Charter 2002 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2002 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

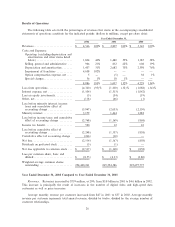

restatement with eÅect from January 1, 2000 to properly exclude those assets from the population of assets

treated as subject to replacement and thus for which a shortened depreciation life was previously assigned.

The evaluation conducted in connection with the restatement also revealed the inadvertent exclusion of

$401 million of trunk and distribution cabling and electronics, which were acquired in 1999, from the

population of assets that were subject to shortened depreciation lives. This group of assets were misclassiÑed

within our Ñxed assets sub-ledger for one acquisition and thus omitted from the analysis performed in

connection with the preparation of our historical Ñnancial statements. Accordingly, an adjustment was made

in the restatement to properly include these assets as well.

Furthermore, an adjustment to reduce the value of assets subject to replacement of approximately

$1.2 billion was determined necessary to record the assets at estimated depreciated replacement cost at the

date of acquisition.

As a result of the items identiÑed above, we determined that depreciation expense was overstated by

$413 million for the Ñrst three quarters of 2002, and $330 million and $119 million in the years ended 2001

and 2000, respectively.

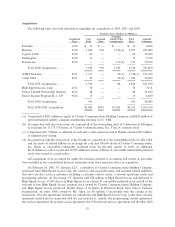

Deferred Tax Liabilities/Franchise Assets. Adjustments were made to record deferred tax liabilities

associated with the acquisition of various cable television businesses. These adjustments increased amounts

assigned to franchise assets by $1.4 billion with a corresponding increase in deferred tax liabilities of

$1.2 billion. The balance of the entry was recorded to equity and minority interest. In addition, as described

above, a correction was made to reduce amounts assigned in purchase accounting to assets identiÑed for

replacement over the three-year period of our rebuild and upgrade of our network. This reduced the amount

assigned to the network assets to be retained and increased the amount assigned to franchise assets by

approximately $627 million with a resulting increase in amortization expense for the years restated. Such

adjustments increased the impairment of franchises recognized in the Ñrst quarter of 2002 by $199 million

(before minority interest) and increased amortization expense by $130 million and $121 million for the years

ended December 31, 2001 and 2000, respectively.

Other Adjustments. In addition to the items described above, reductions to 2000 revenues include the

reversal of certain advertising revenues from equipment vendors. Other adjustments of expenses include

expensing certain marketing and customer acquisition costs previously charged against purchase accounting

reserves, certain tax reclassiÑcations from tax expense to operating costs, reclassifying management fee

revenue from a joint venture to oÅset losses from investments and adjustments to option compensation

expense. The net impact of these adjustments to net loss is an increase of $38 million and a decrease of

$10 million, respectively, for the years ended December 31, 2001 and 2000.

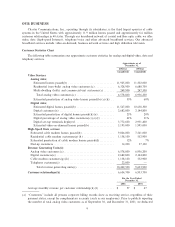

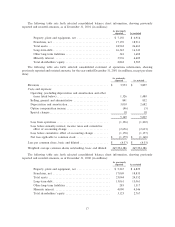

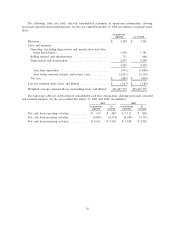

The tables below set forth our condensed consolidated balance sheets as of December 31, 2001 and

December 31, 2000, and condensed consolidated statement of operations and condensed consolidated

statement of cash Öows information for the years ended December 31, 2001 and 2000. For greater detail see

Note 3 to our consolidated Ñnancial statements.

Controls. The adjustments for the rebuild and upgrade of cable systems and deferred tax matters/

franchise generally relate to non-recurring activities. Since our period of rapid growth in 2000 and early 2001,

in which we were rapidly acquiring cable systems, we have integrated the various accounting processes of our

acquired cable systems. For more information, see Note 5 to our consolidated Ñnancial statements. We have

also substantially improved the quantity and, we believe, the quality of our accounting and internal audit staÅ.

In addition, we are developing better interactions between our accounting and internal audit staÅ and the other

elements of our organization. These changes in our staÅ have been supplemented with changes in accounting

and internal controls processes and systems which we believe result in an improved ability of management to

understand and analyze underlying business data. The role of our internal audit staÅ has also been expanded,

particularly with respect to capitalization and depreciation. We believe that these changes in staÅ, responsibili-

ties and processes and systems have improved both our controls over recurring transactions and non-recurring

transactions, such as integration of acquired cable systems and the rebuild and upgrade of cable systems.

16