Walmart 2011 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2011 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

|

|

Management’s Discussion and Analysis of Financial

Condition and Results of Operations

Walmart 2011 Annual Report 21

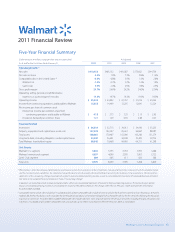

Consolidated Results of Operations

Fiscal Years Ended January 31,

2011 2010 2009

Net sales

(1)

$418,952 $405,132 $401,087

Percentage change from

comparable period 3.4% 1.0% 7.3%

Total U.S. calendar comparable

store and club sales -0.6% -0.8% 3.5%

Gross prot margin as

a percentage of sales 24.7% 24.9% 24.2%

Operating income

(1)

$ 25,542 $ 24,002 $ 22,767

Operating income as a

percentage of net sales 6.1% 5.9% 5.7%

Income from continuing

operations

(1)

$ 15,959 $ 14,962 $ 13,734

Unit counts 8,970 8,459 7,909

Retail square feet

(2)

984,949 952,237 918,044

(1)

Dollar amounts in millions

(2)

Amounts in thousands

Our consolidated net sales increased by 3.4% and 1.0% in scal 2011 and

2010, respectively. Net sales in scal 2011 primarily increased due to our

continued expansion activities as we added 3.4% of additional retail

square feet during the year. In addition, $4.5 billion of the increase in net

sales during scal 2011 resulted from currency exchange rate uctuations,

oset by a 0.6% decline in U.S. comparable store and club sales. Net sales

in scal 2010 increased due to the growth in customer trac, continued

global expansion activities and the acquisition of D&S in January 2009,

oset primarily by a $9.8 billion unfavorable currency exchange rate

impact in our Walmart International segment and price deation in

certain merchandise categories in our Walmart U.S. segment. Volatility

in currency exchange rates may continue to impact the Company’s net

sales in the future.

Our gross prot, as a percentage of net sales (our “gross prot margin”),

was 24.7%, 24.9% and 24.2% in scal 2011, 2010 and 2009, respectively. Our

Walmart U.S. segment and Walmart International segment net sales yield

higher gross prot margins than our Sam’s Club segment, which operates

on lower margins as a membership club warehouse. In scal 2011, gross

prot margin was relatively at compared to scal 2010. In scal 2010, gross

prot margin increased primarily due to enhanced merchandising strategies

in our Walmart U.S. and Sam’s Club segments.

Operating expenses, as a percentage of net sales, were 19.3%, 19.7% and

19.3% for scal 2011, 2010 and 2009, respectively. In scal 2011, operating

expenses as a percentage of net sales decreased primarily due to improved

labor productivity and organizational changes implemented at the end of

scal 2010 designed to strengthen and streamline our operations, as well

as a reduction in certain incentive plan expenses. In scal 2010, operating

expenses increased primarily due to higher health benet costs, a pre-tax

charge of $260 million relating to the restructuring of U.S. operations, and

higher advertising expenses.

Operating income was $25.5 billion, $24.0 billion and $22.8 billion for scal

2011, 2010 and 2009, respectively. Operating income in scal 2011 was aided

by $231 million due to the eects of currency exchange uctuations.

Operating income in scal 2010 was reduced by $540 million due to the

eect of currency exchange rate uctuations. Volatility in currency

exchange rates may continue to impact the Company’s operating income in

the future.

Our eective income tax rate was 32.2%, 32.4% and 34.2% for scal 2011,

2010 and 2009, respectively. The scal 2011 and scal 2010 provision for

taxes include certain tax benets that caused the eective tax rates for

each of those two years to be less than the eective tax rate in scal 2009.

During scal 2011 and 2010, we recorded certain tax benets totaling

$434 million and $372 million, respectively, primarily from the repatriation

of certain non-U.S. earnings that increased our U.S. foreign tax credits.

We expect the scal 2012 annual eective tax rate to be approximately

33.5% to 34.5%. Signicant factors that may impact the annual eective

tax rate include changes in our assessment of certain tax contingencies,

settlement of tax contingencies and the mix of earnings among our

U.S. and international operations.

As a result of the factors discussed above, we reported $16.0 billion,

$15.0 billion and $13.7 billion of income from continuing operations for

the scal years ended January 31, 2011, 2010 and 2009, respectively.

