Facebook 2012 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2012 Facebook annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

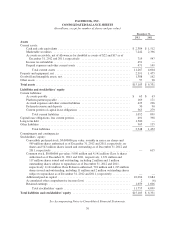

|

|

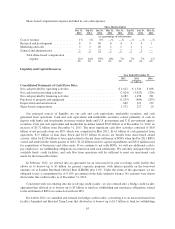

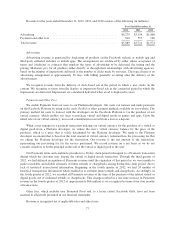

Interest Rate Sensitivity

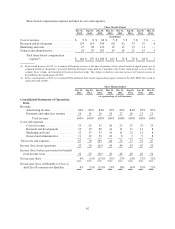

Our exposure to changes in interest rates relates primarily to interest earned and market value on our cash

and cash equivalents and marketable securities and interest paid on our long-term debt.

Our cash and cash equivalents and marketable securities consist of cash, certificates of deposit, time

deposits, money market funds and U.S. government and U.S. government agency securities. Our investment

policy and strategy are focused on preservation of capital and supporting our liquidity requirements. Changes in

U.S. interest rates affect the interest earned on our cash and cash equivalents and marketable securities and the

market value of those securities. A hypothetical 100 basis point increase in interest rates would result in a

decrease of approximately $55 million and $15 million in the market value of our available-for-sale debt

securities as of December 31, 2012 and December 31, 2011, respectively. Any realized gains or losses resulting

from such interest rate changes would only occur if we sold the investments prior to maturity.

Our long-term debt consists of the $1.5 billion draw down on our three-year unsecured term loan facility

that bears variable interest at 1-month LIBOR plus 1.0%. As our risk management objective is to mitigate the

risk of changes in cash flows attributable to changes in the designated 1-month LIBOR for the loan, we have

entered into an interest rate swap agreement for the exact notional amount of $1.5 billion and a fixed interest rate

of 1.46% at the same time the term loan was drawn down to hedge this exposure. Both the term loan and interest

rate swap have a maturity date of October 25, 2015. Changes in the cash flows of the interest rate swap are

expected to exactly offset the changes in cash flows attributable to fluctuations in the 1-month LIBOR based

interest payments on the long-term debt. The net effect of this swap agreement is to convert the variable interest

rate to a fixed rate of 1.46%.

Inflation Risk

We do not believe that inflation has had a material effect on our business, financial condition, or results of

operations.

67