Verizon Wireless 2007 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2007 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

|

|

58

Notes to Consolidated Financial Statements continued

NOTE 12

FINANCIAL INSTRUMENTS

Derivatives

The ongoing effect of SFAS No. 133 and related amendments and inter-

pretations on our consolidated financial statements will be determined

each period by several factors, including the specific hedging instru-

ments in place and their relationships to hedged items, as well as market

conditions at the end of each period.

Interest Rate Risk Management

We have entered into domestic interest rate swaps to achieve a targeted

mix of fixed and variable rate debt, where we principally receive fixed

rates and pay variable rates based on LIBOR. These swaps hedge against

changes in the fair value of our debt portfolio. We record the interest rate

swaps at fair value in our balance sheet as assets and liabilities and adjust

debt for the change in its fair value due to changes in interest rates.

We also enter into interest rate derivatives to limit our exposure to interest

rate changes. In accordance with the provisions of SFAS No. 133, changes

in fair value of these cash flow hedges due to interest rate fluctuations

are recognized in Accumulated Other Comprehensive Loss. Amounts

recorded to Other Comprehensive Income related to these interest rate

cash flow hedges for the years ended December 31, 2007, 2006 and 2005

were not material.

Net Investment Hedges

During 2007, we entered into foreign currency forward contracts to hedge

a portion of our net investment in Vodafone Omnitel. Changes in fair

value of these contracts due to Euro exchange rate fluctuations are rec-

ognized in Accumulated Other Comprehensive Loss and partially offset

the impact of foreign currency changes on the value of our net invest-

ment. As of December 31, 2007, Accumulated Other Comprehensive Loss

includes unrecognized losses of approximately $57 million ($37 million

after-tax) related to these hedge contracts, which along with the unre-

alized foreign currency translation balance on the investment hedged,

remain in Accumulated Other Comprehensive Loss until the investment

is sold.

During 2005, we entered into zero cost Euro collars to hedge a portion

of our net investment in Vodafone Omnitel. During 2005, our positions

in the zero cost euro collars were settled. As of December 31, 2007 and

2006, Accumulated Other Comprehensive Loss includes unrecognized

gains of $2 million in each year related to these hedge contracts, which

along with the unrealized foreign currency translation balance of the

investment hedged, remain in Accumulated Other Comprehensive Loss

until the investment is sold.

Other Derivatives

On May 17, 2005, we purchased 43.4 million shares of MCI common stock

under a stock purchase agreement that contained a provision for the

payment of an additional cash amount determined immediately prior to

April 9, 2006 based on the market price of Verizon’s common stock. Under

SFAS No. 133, this additional cash payment was an embedded derivative

which we carried at fair value and was subject to changes in the market

price of Verizon stock. Since this derivative did not qualify for hedge

accounting under SFAS No. 133, changes in its fair value were recorded in

the consolidated statements of income in Other Income and (Expense),

Net. As of December 31, 2006, this embedded derivative expired with

no requirement for an additional cash payment to be made under the

stock purchase agreement. During 2006 and 2005, we recorded pretax

income of $4 million and $57 million, respectively, in connection with this

embedded derivative.

Concentrations of Credit Risk

Financial instruments that subject us to concentrations of credit risk con-

sist primarily of temporary cash investments, short-term and long-term

investments, trade receivables, certain notes receivable, including lease

receivables, and derivative contracts. Our policy is to deposit our tem-

porary cash investments with major financial institutions. Counterparties

to our derivative contracts are also major financial institutions. The finan-

cial institutions have all been accorded high ratings by primary rating

agencies. We limit the dollar amount of contracts entered into with any

one financial institution and monitor our counterparties’ credit ratings.

We generally do not give or receive collateral on swap agreements due

to our credit rating and those of our counterparties. While we may be

exposed to credit losses due to the nonperformance of our counterpar-

ties, we consider the risk remote and do not expect the settlement of

these transactions to have a material effect on our results of operations

or financial condition.

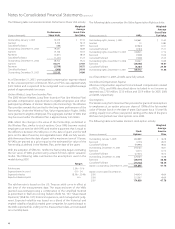

Fair Values of Financial Instruments

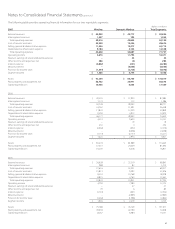

The tables that follow provide additional information about our signifi-

cant financial instruments:

Financial Instrument Valuation Method

Cash and cash equivalents and

short-term investments

Carrying amounts

Short- and long-term debt

(excluding capital leases)

Market quotes for similar terms

and maturities or future cash ows

discounted at current rates

Cost investments in unconsolidated

businesses, derivative assets

and liabilities and notes receivable

Future cash ows discounted at

current rates, market quotes

for similar instruments or other

valuation models

(dollars in millions)

At December 31, 2007 2006

Carrying

Amount Fair Value

Carrying

Amount Fair Value

Short- and long-term debt $ 30,845 $ 32,380 $ 36,000 $ 37,165

Cost investments in

unconsolidated businesses 315 315 270 270

Short- and long-term

derivative assets 61 61 31 31

Short- and long-term

derivative liabilities 57 57 10 10