Humana 2007 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2007 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

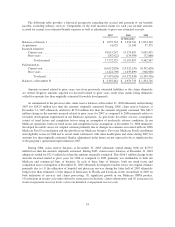

|

|

amount, or target cost, with the federal government and determine an underwriting fee. Any variance from the

target cost is shared. We earn more revenue or incur additional costs based on the variance in actual health care

costs versus the negotiated target cost. We receive 20% for any cost underrun, subject to a ceiling that limits the

underwriting profit to 10% of the target cost. We pay 20% for any cost overrun, subject to a floor that limits the

underwriting loss to negative 4% of the target cost. A final settlement occurs 12 to 18 months after the end of

each contract year to which it applies. We defer the recognition of any revenues for favorable contingent

underwriting fee adjustments related to cost underruns until the amount is determinable and the collectibility is

reasonably assured. We estimate and recognize unfavorable contingent underwriting fee adjustments related to

cost overruns currently in operations as an increase in benefit expenses. We continually review these benefit

expense estimates of future payments to the government for cost overruns and make necessary adjustments to our

reserves.

The military services contracts contain provisions to negotiate change orders. Change orders occur when we

perform services or incur costs under the directive of the federal government that were not originally specified in

our contract. Under federal regulations we may be entitled to an equitable adjustment to the contract price in

these situations. Change orders may be negotiated and settled at any time throughout the year. We record revenue

applicable to change orders when services are performed and these amounts are determinable and the

collectibility is reasonably assured.

Investment Securities

Investment securities totaled $4,650.4 million, or 36% of total assets at December 31, 2007. Debt securities

totaled $4,639.1 million, or nearly 100% of this investment portfolio. More than 98% of our debt securities were

of investment-grade quality, with an average credit rating of AA+ by S&P at December 31, 2007. Most of the

debt securities that are below investment grade are rated at the higher end (BB or better) of the non-investment

grade spectrum. We have minimal exposure to sub-prime mortgages as we acceded to approximately $8 million

of sub-prime and second-lien mortgages with our acquisition of KMG in the fourth quarter of 2007. However, by

the end of January 2008, we had reduced that amount to approximately $4 million of sub-prime mortgages, each

of which have maintained at least an AA+ rating after subsequent reviews by the rating agencies. There are no

collateralized debt obligations or structured investment vehicles in our investment portfolio. Our investment

policy limits investments in a single issuer and requires diversification among various asset types.

Duration is indicative of the relationship between changes in market value and changes in interest rates,

providing a general indication of the sensitivity of the fair values of our debt securities to changes in interest

rates. However, actual market values may differ significantly from estimates based on duration. The average

duration of our debt securities was approximately 3.9 years at December 31, 2007. Given that short term interest

rates were higher than long term rates during most of 2007, cash was invested in cash equivalents instead of

longer duration investment securities. Including cash equivalents, the average duration was approximately

2.6 years. Based on the duration including cash equivalents, a 1% increase in interest rates would generally

decrease the fair value of our securities by approximately $172 million.

Our investment securities, which consist primarily of debt securities, have been categorized as available for

sale and, as a result, are stated at fair value. Fair value of actively traded debt and equity securities are based on

quoted market prices. Fair value of inactively traded debt securities are based on quoted market prices of

identical or similar securities or based on observable inputs like interest rates. Fair value of privately held debt

securities, including venture capital investments are estimated using a variety of valuation methodologies where

an observable quoted market does not exist. Such methodologies include reviewing the value ascribed to the most

recent financing, comparing the security with securities of publicly traded companies in a similar line of

business, and reviewing the underlying financial performance including estimating discounted cash flows.

Investment securities available for current operations are classified as current assets. Unrealized holding gains

and losses, net of applicable deferred taxes, are included as a component of stockholders’ equity and

comprehensive income until realized from a sale or other than temporary impairment.

58