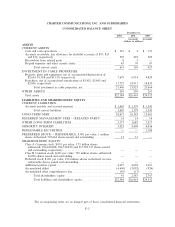

Charter 2002 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2002 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

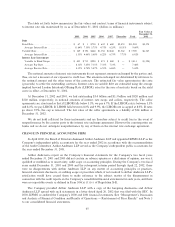

|

|

‚ incur additional debt;

‚ issue equity;

‚ repurchase or redeem equity interests and debt;

‚ grant liens; and

‚ pledge assets.

Furthermore, in accordance with our subsidiaries' credit facilities, a number of our subsidiaries are

required to maintain speciÑed Ñnancial ratios and meet Ñnancial tests. These Ñnancial ratios decrease over

time and will become more diÇcult to maintain during the latter half of 2003 and thereafter. The ability to

comply with these provisions may be aÅected by events beyond our control. The breach of any of these

covenants will result in a default under the applicable debt agreement or instrument and could trigger

acceleration of the debt under the applicable agreement, and in certain cases under other agreements

governing our long-term indebtedness. Any default under our credit facilities or indentures governing our

outstanding debt might adversely aÅect our growth, our Ñnancial condition and our results of operations and

the ability to make payments on the publicly held notes of Charter Communications, Inc. and our subsidiaries

and the credit facilities of our subsidiaries. For more information, see the section above entitled ""Liquidity and

Capital Resources.''

Acceleration of Indebtedness of Our Subsidiaries. In the event of a default under our subsidiaries' credit

facilities or public notes, our subsidiaries' creditors could elect to declare all amounts borrowed, together with

accrued and unpaid interest and other fees, to be due and payable. In such event, our subsidiaries' credit

facilities and indentures will not permit our subsidiaries to distribute funds to Charter Communications

Holding Company or Charter Communications, Inc. to pay interest or principal on our public notes. If the

amounts outstanding under such credit facilities or public notes are accelerated, all of our subsidiaries' debt

and liabilities would be payable from our subsidiaries' assets, prior to any distribution of our subsidiaries' assets

to pay the interest and principal amounts on our public notes. In addition, the lenders under our credit

facilities could foreclose on their collateral, which includes equity interests in our subsidiaries, and exercise

other rights of secured creditors. In any such case, we might not be able to repay or make any payments on our

public notes. Additionally, an acceleration or payment default under our credit facilities would cause a cross-

default in the indentures governing the Charter Holdings notes and our convertible senior notes and would

trigger the cross-default provision of the Charter Operating Credit Agreement. Any default under any of our

subsidiaries' credit facilities or public notes might adversely aÅect the holders of our public notes and our

growth, Ñnancial condition and results of operations and could force us to examine all options, including

seeking the protection of the bankruptcy laws.

Charter Communications, Inc.'s Public Notes are Structurally Subordinated to all Liabilities of our

Subsidiaries. The borrowers and guarantors under the Charter Operating credit facilities, the CC VI

Operating credit facilities, the Falcon credit facilities and the CC VIII Operating credit facilities are our

indirect subsidiaries. A number of our subsidiaries are also obligors under other debt instruments, including

Charter Holdings, which is a co-issuer of senior notes and senior discount notes issued in March 1999, January

2000, January 2001, May 2001 and January 2002. As of December 31, 2002, our total debt was approximately

$18.7 billion, $17.3 billion of which would have been structurally senior to the Charter Communications, Inc.

public notes. In a liquidation, the lenders under all of our subsidiaries' credit facilities and the holders of the

other debt instruments and all other creditors of our subsidiaries will have the right to be paid before us from

any of our subsidiaries' assets.

If we caused a subsidiary to make a distribution to enable us to make payments in respect of our public

notes, and such transfer were deemed a fraudulent transfer or an unlawful distribution, the holders of our

public notes could be required to return the payment to (or for the beneÑt of) the creditors of our subsidiaries.

In the event of the bankruptcy, liquidation or dissolution of a subsidiary, following payment by such subsidiary

of its liabilities, such subsidiary may not have suÇcient assets remaining to make any payments to us as an

equity holder or otherwise and may be restricted by bankruptcy and insolvency laws from making any such

payments. This adversely aÅects our ability to make payments to the holders of our public notes.

59