HSBC 2006 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

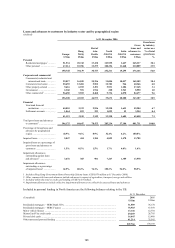

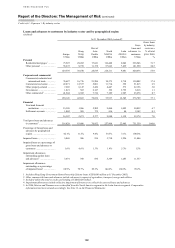

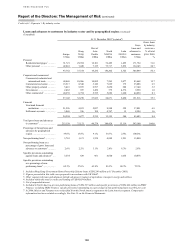

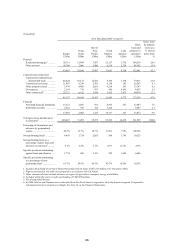

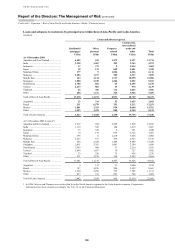

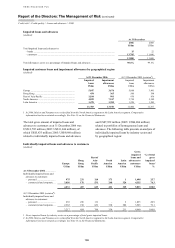

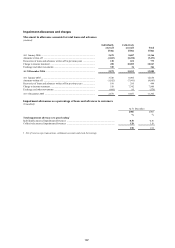

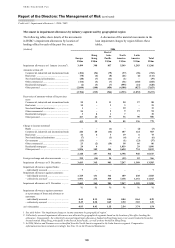

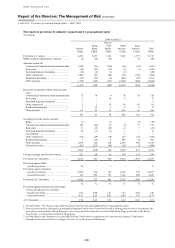

HSBC HOLDINGS PLC

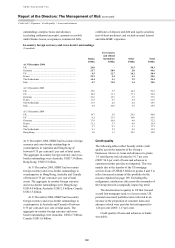

Report of the Directors: The Management of Risk (continued)

Credit risk > Exposure > Areas of special interest / Cross-border distribution

190

1 HSBC Finance includes lending in Canada and the UK and excludes loans transferred to HSBC USA Inc.

2 Total mortgage lending includes residential mortgages and second lien mortgage lending included within ‘Other personal lending’.

3 Loan to value ratios are generally based on values at origination date.

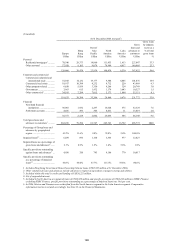

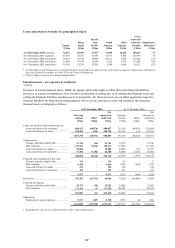

Mortgage lending in the US

(Unaudited)

Mortgage lending in the US includes loans and

advances to customers with a first lien interest over

a property. These balances are secured and are

reported within residential mortgages. Loans with

only a second lien are reported in other personal

lending. The commentary that follows discusses both

residential mortgages and second lien loans included

within other personal lending.

HSBC continues to monitor a range of trends

affecting the US mortgage lending industry. Housing

markets in a large part of the US have been affected

by a general slowing in the rate of appreciation in

property values, or an actual decline in some

markets, while the period of time properties remain

unsold has increased. In addition, the ability of some

borrowers to service their adjustable-rate mortgages

(‘ARM’s) has been compromised as interest rates

have risen, increasing the amounts payable on their

loans as prices reset higher under their contracts. The

effect of interest rate adjustments on first mortgages

are also estimated to have had a direct impact on

borrowers’ ability to repay any additional second

lien mortgages taken out on the same properties.

Similarly, as interest-only mortgages leave the

interest-only payment period, rising payment

obligations are expected to strain the ability of

borrowers to make the increased payments. Studies

published in the US, and HSBC’s own experience,

indicate that mortgages originated throughout the

industry in 2005 and 2006 are performing worse than

loans originated in prior periods.

The effects of these recent trends have been

concentrated in the mortgage services business

(‘mortgage services’), which purchases first and

second lien mortgages from a network of over

220 third party lenders. As detailed in the

table below, this business has approximately

US$49.5 billion of loans and advances to personal

customers, 10.4 per cent of the Group’s gross loans

and advances to personal customers.

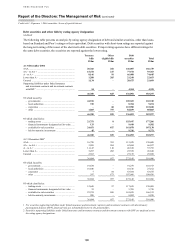

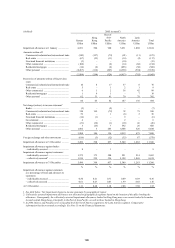

In 2005 and continuing into the first six months

of 2006, second lien mortgage loans in mortgage

services increased significantly as a percentage of

total loans acquired compared with prior periods.

During the second quarter of 2006 HSBC began to

experience deterioration in the credit performance of

mortgages acquired in 2005 by mortgage services in

the second lien and portions of the first lien

portfolios. The deterioration continued in the third

quarter of 2006 and began to affect second and first

lien loans acquired in that year. Further deterioration

in the fourth quarter of 2006 was largely in the first

lien adjustable-rate and second lien portfolios.

HSBC also determined that a significant number of

its second lien customers have underlying

adjustable-rate first mortgages that face repricing in

the near-term which, based on experience, are

estimated to adversely affect the probability of

repayment on the related second lien mortgage. As

numerous interest rate rises have occurred as credit

has tightened and there has been either a slowdown

in the rate of appreciation of properties or a decline

in their value, it is estimated that the probability of

default on adjustable-rate first mortgages subject to

repricing, and on any second lien mortgage loans

that are subordinate to adjustable-rate first liens, is

greater than has been experienced in the past. As a

result, loan impairment charges relating to the

mortgage services portfolio have increased

significantly.

Accordingly, while overall credit performance,

as measured by delinquency and write-off rates, has

performed broadly in line with industry trends across

other parts of the US mortgage portfolio, higher

delinquency and losses have been reported in

mortgage services, largely in the aforementioned

loans originated in 2005 and 2006. A number of

steps have been taken to mitigate risk in the affected

parts of the portfolio. These include enhanced

segmentation and analytics to identify the higher risk

portions of the portfolio, and increased collections

capacity. HSBC is restructuring or modifying loans

in accordance with defined policies if it believes that

customers will continue to pay the restructured or

modified loan. Also, customers who have adjustable-

rate mortgage loans nearing the first reset, and who

are expected to be the most affected by a rate

adjustment, are being contacted in order to assess

their ability to make the higher payment and, as

appropriate, refinance or modify their loans.

Furthermore, HSBC has slowed growth in this

portion of the portfolio by implementing repricing

initiatives in selected segments of the originated

loans and tightening underwriting criteria, especially

for second lien, stated income (low documentation)

and other higher risk segments. These actions,

combined with normal attrition, resulted in a net

reduction in loans and advances in mortgage services

during the second half of 2006. It is expected that

this portfolio will remain under pressure as the loans

originated in 2005 and 2006 season. It is also

expected that this portfolio will run off faster than in