HSBC 2006 Annual Report Download - page 178

Download and view the complete annual report

Please find page 178 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

Report of the Directors: The Management of Risk (continued)

Credit risk > Credit risk management / Exposure

176

Collectively assessed allowances are generally

calculated monthly and charges for new allowances,

or reversals of existing allowances, are determined

for each separately identified portfolio.

Impairment allowances

When impairment losses occur, HSBC reduces the

carrying amount of loans and advances and held-to-

maturity financial investments through the use of an

allowance account. When impairment of available-

for-sale financial assets occurs, the carrying amount

of the asset is reduced directly.

Loan write-offs

Loans, and the related impairment allowances, are

normally written off, either partially or in full, in the

case of that portion of the loan amount not covered

by the value of security, when there is no realistic

prospect of further recovery; and in the case of

secured balances, after proceeds from the realisation

of security have been received. Unsecured consumer

facilities are normally written off between 150 and

210 days overdue. In HSBC Finance, this period is

generally extended to 300 days overdue (240 days

for real estate secured products).

Instances of write-off periods exceeding

360 days overdue are few, but can arise where

certain consumer finance accounts are deemed

collectible beyond this point or where, in a few

countries, regulation or legislation constrain earlier

write-off.

In the event of bankruptcy, or analogous

proceedings, write-off can occur earlier.

Cross-border exposures

Management assesses the vulnerability of countries

to foreign currency payment restrictions when

considering impairment allowances on cross-border

exposures. This assessment includes an analysis of

the economic and political factors existing at the

time. Economic factors include the level of external

indebtedness, the debt service burden and access to

external sources of funds to meet the debtor

country’s financing requirements. Political factors

taken into account include the stability of the country

and its government, threats to security, and the

quality and independence of the legal system.

Impairment allowances are applied to all

qualifying exposures within these countries unless

these exposures and the inherent risks are:

• performing, trade-related and of less than one

year’s maturity;

• mitigated by acceptable security cover which is,

other than in exceptional cases, held outside the

country concerned;

• in the form of securities held for trading

purposes for which a liquid and active market

exists, and which are measured at fair value

daily;

• performing facilities with principal (excluding

security) of US$1 million or below; or

• performing facilities with maturity dates shorter

than three months.

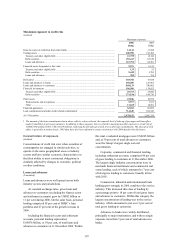

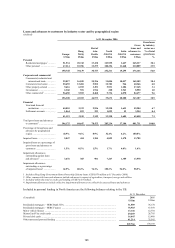

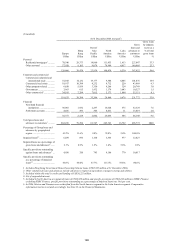

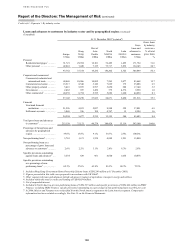

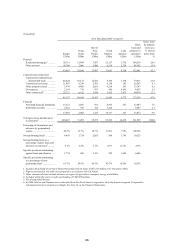

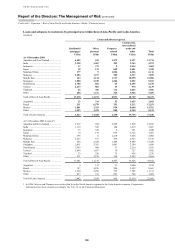

Credit exposure

Maximum exposure to credit risk

(Audited)

Factors which had a direct impact on changes in

HSBC’s maximum exposure to credit risk during

2006 related to the curtailment of growth in

mortgage lending in the US in response to

deteriorating conditions, and slowed growth in UK

personal unsecured lending following an increase in

personal bankruptcies and IVAs. Elsewhere, growth

reflected underlying economic trends on a

geographic basis.

The following table presents the maximum

exposure to credit risk of balance sheet and off

balance sheet financial instruments, before taking

account of any collateral held or other credit

enhancements unless such credit enhancements meet

offsetting requirements as set out in Note 2(m) on

the Financial Statements. For financial assets

recognised on the balance sheet, the exposure to

credit risk equals their carrying amount. For

financial guarantees granted, the maximum exposure

to credit risk is the maximum amount that HSBC

would have to pay if the guarantees are called upon.

For loan commitments and other credit related

commitments that are irrevocable over the life of the

respective facilities, the maximum exposure to credit

risk is the full amount of the committed facilities.