Charter 2002 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2002 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

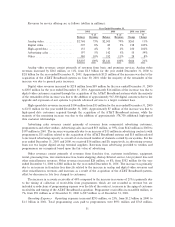

We performed our annual impairment assessment as of October 1, 2002 using an independent third-party

appraiser and following the guidance of EITF Issue 02-17, Recognition of Customer Relationship Intangible

Assets Acquired in a Business Combination, which was issued in October 2002 and requires the consideration

of assumptions that marketplace participants would consider, such as expectations of future contract renewals

and other beneÑts related to the intangible asset. Revised earnings forecasts and the methodology required by

SFAS No. 142, which excludes certain intangibles, led to recognition of a $4.6 billion impairment charge in

the fourth quarter of 2002.

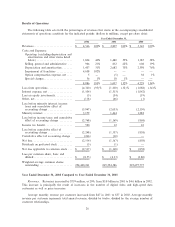

The independent third party appraiser's valuation as of October 1, 2002, yielded an enterprise value of

approximately $25 billion, which included $3 billion assigned to customer relationships. SFAS No. 142 does

not permit the recognition of the customer relationship asset not previously recognized. Accordingly, our

impairment analysis could not include approximately $373 million and $2.9 billion attributable to customer

relationship values as of January 1, 2002 and October 1, 2002, respectively.

This valuation involves numerous assumptions as noted above. While the current economic conditions

indicate the combination of assumptions utilized in the appraisal is reasonable, as market conditions change so

will the assumptions with a resulting impact on the valuation. A 10% increase in fair value of the enterprise

would have decreased the impairment charge by approximately $1.6 billion while a 10% decrease in the fair

value of the enterprise would have increased the impairment charge by approximately $2.0 billion.

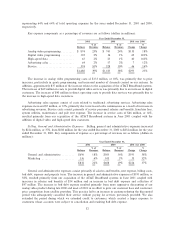

Income Taxes. All operations are held through Charter Communications Holding Company, LLC and

its direct and indirect subsidiaries. Charter Communications Holding Company and the majority of its

subsidiaries are not subject to income tax. However, certain of these subsidiaries are corporations and are

subject to income tax. All of the taxable income, gains, losses, deductions and credits of Charter Communica-

tions Holding Company are passed through to its members: Charter Communications, Inc., Charter

Investment, Inc., Vulcan Cable III, Inc., and certain former owners of acquired companies. Charter

Communications, Inc. is responsible for its share of taxable income or loss of Charter Communications

Holding Company allocated to it in accordance with the Charter Communications Holding Company

amended and restated limited liability company agreement (""LLC Agreement'') and partnership tax rules

and regulations.

The LLC Agreement provides for certain special allocations of net tax proÑts and net tax losses (such net

tax proÑts and net tax losses being determined under the applicable federal income tax rules for determining

capital accounts). Pursuant to the LLC Agreement, through the end of 2003, net tax losses of Charter

Communications Holding Company that would otherwise have been allocated to Charter Communications,

Inc. based generally on its percentage ownership of outstanding common units will be allocated instead to the

membership units held by Vulcan Cable and Charter Investment (the ""Special Loss Allocations'') to the

extent of their capital account balances. The LLC Agreement further provides that, beginning at the time

Charter Communications Holding Company Ñrst generates net tax proÑts, the net tax proÑts that would

otherwise have been allocated to Charter Communications, Inc. based generally on its percentage ownership

of outstanding common membership units will instead be allocated to Vulcan Cable and Charter Investment

(the ""Special ProÑt Allocations''). The Special ProÑt Allocations to Vulcan Cable and Charter Investment

will generally continue until the cumulative amount of the Special ProÑt Allocations oÅsets the cumulative

amount of the Special Loss Allocations. The LLC Agreement generally provides that any additional net tax

proÑts are to be allocated proportionately among the members of Charter Communications Holding Company

based on their ownership of Charter Communications Holding Company membership units. The cumulative

amount of the actual income tax losses allocated to Vulcan Cable and Charter Investment as a result of the

Special Loss Allocations through the period ended December 31, 2002 is approximately $3.3 billion.

In certain situations, the Special Loss Allocations and Special ProÑt Allocations described above could

result in Charter Communications, Inc. paying taxes in an amount that is more or less than if Charter

Communications Holding Company had allocated net tax proÑts and net tax losses among its members based

generally on the number of common membership units owned by such members. This could occur due to

diÅerences in (i) the character of the allocated income (e.g., ordinary versus capital), (ii) the allocated

amount and timing of tax depreciation and tax amortization expense due to the application of section 704(c)

24