Charter 2011 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2011 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

|

|

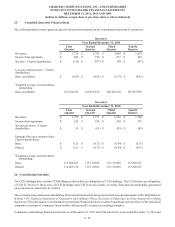

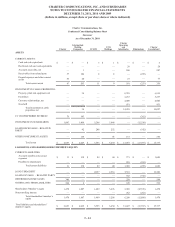

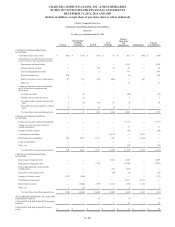

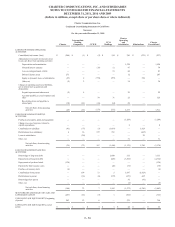

CHARTER COMMUNICATIONS, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2011, 2010 AND 2009

(dollars in millions, except share or per share data or where indicated)

F- 40

Fresh start accounting provided, among other things, for a determination of the value assigned to the equity of the emerging

company as of a date selected for financial reporting purposes. In the Disclosure Statement, the reorganization value of the Company

was set forth as approximately $14.1 billion to $16.6 billion, with a midpoint estimate of $15.4 billion. Under fresh start accounting,

this reorganization value was allocated to the Company’s assets based on their respective fair values. The fresh start adjustments

to fair value resulted in an increase to the carrying value of property, plant and equipment of $2.0 billion, the establishment of

customer relationships at a fair value of $2.4 billion, and the recording of goodwill of $951 million. The reduction in long-term

debt was $502 million to reflect it at its fair value and the net increase to shareholder’s equity was $6.0 billion.

Reorganization value, along with other terms of the Plan, was determined after extensive arms-length negotiations with the

Company’s creditors. The value was based upon expected future cash flows of the business after emergence from Chapter 11,

discounted at rates reflecting perceived business and financial risks (the discounted cash flows). This valuation and a valuation

using market value multiples for peer companies were blended to arrive at the reorganization value. Reorganization value is

intended to approximate the amount a willing buyer would pay for the assets of the Company immediately after the reorganization.

Based on conditions in the cable industry and general economic conditions, the mid-point of the range of valuations was used to

determine the reorganization value. Under fresh start accounting, this reorganization value was allocated to the Company’s assets

based on their respective fair values. The reorganization value, after adjustments for working capital, is reduced by the fair value

of debt and other noncurrent liabilities, and preferred stock with the remainder representing the value to common shareholders.

The market capitalization of Charter’s common stock may differ materially from this value.

The significant assumptions related to the valuations of the Company’s assets and liabilities in connection with fresh start accounting

include the following:

Property, plant and equipment — Property, plant and equipment was valued at fair value of $6.8 billion as of November 30, 2009.

In establishing fair value for the vast majority of the Company’s property, plant and equipment, the cost approach was utilized.

The cost approach considers the amount required to replace an asset by constructing or purchasing a new asset with similar utility,

then adjusts the value in consideration of all forms of depreciation as of the appraisal date.

The cost approach relies on management’s assumptions regarding current material and labor costs required to rebuild and repurchase

significant components of the Company’s property, plant and equipment along with assumptions regarding the age and estimated

useful lives of the Company’s property, plant and equipment.

Intangible Assets — The Company identified the following intangible assets to be valued: (i) franchise marketing rights, (ii)

customer relationships, and (iii) trademarks.

Franchise marketing rights and customer relationships were valued using an income approach and were valued at $5.3 billion and

$2.4 billion, respectively, as of November 30, 2009. See Note 5 to the consolidated financial statements for a description of the

methods used to value intangible assets.

The relief from royalty method was used to value trademarks at $158 million as of November 30, 2009. See Note 5 to the consolidated

financial statements for a description of the methods used to value intangible assets.

Long-Term Debt – Long-term debt was valued at fair value using quoted market prices.

We recorded a pre-tax gain of $5.7 billion resulting from the aggregate changes to the net carrying value of our pre-emergence

assets and liabilities to record their fair values under fresh start accounting. Income tax benefit for the eleven months ended

November 30, 2009 (Predecessor) includes $92 million of benefit related to these adjustments and to gains due to Plan effects.

Reorganization items, net is presented separately in the condensed consolidated statements of operations and represents items of

income, expense, gain or loss that are realized or incurred by the Company because it was in reorganization under Chapter 11 of

the U.S. Bankruptcy Code.