analysis of

the acquired fixed assets, including real and personal property; various

contracts, including leases, contractual commitments, and other busi-

ness contracts; customer relationships; investments; and contingencies.

The fair values of the assets acquired and liabilities assumed were deter-

mined using one or more of three valuation approaches: market, income

and cost. The selection of a particular method for a given asset depended

on the reliability of available data and the nature of the asset, among

other considerations. The market approach, which indicates value for a

subject asset based on available market pricing for comparable assets,

was utilized for certain acquired real property and investments. The

income approach, which indicates value for a subject asset based on the

present value of cash flow projected to be generated by the asset, was

used for certain intangible assets such as customer relationships, as well

as for favorable/unfavorable contracts. Projected cash flow is discounted

at a required rate of return that reflects the relative risk of achieving the

cash flow and the time value of money. Projected cash flows for each

asset considered multiple factors, including current revenue from existing

customers; distinct analysis of expected price, volume, and attrition

trends; reasonable contract renewal assumptions from the perspective of

a marketplace participant; expected profit margins giving consideration

to marketplace synergies; and required returns to contributory assets. The

cost approach, which estimates value by determining the current cost of

replacing an asset with another of equivalent economic utility, was used

for the majority of personal property. The cost to replace a given asset

reflects the estimated reproduction or replacement cost for the property,

less an allowance for loss in value due to depreciation or obsolescence,

with specific consideration given to economic obsolescence if indicated.