America Online 2011 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2011 America Online annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

Table of Contents

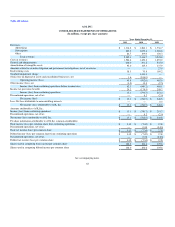

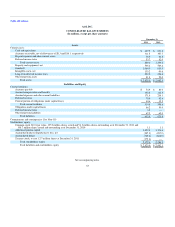

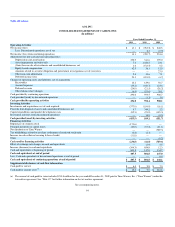

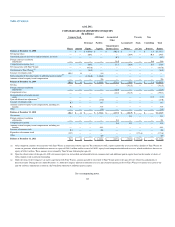

AOL INC.

PART II—ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

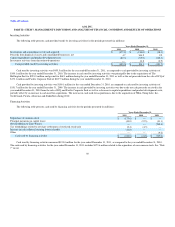

any operating unit below the consolidated unit level. Based on the facts above, we also concluded for purposes of our impairment analysis that AOL consists

of a single reporting unit. This conclusion is also based on the shared infrastructure and interdependency of our revenue streams. Different judgments relating

to the determination of reporting units could significantly affect the testing of goodwill for impairment and the amount of any impairment recognized.

Goodwill impairment is determined using a two-step process. The first step involves a comparison of the estimated fair value of our reporting unit to its

carrying amount, including goodwill. If the estimated fair value of our reporting unit exceeds its carrying amount, goodwill of the reporting unit is not

impaired and the second step of the impairment test is not necessary. If the carrying amount of our reporting unit exceeds its estimated fair value, then the

second step of the goodwill impairment test must be performed. To measure the amount of impairment loss, if any, we determine the implied fair value of

goodwill in the same manner as the amount of goodwill recognized in a business combination. Specifically, the estimated fair value of the reporting unit is

allocated to all of the assets and liabilities of that unit (including any unrecognized intangible assets) as if the reporting unit had been acquired in a business

combination and the fair value of the reporting unit was the price paid to acquire the reporting unit. If the carrying amount of the reporting unit's goodwill

exceeds the implied fair value of that goodwill, an impairment loss is recognized in an amount equal to that excess.

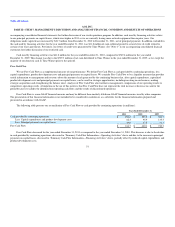

We experienced a significant decline in our stock price leading up to and subsequent to the announcement on August 9, 2011 of our financial results for

the three months ended June 30, 2011. We determined that the magnitude of this stock price decline along with the weakness in the overall equity markets

constituted a substantive change in circumstances in August that could potentially reduce the fair value of our single reporting unit below its carrying amount.

Accordingly, we tested goodwill for impairment as of August 31, 2011 (the "interim testing date"). We also performed our annual impairment test as of

December 1, 2011.

In performing each of these impairment tests, the estimated fair value of our reporting unit was determined utilizing a market-based approach, with the

quoted market price of our stock in an active market as the primary input. To determine the estimated fair value of our reporting unit as of August 31, 2011,

we calculated our market capitalization based on our stock price and adjusted it by a control premium of 50%, which resulted in an estimated fair value of

$2,455.8 million. From August 31, 2011 to the date of our annual goodwill impairment test, while the Company's stock price declined, our actual operating

income slightly exceeded our projections and our long-term projections did not materially change during that period. Given these trends, we determined as of

December 1, 2011 that it was appropriate to adjust our market capitalization with a control premium of 70%, which resulted in an estimated fair value for our

reporting unit of $2,318.1 million as of December 1, 2011. The premium used to arrive at a controlling interest equity value in each of these cases was

determined based in part on values observed in recent market transactions, and based in part on the value of other assets that a marketplace participant could

benefit from in acquiring a controlling interest in our reporting unit.

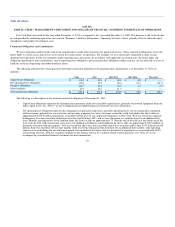

Determining the fair value of our reporting unit requires the exercise of significant judgment, primarily related to the premium used to arrive at a

controlling interest equity value used in the market-based approach. The control premium is determined based in part on recent market transactions and also

takes into account recent trends in market capitalization as of the date of the impairment test, and therefore the control premium determined herein does not

necessarily correlate to a control premium determined in the past or future goodwill impairment analyses. Significant changes in the estimates and

assumptions used in deriving our control premium could materially affect the determination of fair value for our reporting unit, which could impact the

magnitude of an impairment loss (if any) recognized or trigger future impairment. Due to the significant judgments used in deriving the control premium, the

fair value of our single reporting unit determined in connection with the goodwill impairment test may not necessarily be indicative of the actual value that

would be recognized in any future transaction.

56