GE 2012 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2012 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

106 GE 2012 ANNUAL REPORT

notes to consolidated financial statements

by asset class and diversification across classes to determine

expected overall portfolio results given current and target allo-

cations. Based on our analysis of future expectations of asset

performance, past return results, our current and target asset

allocations as well as a shorter time horizon for retiree life plan

assets, we have assumed a 7.0% long-term expected return on

those assets for cost recognition in 2013. We apply our expected

rate of return to a market-related value of assets, which stabilizes

variability in the amounts to which we apply that expected return.

We amortize experience gains and losses, as well as the

effects of changes in actuarial assumptions and plan provi-

sions, over a period no longer than the average future service

of employees.

FUNDING POLICY. We fund retiree health benefits on a pay-as-

you-go basis. We expect to contribute approximately $600 million

in 2013 to fund such benefits. We fund the retiree life insurance

trust at our discretion.

Changes in the accumulated postretirement benefit obligation

for retiree benefit plans follow.

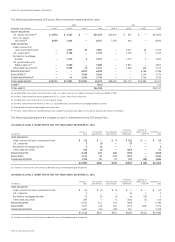

ACCUMULATED POSTRETIREMENT BENEFIT OBLIGATION (APBO)

(In millions) 2012 2011

Balance at January 1 $13,056 $12,010

Service cost for benefits earned 219 216

Interest cost on benefit obligations 491 604

Participant contributions 54 55

Plan amendments (832) 25

Actuarial loss (gain) (60) 911 (a)

Benefits paid (758) (765)

Net curtailment/settlement (366) —

Balance at December 31 (b) $11,804 $13,056

(a) Primarily associated with discount rate change.

(b) The APBO for the retiree health plans was $9,218 million and $10,286 million at

year-end 2012 and 2011, respectively.

A one percentage point change in the assumed healthcare cost

trend rate would have the following effects.

(In millions) 1% Increase 1% Decrease

APBO at December 31, 2012 $1,017 $(860)

Service and interest cost in 2012 76 (63)

PLAN ASSETS

The fair value of the classes of retiree benefit plans’ investments

is presented below. The inputs and valuation techniques used

to measure the fair value of assets are consistently applied and

described in Note 1.

FAIR VALUE OF PLAN ASSETS

(In millions) 2012 2011

Balance at January 1 $1,004 $1,125

Actual gain on plan assets 98 15

Employer contributions 548 574

Participant contributions 54 55

Benefits paid (758) (765)

Balance at December 31 $ 946 $1,004

ASSET ALLOCATION

December 31

2012 Target

allocation

2012 Actual

allocation

Equity securities 35–75% (a) 35% (b)

Debt securities (including cash equivalents) 11–41 40

Private equities 3–13 17

Real estate 2–12 6

Other 0–10 2

(a) Target allocations were 18–38% for U.S. equity securities and 17–37% for

non-U.S. equity securities.

(b) Actual allocations were 22% for U.S. equity securities and 13% for non-U.S.

equity securities.

Plan fiduciaries set investment policies and strategies for the

trust and oversee its investment allocation, which includes

selecting investment managers and setting long-term strategic

targets. The primary strategic investment objectives are balanc-

ing investment risk and return and monitoring the plan’s liquidity

position in order to meet the near-term benefit payment and

other cash needs. Target allocation percentages are established

at an asset class level by plan fiduciaries. Target allocation ranges

are guidelines, not limitations, and occasionally plan fiduciaries

will approve allocations above or below a target range.

Trust assets invested in short-term securities must generally

be invested in securities rated A-1/P-1 or better, except for 15%

of such securities that may be rated A-2/P-2 and other short-term

securities as may be approved by the plan fiduciaries. According

to statute, the aggregate holdings of all qualifying employer

securities (e.g., GE common stock) and qualifying employer real

property may not exceed 10% of the fair value of trust assets at

the time of purchase. GE securities represented 5.8% and 4.7% of

trust assets at year-end 2012 and 2011, respectively.

Retiree life plan assets were $946 million and $1,004 mil-

lion at December 31, 2012 and 2011, respectively. Equity and

debt securities amounting to $741 million and $760 million rep-

resented approximately 75% and 74% of total investments at

December 31, 2012 and 2011, respectively. The plans’ invest-

ments were classified as 28% Level 1, 47% Level 2 and 25%

Level 3 at December 31, 2012. The plans’ investments were classi-

fied as 32% Level 1, 42% Level 2 and 26% Level 3 at December 31,

2011. The changes in Level 3 investments were insignificant for

the years ended December 31, 2012 and 2011.

RETIREE BENEFIT ASSET (LIABILITY)

December 31 (In millions) 2012 2011

Funded status (a) $(10,858) $(12,052)

Liability recorded in the Statement

of Financial Position

Retiree health plans

Due within one year $ (589) $ (602)

Due after one year (8,629) (9,684)

Retiree life plans (1,640) (1,766)

Net liability recognized $(10,858) $(12,052)

Amounts recorded in shareowners’

equity (unamortized)

Prior service cost $ 1,356 $ 2,901

Net actuarial loss 182 401

Total $ 1,538 $ 3,302

(a) Fair value of assets less APBO, as shown in the preceding tables.