Humana 2007 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2007 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

|

|

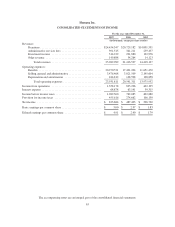

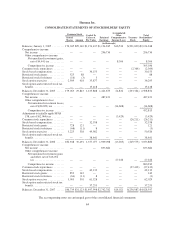

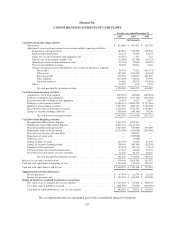

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

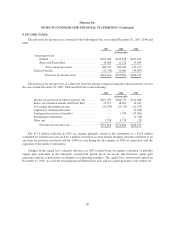

Earnings Per Common Share

We compute basic earnings per common share on the basis of the weighted average number of unrestricted

common shares outstanding. Diluted earnings per common share is computed on the basis of the weighted

average number of unrestricted common shares outstanding plus the dilutive effect of outstanding employee

stock options and restricted shares using the treasury stock method.

Recently Issued Accounting Pronouncements

In December 2007, the Financial Accounting Standards Board, or FASB, issued FASB Statement No. 141

(Revised 2007), Business Combination, or SFAS 141R. SFAS 141R will significantly change the accounting for

business combinations. Under SFAS 141R, an acquiring entity will be required to recognize all the assets

acquired and liabilities assumed in a transaction at the acquisition-date fair value with limited exceptions. SFAS

141R will change the accounting treatment for certain specific items including expensing transaction and

restructuring costs and adjusting earnings in periods subsequent to the acquisition for changes in deferred tax

asset valuation allowances and income tax uncertainties as well as changes in the fair value of acquired

contingent liabilities. SFAS 141R also includes a substantial number of new disclosure requirements. SFAS

141R applies prospectively to business combinations for which the acquisition date is on or after January 1, 2009

with early adoption prohibited.Accordingly, we are required to record and disclose business combinations

following existing GAAP until January 1, 2009. We currently are evaluating the provisions of SFAS 141R.

In December 2007, the FASB issued FASB Statement No. 160, Noncontrolling Interests in Consolidated

Financial Statements—An Amendment of ARB No. 5, or SFAS 160.SFAS 160 establishes new accounting and

reporting standards for the noncontrolling interest in a subsidiary and for the deconsolidation of a subsidiary.

Specifically, SFAS 160 requires the recognition of a noncontrolling interest (minority interest) as equity and

separate from the parent’s equity. The amount of net income attributable to the noncontrolling interest will be

included in consolidated net income on the face of the income statement. SFAS 160 is effective for fiscal years,

and interim periods within those fiscal years, beginning January 1, 2009. Like SFAS 141R discussed above,

earlier adoption is prohibited. We currently are evaluating the provisions of SFAS 160.

In February 2007, the FASB issued Statement of Financial Accounting Standards No. 159, The Fair Value

Option for Financial Assets and Financial Liabilities, or SFAS 159. SFAS 159 allows us an option to report

selected financial assets and liabilities at fair value and establishes related presentation and disclosure

requirements. We were required to make an election regarding this fair value option in the first quarter of 2008,

and we did not elect to adopt this fair value option under SFAS 159.

In September 2006, the FASB issued Statement of Financial Accounting Standards No. 157, Fair Value

Measurements, or SFAS 157. SFAS 157 defines fair value, establishes a framework for measuring fair value, and

expands disclosures about fair value measurements. SFAS 157 does not require new fair value measurements.

We adopted SFAS 157 on January 1, 2008. The adoption of SFAS 157 did not have a material impact on our

financial position or results of operations. We are evaluating the disclosure provisions of SFAS 157 required in

connection with the filing of our first quarter 2008 Form 10-Q.

Reclassification

The balance sheet reflects the reclassification of future policy benefits payable to conform to the current

year presentation.

73