Charter 2002 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2002 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

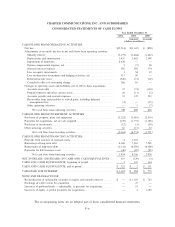

on reported results. SFAS No. 148 was adopted by us beginning January 1, 2003. On January 1, 2003, we also

adopted SFAS 123, ""Accounting for Stock-Based Compensation'' on the prospective method under which we

will recognize compensation expense of a stock-based award to an employee over the vesting period based on

the fair value of the award on the grant date.

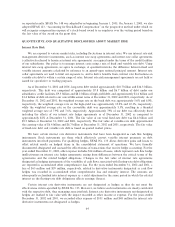

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Interest Rate Risk

We are exposed to various market risks, including Öuctuations in interest rates. We use interest rate risk

management derivative instruments, such as interest rate swap agreements and interest rate collar agreements

(collectively referred to herein as interest rate agreements) as required under the terms of the credit facilities

of our subsidiaries. Our policy is to manage interest costs using a mix of Ñxed and variable rate debt. Using

interest rate swap agreements, we agree to exchange, at speciÑed intervals, the diÅerence between Ñxed and

variable interest amounts calculated by reference to an agreed-upon notional principal amount. Interest rate

collar agreements are used to limit our exposure to, and to derive beneÑts from, interest rate Öuctuations on

variable rate debt to within a certain range of rates. Interest rate risk management agreements are not held or

issued for speculative or trading purposes.

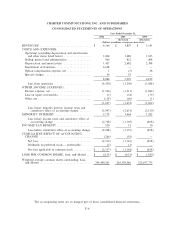

As of December 31, 2002 and 2001, long-term debt totaled approximately $18.7 billion and $16.3 billion,

respectively. This debt was comprised of approximately $7.8 billion and $6.7 billion of debt under our

subsidiaries' credit facilities, $9.5 billion and $8.2 billion of high-yield debt and approximately $1.4 billion and

$1.4 billion of debt related to our convertible senior notes at December 31, 2002 and 2001, respectively. As of

December 31, 2002 and 2001, the weighted average rate on the bank debt was approximately 5.6% and 6.0%,

respectively, the weighted average rate on the high-yield was approximately 10.2% and 10.1%, respectively,

while the weighted average rate on the convertible debt was approximately 5.3%, resulting in a blended

weighted average rate of 7.9% and 7.6%, respectively. Approximately 79% of our debt was eÅectively Ñxed

including the eÅects of our interest rate hedge agreements as of December 31, 2002 as compared to

approximately 82% at December 31, 2001. The fair value of our total Ñxed-rate debt was $4.4 billion and

$9.5 billion at December 31, 2002 and 2001, respectively. The fair value of variable-rate debt approximated

the carrying value of $6.4 billion and $6.7 billion at December 31, 2002 and 2001, respectively. The fair value

of Ñxed-rate debt and variable rate debt is based on quoted market prices.

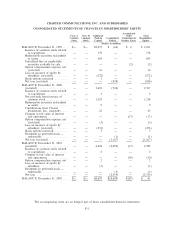

We have certain interest rate derivative instruments that have been designated as cash Öow hedging

instruments. Such instruments are those which eÅectively convert variable interest payments on debt

instruments into Ñxed payments. For qualifying hedges, SFAS No. 133 allows derivative gains and losses to

oÅset related results on hedged items in the consolidated statement of operations. We have formally

documented, designated and assessed the eÅectiveness of transactions that receive hedge accounting. For the

year ended December 31, 2002, other expense includes $14 million of losses, which represent cash Öow hedge

ineÅectiveness on interest rate hedge agreements arising from diÅerences between the critical terms of the

agreements and the related hedged obligations. Changes in the fair value of interest rate agreements

designated as hedging instruments of the variability of cash Öows associated with Öoating-rate debt obligations

are reported in accumulated other comprehensive loss. For the years ended December 31, 2002 and 2001, a

loss of $65 million and $39 million, respectively, related to derivative instruments designated as cash Öow

hedges was recorded in accumulated other comprehensive loss and minority interest. The amounts are

subsequently reclassiÑed into interest expense as a yield adjustment in the same period in which the related

interest on the Öoating-rate debt obligations aÅects earnings (losses).

Certain interest rate derivative instruments are not designated as hedges as they do not meet the

eÅectiveness criteria speciÑed by SFAS No. 133. However, we believe such instruments are closely correlated

with the respective debt, thus managing associated risk. Interest rate derivative instruments not designated as

hedges are marked to fair value with the impact recorded as other income or expense. For the years ended

December 31, 2002 and 2001, we recorded other expense of $101 million and $48 million for interest rate

derivative instruments not designated as hedges.

64