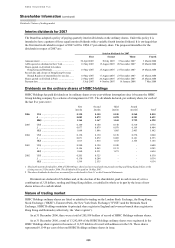

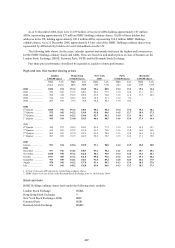

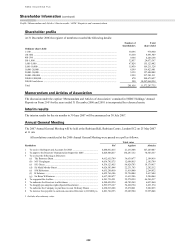

HSBC 2006 Annual Report Download - page 434

Download and view the complete annual report

Please find page 434 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

432 -

433

433 -

434

434 -

435

435 -

436

436 -

437

437 -

438

438 -

439

439 -

440

440 -

441

441 -

442

442 -

443

443 -

444

444 -

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

Note 47

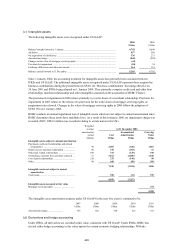

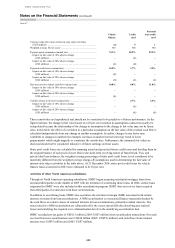

432

Vehicle

finance

Credit

card

Personal

non-credit

card

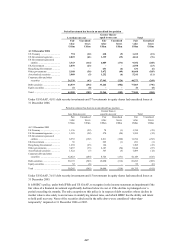

Carrying value (fair value) of interest-only strip receivables

(US$ millions) .................................................................................... (4) 9 1

Weighted average life (in years) ............................................................. 0.7 0.3 0.3

Payment speed assumption (annual rate) ................................................ 74.3% 98.9% 99.2%

Impact on fair value of 10% adverse change

(US$ millions) ................................................................................ – (1) –

Impact on fair value of 20% adverse change

(US$ millions) ................................................................................ (1) (2) –

Expected credit losses (annual rate) ....................................................... 10.0% 3.7% 9.8%

Impact on fair value of 10% adverse change

(US$ millions) ................................................................................ (2) – –

Impact on fair value of 20% adverse change

(US$ millions) ................................................................................ (3) (1) (1)

Discount rate for residual cash flows (annual rate) ................................ 10.0% 9.0% 11.0%

Impact on fair value of 10% adverse change

(US$ millions) ................................................................................ – – –

Impact on fair value of 20% adverse change

(US$ millions) ................................................................................ (1) – –

Variable returns to investors (annual rate) ............................................. – 4.7% 6.0%

Impact on fair value of 10% adverse change

(US$ millions) ................................................................................ – (1) –

Impact on fair value of 20% adverse change

(US$ millions) ................................................................................ – (1) (1)

These sensitivities are hypothetical and should not be considered to be predictive of future performance. As the

figures indicate, the change in fair value based on a 10 per cent variation in assumptions cannot necessarily be

extrapolated because the relationship of the change in assumption to the change in fair value may not be linear.

Also, in this table, the effect of a variation in a particular assumption on the fair value of the residual cash flow is

calculated independently from any change in another assumption. In reality, changes in one factor may

contribute to changes in another (for example, increases in market interest rates may result in lower

prepayments) which might magnify or counteract the sensitivities. Furthermore, the estimated fair values as

disclosed should not be considered indicative of future earnings on these assets.

Static pool credit losses are calculated by summing actual and projected future credit losses and dividing them by

the original balance of each pool of asset. Due to the short-term revolving nature of MasterCard, Visa, and

private label loan balances, the weighted average percentage of static pool credit losses is not considered to be

materially different from the weighted average charge-off assumptions used in determining the fair value of

interest-only strip receivables in the table above. At 31 December 2006, static pool credit losses for vehicle

finance loans securitised in 2003 were estimated to be 10 per cent.

Activities of other North American subsidiaries

Through its North American operating subsidiaries, HSBC began acquiring residential mortgage loans from

unrelated third parties in the middle of 2005 with the intention of securitising those loans. In 2006, certain loans

originated by HSBC were also included in this securitisation program. HSBC does not service loans acquired

from third parties in connection with these securitisations.

In addition to securitising loans, HSBC also securitises the net interest margin (NIM) associated with certain

interests it retains from loan securitisations. A NIM securitisation is a structured finance transaction backed by

the cash flows on certain classes of retained interests in loan securitisations, primarily residual interests. The

notes issued in a NIM securitisation are collateralised by the excess spread left after absorbing any realised

losses and satisfying the required over collateralisation levels in the underlying securitisation deal.

HSBC recorded pre-tax gains of US$113 million (2005: US$3 million) from securitisation transactions. Proceeds

received from new securitisations were US$18 billion (2005: US$576 million), and cash flows from retained

interests were US$35 million and (2005: US$7 million).