GE 2012 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2012 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

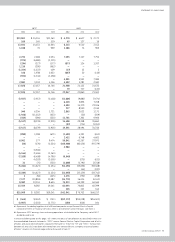

84 GE 2012 ANNUAL REPORT

notes to consolidated financial statements

specific to the attributes of the specific collateral or appraisal

information may not be reflective of current market conditions

due to the passage of time and the occurrence of market events

since receipt of the information. For real estate, fair values are

based on discounted cash flow estimates which reflect current

and projected lease profiles and available industry informa-

tion about capitalization rates and expected trends in rents and

occupancy and are corroborated by external appraisals. These

investments are generally included in Level 3.

RETAINED INVESTMENTS IN FORMERLY CONSOLIDATED

SUBSIDIARIES.

Upon a change in control that results in

deconsolidation of a subsidiary, the fair value measurement of

our retained noncontrolling stake in the former subsidiary is

valued using an income approach, a market approach, or a com-

bination of both approaches, as appropriate. In applying these

methodologies, we rely on a number of factors, including actual

operating results, future business plans, economic projections,

market observable pricing multiples of similar businesses and

comparable transactions, and possible control premium. These

investments are included in Level 1 or Level 3, as appropriate,

determined at the time of the transaction.

Accounting Changes

On January 1, 2012, we adopted FASB Accounting Standards Update

(ASU) 2011-05, an amendment to ASC 220, Comprehensive Income.

ASU 2011-05 introduced a new statement, the Consolidated

Statement of Comprehensive Income. The amendments affect only

the display of those components of equity categorized as other

comprehensive income and do not change existing recognition

and measurement requirements that determine net earnings.

On January 1, 2012, we adopted FASB ASU 2011-04, an

amendment to ASC 820, Fair Value Measurements. ASU 2011-04

clarifies or changes the application of existing fair value mea-

surements, including: that the highest and best use valuation

premise in a fair value measurement is relevant only when mea-

suring the fair value of nonfinancial assets; that a reporting entity

should measure the fair value of its own equity instrument from

the perspective of a market participant that holds that instru-

ment as an asset; to permit an entity to measure the fair value of

certain financial instruments on a net basis rather than based on

its gross exposure when the reporting entity manages its finan-

cial instruments on the basis of such net exposure; that in the

absence of a Level 1 input, a reporting entity should apply premi-

ums and discounts when market participants would do so when

pricing the asset or liability consistent with the unit of account;

and that premiums and discounts related to size as a character-

istic of the reporting entity’s holding are not permitted in a fair

value measurement. Adopting these amendments had no effect

on the financial statements.

On January 1, 2011, we adopted FASB ASU 2009-13 and ASU

2009-14, amendments to ASC 605, Revenue Recognition and ASC

985, Software, respectively, (ASU 2009-13 &14). ASU 2009-13

requires the allocation of consideration to separate components

of an arrangement based on the relative selling price of each

component. ASU 2009-14 requires certain software-enabled

products to be accounted for under the general accounting stan-

dards for multiple component arrangements. These amendments

were effective for new revenue arrangements entered into or

materially modified on or subsequent to January 1, 2011.

Although the adoption of these amendments eliminated the

allocation of consideration using residual values, which was

applied primarily in our Healthcare segment, the overall impact of

adoption was insignificant to our financial statements. In addition,

there are no significant changes to the number of components or

the pattern and timing of revenue recognition following adoption.

On July 1, 2011, we adopted FASB ASU 2011-02, an amend-

ment to ASC 310, Receivables. This ASU provides guidance for

determining whether the restructuring of a debt constitutes a TDR

and requires that such actions be classified as a TDR when there

is both a concession and the debtor is experiencing financial dif-

ficulties. The amendment also clarifies guidance on a creditor’s

evaluation of whether it has granted a concession. The amend-

ment applies to restructurings that have occurred subsequent

to January 1, 2011. As a result of adopting these amendments

on July 1, 2011, we have classified an additional $271 million of

financing receivables as TDRs and have recorded an increase of

$77 million to our allowance for losses on financing receivables.

See Note 23.

On January 1, 2010, we adopted ASU 2009-16 and ASU

2009-17, amendments to ASC 860, Transfers and Servicing, and

ASC 810, Consolidation, respectively (ASU 2009-16 & 17). ASU

2009-16 eliminated the Qualified Special Purpose Entity (QSPE)

concept, and ASU 2009-17 required that all such entities be evalu-

ated for consolidation as VIEs. Adoption of these amendments

resulted in the consolidation of all of our sponsored QSPEs. In

addition, we consolidated assets of VIEs related to direct invest-

ments in entities that hold loans and fixed income securities, a

media joint venture and a small number of companies to which

we have extended loans in the ordinary course of business and

subsequently were subject to a TDR.

We consolidated the assets and liabilities of these enti-

ties at amounts at which they would have been reported in our

financial statements had we always consolidated them. We

also deconsolidated certain entities where we did not meet the

definition of the primary beneficiary under the revised guid-

ance; however, the effect was insignificant at January 1, 2010.

The incremental effect on total assets and liabilities, net of our

investment in these entities, was an increase of $31,097 mil-

lion and $33,042 million, respectively, at January 1, 2010. The

net reduction of total equity (including noncontrolling interests)

was $1,945 million at January 1, 2010, principally related to the

reversal of previously recognized securitization gains as a cumu-

lative effect adjustment to retained earnings. See Note 24 for

additional information.