Charter 2002 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2002 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

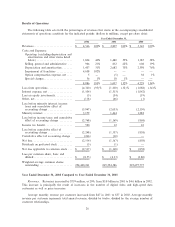

assets), respectively. Furthermore, we recorded approximately $54 million of goodwill as a result of the

acquisition of High Speed Access in February 2002.

We adopted SFAS No. 142 ""Goodwill and Other Intangible Assets'' on January 1, 2002. SFAS No. 142

requires that franchise intangible assets that meet the indeÑnite life criteria no longer be amortized against

earnings but instead must be tested for impairment annually or more frequently as warranted by events or

changes in circumstances. In determining whether our franchises have an indeÑnite life, we considered the

exclusivity of the franchise, the expected costs of franchise renewals, and the technological state of the

associated cable systems with a view to whether or not we are in compliance with any technology upgrading

requirements. We have concluded that as of January 1, 2002 and December 31, 2002 more than 99% of our

franchises qualify for indeÑnite life treatment under SFAS No. 142, and that less than one percent of our

franchises do not qualify for indeÑnite-life treatment due to technological or operational factors that limit their

lives. Costs of Ñnite-lived franchises, along with costs associated with franchise renewals, will be amortized on

a straight-line basis over 10 years, which represents management's best estimate of the average remaining

useful lives of such franchises. Prior to the adoption of SFAS No. 142, our franchises were amortized over an

average useful life of 15 years. Franchise amortization expense related to franchises not qualifying for

indeÑnite life treatment totaled $9 million for the year ended December 31, 2002. Franchise amortization

expense was $1.4 billion and $1.4 billion, representing approximately 28% and 33% of costs and expenses, for

the years ended December 31, 2001 and 2000. Going forward, we expect amortization expense on franchise

assets will be approximately $8 million annually based on our current franchise agreements and anticipated

upgrade plans. Our goodwill is also deemed to have an indeÑnite life under SFAS No. 142.

SFAS No. 144, ""Accounting for Impairment or Disposal of Long-Lived Assets,'' requires that we

evaluate the recoverability of our property, plant and equipment and franchise assets which did not qualify for

indeÑnite life treatment under SFAS No. 142 upon the occurrence of events or changes in circumstances

which indicate that the carrying amount of an asset may not be recoverable. Such events or changes in

circumstances could include such factors as changes in technological advances, Öuctuations in the fair value of

such assets, adverse changes in relationships with local franchise authorities, adverse changes in market

conditions or poor operating results. Under SFAS No. 144, a long-lived asset is deemed impaired when the

carrying amount of the asset exceeds the projected undiscounted future cash Öows associated with the asset.

Furthermore, we were required to evaluate the recoverability of our indeÑnite life franchises, as well as

goodwill, as of January 1, 2002 upon adoption of SFAS No. 142, and on an annual basis or more frequently as

deemed necessary.

Under both SFAS No. 144 and SFAS No. 142, if an asset is determined to be impaired, it is required to

be written down to its estimated fair market value. We determine fair market value based on estimated

discounted future cash Öows, using reasonable and appropriate assumptions that are consistent with internal

forecasts. Our assumptions include these and other factors: penetration rates for analog and digital video and

high-speed data, revenue growth rates, expected operating margins and capital expenditures. Considerable

management judgment is necessary to estimate future cash Öows, and such estimates include inherent

uncertainties, including those relating to the timing and amount of future cash Öows and the discount rate used

in the calculation. We utilize an independent third-party appraiser with expertise in the cable industry to assist

in the determination of the fair value of intangible assets.

During the Ñrst quarter of 2002, we had an independent appraiser perform valuations of our franchises as

of January 1, 2002. Based on the guidance prescribed in Emerging Issues Task Force (EITF) Issue No. 02-7,

Unit of Accounting for Testing of Impairment of IndeÑnite-Lived Intangible Assets, franchises were aggregated

into essentially inseparable asset groups to conduct the valuations. The asset groups generally represent

geographic clusters of our cable systems which management believes represents the highest and best use of

those assets. We determined that our franchises were impaired and as a result recorded the cumulative eÅect

of a change in accounting principle of $266 million, net of minority interest. This adjustment has been

reÖected in the year ended December 31, 2002 Ñnancial statements. As required by SFAS No. 142, the

standard has not been retroactively applied to results for the period prior to adoption.

23