GE 2012 Annual Report Download - page 131

Download and view the complete annual report

Please find page 131 of the 2012 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

GE 2012 ANNUAL REPORT 129

notes to consolidated financial statements

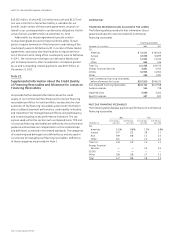

PAST DUE FINANCING RECEIVABLES

The following table displays payment performance of Consumer

financing receivables.

2012 2011

December 31

Over 30 days

past due

Over 90 days

past due (a) Over 30 days

past due

Over 90 days

past due (a)

Non-U.S. residential

mortgages 12.0% 7.5% 12.3% 7.9%

Non-U.S. installment

and revolving credit 3.9 1.1 4.1 1.2

U.S. installment and

revolving credit 4.6 2.0 5.0 2.2

Non-U.S. auto 3.1 0.5 3.1 0.6

Other 2.8 1.7 3.5 2.0

Total 6.5 3.4 6.9 3.7

(a) Included $24 million and $45 million of loans at December 31, 2012 and 2011,

respectively, which are over 90 days past due and accruing interest, mainly

representing accretion on loans acquired at a discount.

NONACCRUAL FINANCING RECEIVABLES

The following table provides further information about Consumer

financing receivables that are classified as nonaccrual.

Nonaccrual financing

receivables

Nonearning financing

receivables

December 31 (Dollars in millions) 2012 2011 2012 2011

Non-U.S. residential

mortgages $2,600 $2,995 $2,569 $2,870

Non-U.S. installment

and revolving credit 224 321 224 263

U.S. installment and

revolving credit 1,026 990 1,026 990

Non-U.S. auto 24 43 24 43

Other 427 487 351 419

Total $4,301 $4,836 $4,194 $4,585

Allowance for losses

percentage 84.3% 73.8% 86.4% 77.9%

IMPAIRED LOANS

The vast majority of our Consumer nonaccrual financing

receivables are smaller balance homogeneous loans evaluated

collectively, by portfolio, for impairment and therefore are out-

side the scope of the disclosure requirement for impaired loans.

Accordingly, impaired loans in our Consumer business represent

restructured smaller balance homogeneous loans meeting the

definition of a TDR, and are therefore subject to the disclosure

requirement for impaired loans, and commercial loans in our

Consumer—Other portfolio. The recorded investment of these

impaired loans totaled $3,220 million (with an unpaid principal

balance of $3,269 million) and comprised $105 million with no

specific allowance, primarily all in our Consumer—Other portfolio,

and $3,115 million with a specific allowance of $674 million at

December 31, 2012. The impaired loans with a specific allowance

included $309 million with a specific allowance of $83 million in

our Consumer—Other portfolio and $2,806 million with a spe-

cific allowance of $591 million across the remaining Consumer

business and had an unpaid principal balance and average

investment of $3,152 million and $2,956 million, respectively, at

December 31, 2012. We recognized $169 million and $141 million

of interest income, including $5 million and $15 million on a cash

basis, for the years ended December 31, 2012 and 2011, respec-

tively, principally in our Consumer—Non-U.S. and U.S. installment

and revolving credit portfolios. The total average investment in

impaired loans for the years ended December 31, 2012 and 2011

was $3,056 million and $2,623 million, respectively.

Impaired loans classified as TDRs in our Consumer business

were $3,053 million and $2,723 million at December 31, 2012 and

2011, respectively. We utilize certain loan modification programs

for borrowers experiencing financial difficulties in our Consumer

loan portfolio. These loan modification programs primarily include

interest rate reductions and payment deferrals in excess of three

months, which were not part of the terms of the original con-

tract, and are primarily concentrated in our non-U.S. residential

mortgage and U.S. credit card portfolios. For the year ended

December 31, 2012, we modified $1,756 million of consumer loans

for borrowers experiencing financial difficulties, which are classified

as TDRs, and included $1,186 million of non-U.S. consumer loans,

primarily residential mortgages, credit cards and personal loans

and $570 million of U.S. consumer loans, primarily credit cards. We

expect borrowers whose loans have been modified under these

programs to continue to be able to meet their contractual obliga-

tions upon the conclusion of the modification. Of our $1,756 million

of modifications classified as TDRs during 2012, $334 million have

subsequently experienced a payment default in 2012, primarily in

our installment and revolving credit portfolios. Of our $1,924 million

of modifications classified as TDRs during 2011, $240 million have

subsequently experienced a payment default in 2011.