Charter 2011 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2011 Charter annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

|

|

53

actual amount of our capital expenditures depends on completion of an ambitious activity plan and will be subject to the growth

rates of both our residential and commercial businesses.

Our capital expenditures are funded primarily from free cash flow and borrowings on our credit facility. In addition, our liabilities

related to capital expenditures increased by $57 million and $8 million for the years ended December 31, 2011 and 2010, respectively,

and decreased by $10 million for the year ended December 31, 2009.

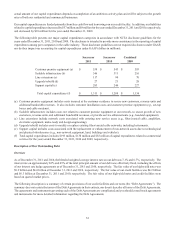

The following table presents our major capital expenditures categories in accordance with NCTA disclosure guidelines for the

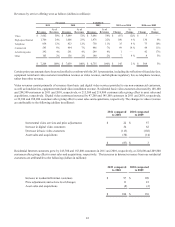

years ended December 31, 2011, 2010 and 2009. The disclosure is intended to provide more consistency in the reporting of capital

expenditures among peer companies in the cable industry. These disclosure guidelines are not required disclosures under GAAP,

nor do they impact our accounting for capital expenditures under GAAP (dollars in millions):

Customer premise equipment (a)

Scalable infrastructure (b)

Line extensions (c)

Upgrade/rebuild (d)

Support capital (e)

Total capital expenditures (f)

Successor

2011

$ 538

346

117

27

283

$ 1,311

Successor

2010

$ 543

311

90

21

244

$ 1,209

Combined

2009

$ 593

216

70

28

227

$ 1,134

(a) Customer premise equipment includes costs incurred at the customer residence to secure new customers, revenue units and

additional bandwidth revenues. It also includes customer installation costs and customer premise equipment (e.g., set-top

boxes and cable modems).

(b) Scalable infrastructure includes costs not related to customer premise equipment or our network, to secure growth of new

customers, revenue units, and additional bandwidth revenues, or provide service enhancements (e.g., headend equipment).

(c) Line extensions include network costs associated with entering new service areas (e.g., fiber/coaxial cable, amplifiers,

electronic equipment, make-ready and design engineering).

(d) Upgrade/rebuild includes costs to modify or replace existing fiber/coaxial cable networks, including betterments.

(e) Support capital includes costs associated with the replacement or enhancement of non-network assets due to technological

and physical obsolescence (e.g., non-network equipment, land, buildings and vehicles).

(f) Total capital expenditures includes $195 million, $138 million and $83 million of capital expenditures related to commercial

services for the years ended December 31, 2011, 2010 and 2009, respectively.

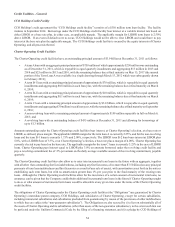

Description of Our Outstanding Debt

Overview

As of December 31, 2011 and 2010, the blended weighted average interest rate on our debt was 7.1% and 6.7%, respectively. The

interest rate on approximately 82% and 65% of the total principal amount of our debt was effectively fixed, including the effects

of our interest rate hedge agreements as of December 31, 2011 and 2010, respectively. The fair value of our high-yield notes was

$9.2 billion and $6.6 billion at December 31, 2011 and 2010, respectively. The fair value of our credit facilities was $4.2 billion

and $6.3 billion at December 31, 2011 and 2010, respectively. The fair value of our high-yield notes and credit facilities were

based on quoted market prices.

The following description is a summary of certain provisions of our credit facilities and our notes (the “Debt Agreements”). The

summary does not restate the terms of the Debt Agreements in their entirety, nor does it describe all terms of the Debt Agreements.

The agreements and instruments governing each of the Debt Agreements are complicated and you should consult such agreements

and instruments for more detailed information regarding the Debt Agreements.