Walmart U.S. Segment

Fiscal Years Ended January 31,

2011 2010 2009

Net sales

(1)

$260,261 $259,919 $256,970

Percentage change from

comparable period 0.1% 1.1% 7.6%

Calendar comparable store sales -1.5% -0.7% 3.2%

Operating income

(1)

$ 19,914 $ 19,313 $ 18,310

Operating income as

a percentage of net sales 7.7% 7.4% 7.1%

Unit counts 3,804 3,755 3,703

Retail square feet

(2)

617,067 605,852 592,256

(1)

Dollar amounts in millions

(2)

Amounts in thousands

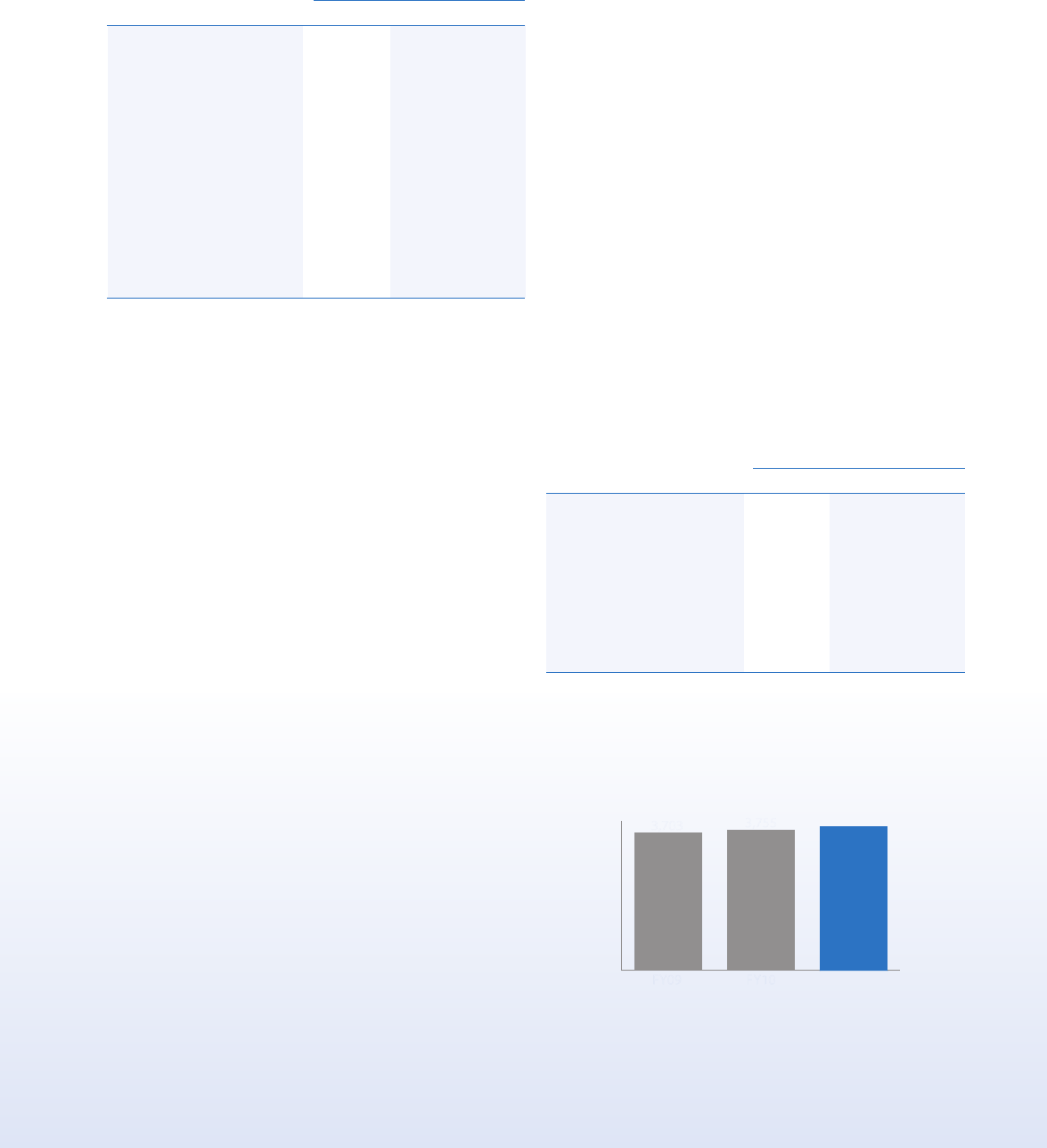

Walmart U.S.

unit counts

3,804

3,755

3,703

FY09 FY10 FY11