Humana 2007 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2007 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

|

|

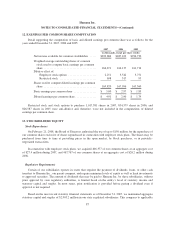

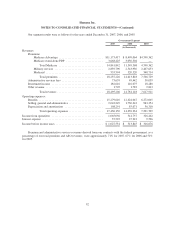

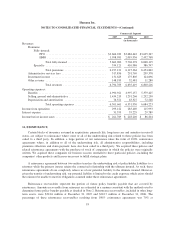

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Commercial Segment

2007 2006 2005

(in thousands)

Revenues:

Premiums:

Fully-insured:

PPO .......................................... $3,664,019 $3,684,442 $3,635,347

HMO ......................................... 1,998,981 2,019,936 2,432,768

Total fully-insured ........................... 5,663,000 5,704,378 6,068,115

Specialty .......................................... 534,121 410,986 386,747

Total premiums ............................. 6,197,121 6,115,364 6,454,862

Administrative services fees ............................... 317,856 291,769 209,378

Investment income ...................................... 131,623 175,805 124,696

Other revenue .......................................... 148,183 52,481 11,280

Total revenues .............................. 6,794,783 6,635,419 6,800,216

Operating expenses:

Benefits ............................................... 4,990,921 4,997,157 5,379,425

Selling, general and administrative .......................... 1,434,219 1,291,266 1,232,250

Depreciation and amortization ............................. 76,521 63,527 72,548

Total operating expenses ...................... 6,501,661 6,351,950 6,684,223

Income from operations ...................................... 293,122 283,469 115,993

Interest expense ............................................. 31,353 35,229 29,789

Income before income taxes ................................... $ 261,769 $ 248,240 $ 86,204

16. REINSURANCE

Certain blocks of insurance assumed in acquisitions, primarily life, long-term care and annuities in run-off

status, are subject to reinsurance where some or all of the underwriting risk related to these policies has been

ceded to a third party. In addition, a large portion of our reinsurance takes the form of 100% coinsurance

agreements where, in addition to all of the underwriting risk, all administrative responsibilities, including

premium collections and claim payment, have also been ceded to a third party. We acquired these policies and

related reinsurance agreements with the purchase of stock of companies in which the policies were originally

written. We acquired these companies for business reasons unrelated to these particular policies, including the

companies’ other products and licenses necessary to fulfill strategic plans.

A reinsurance agreement between two entities transfers the underwriting risk of policyholder liabilities to a

reinsurer while the primary insurer retains the contractual relationship with the ultimate insured. As such, these

reinsurance agreements do no completely relieve us of our potential liability to the ultimate insured. However,

given the transfer of underwriting risk, our potential liability is limited to the credit exposure which exists should

the reinsurer be unable to meet its obligations assumed under these reinsurance agreements.

Reinsurance recoverables represent the portion of future policy benefits payable that are covered by

reinsurance. Amounts recoverable from reinsurers are estimated in a manner consistent with the methods used to

determine future policy benefits payable as detailed in Note 2. Reinsurance recoverables, included in other long-

term assets, were $341.6 million at December 31, 2007 and $242.7 million at December 31, 2006. The

percentage of these reinsurance recoverables resulting from 100% coinsurance agreements was 70% at

93