Charter 2002 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2002 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

|

|

CHARTER COMMUNICATIONS, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

December 31, 2002, 2001 and 2000

(dollars in millions, except where indicated)

In June 2002, the Financial Accounting Standards Board issued SFAS No. 146, ""Accounting for Costs

Associated with Exit or Disposal Activities.'' SFAS No. 146 addresses Ñnancial accounting and reporting for

costs associated with exit or disposal activities and nulliÑes Emerging Issues Task Force Issue No. 94-3,

""Liability Recognition for Certain Employee Termination BeneÑts and Other Costs to Exit an Activity

(including Certain Costs Incurred in a Restructuring).'' SFAS 146 requires that a liability for costs associated

with an exit or disposal activity be recognized when the liability is incurred rather than when a company

commits to such an activity and also establishes fair value as the objective for initial measurement of the

liability. SFAS No. 146 will be adopted by the Company for exit or disposal activities that are initiated after

December 31, 2002. Adoption will not have a material impact on the consolidated Ñnancial statements of the

Company.

In December 2002, the Financial Accounting Standards Board (FASB) issued SFAS No. 148,

""Accounting for Stock-Based Compensation Ì Transition and Disclosure.'' SFAS No. 148 amends SFAS

No. 123 to provide alternative methods of transition for a voluntary change to the fair value based method of

accounting for stock-based employee compensation. In addition, it amends the disclosure requirements of

SFAS No. 123 to require prominent disclosures in both annual and interim Ñnancial statements about the

method of accounting for stock-based compensation and the eÅect of the method used on reported results.

The Company adopted SFAS No. 148 beginning January 1, 2003. On January 1, 2003, the Company also

adopted SFAS No. 123, ""Accounting for Stock-Based Compensation'' on the prospective method under

which the Company will recognize compensation expense of a stock-based award to an employee over the

vesting period based on the fair value of the award on the grant date.

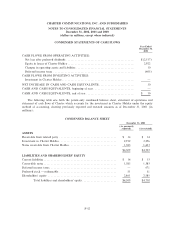

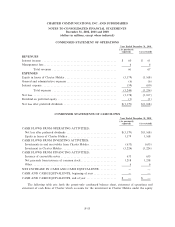

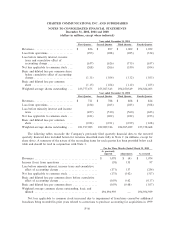

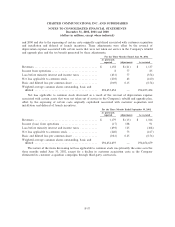

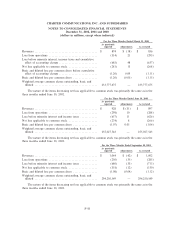

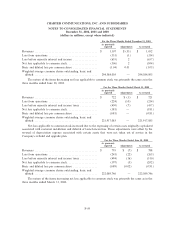

27. Parent Company Only Financial Statements

As the result of limitations on, and prohibitions of, distributions, substantially all of the net assets of the

consolidated subsidiaries are restricted for distribution to Charter, the parent company. The following

condensed parent-only Ñnancial statements of Charter account for the investment in Charter Holdco under

the equity method of accounting. The Ñnancial statements should be read in conjunction with the consolidated

Ñnancial statements of the Company and notes thereto. The information in this footnote has been revised from

the information previously reported to reÖect the Company's restatement of its consolidated Ñnancial

statements of the years ended December 31, 2001 and 2000. See Note 3 for a description of the restatement.

F-50