Nike 2011 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2011 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

19NIKE,INC.-Form10-K

PARTII

ITEM7Management’s Discussion and Analysis of Financial Condition and Results of Operations

The reported futures and advance orders growth is not necessarily indicative

of our expectation of revenue growth during this period. This is due toyear-

over-year changes in shipment timing and because the mix of orders can shift

between advance/futures and at-once orders and the fulfi llment of certain

orders may fall outside of the schedule noted above. In addition, exchange

rate fl uctuations as well as differing levels of order cancellations and discounts

can cause differences in the comparisons between advance/futures orders and

actual revenues. Moreover, a signifi cant portion of our revenue is not derived

from futures and advance orders, including at-once and close-out sales of

NIKE Brand footwear and apparel, sales of NIKE Brand equipment, sales from

our Direct to Consumer operations, and sales from our Other Businesses.

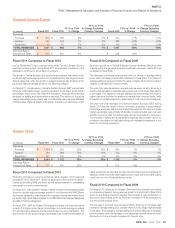

Gross Margin

(Inmillions)

Fiscal2011 Fiscal2010

FY11vs. FY10

%Change Fiscal2009

FY10vs. FY09

%Change

Gross Margin $ 9,508 $ 8,800 8 % $ 8,604 2 %

Gross Margin % 45.6 % 46.3 % (70 )bps 44.9 % 140 bps

Fiscal 2011 Compared to Fiscal 2010

For fi scal2011, our consolidated gross margin percentage was 70 basis

points lower than the prioryear. The primary factors contributing to this

decrease were as follows:

• Higher input costs across most businesses,

•

Increased transportation costs, including additional air freight incurred to

meet strong demand for NIKE Brand products across most businesses,

most notably in North America, Western Europe, and Central& Eastern

Europe geographies, and

•

A lower mix of licensee revenue as distribution for certain markets within our

Other Businesses transitioned from licensees to operating units of NIKE,Inc.

Together, these factors decreased consolidated gross margins by approximately

130 basis points for fi scal2011, with the most signifi cant erosion in the second

half of the fi scalyear. These decreases were partially offset by the positive

impact from the growth and expanding profi tability of our NIKE Brand Direct

to Consumer business, a higher mix of full-price sales and favorable impacts

from our ongoing product cost effi ciency initiatives.

As we head into fi scal2012, we anticipate that our gross margins will continue

to face pressure from macroeconomic factors, most notably rising product

input costs as well as higher transportation costs, which may more than

offset the favorable impact from our planned price increases and ongoing

production cost effi ciency initiatives.

Fiscal 2010 Compared to Fiscal 2009

For fi scal2010, our consolidated gross margin percentage was 140 basis

points higher than the prioryear. The primary factors contributing to this

improvement were as follows:

•

Improved in-line product margins across most geographies, driven by reduced

raw material and freight costs as well as favorable changes in product mix,

• Improved inventory positions, most notably in North America and Western

Europe, which drove a shift in mix from discounted close-out to higher

margin in-line sales, and

•

Growth of NIKE-owned retail as a percentage of total revenue, across most

NIKE Brand geographies, driven by an increase in both new store openings

and comparable store sales.

Together, these factors increased consolidated gross margins by approximately

160basis points for fi scal2010. These increases were partially offset by the

impact of unfavorable currency exchange rates, primarily affecting our Emerging

Markets and Central& Eastern Europe geographies.

Selling and Administrative Expense

(Inmillions)

Fiscal2011 Fiscal2010

FY11vs. FY10

% Change Fiscal2009

FY10vs. FY09

%Change

Demand creation expense

(1) $ 2,448 $ 2,356 4 % $ 2,352 0 %

Operating overhead expense 4,245 3,970 7 % 3,798 5 %

Selling and administrative expense $ 6,693 $ 6,326 6 % $ 6,150 3 %

% of Revenues 32.1 % 33.3 % (120 )bps 32.1 % 120 bps

(1) Demand creation consists of advertising and promotion expenses, including costs of endorsement contracts.

Fiscal 2011 Compared to Fiscal 2010

In fi scal2011, the effect of changes in foreign currency exchange rates did

not have a signifi cant impact on selling and administrative expense.

Demand creation expense increased 4% compared to the prioryear, primarily

driven by a higher level of brand event spending around the World Cup and

World Basketball Festival in the fi rst half of fi scal2011, as well as increased

spending around key product initiatives and investments in retail product

presentation with wholesale customers.

Operating overhead expense increased 7% compared to the prioryear.

Thisincrease was primarily attributable to increased investments in our Direct

to Consumer operations as well as growth in our wholesale operations, where

we incurred higher personnel costs and travel expenses as compared to the

prioryear.

Fiscal 2010 Compared to Fiscal 2009

In fi scal2010, changes in currency exchange rates had a minimal impact on

demand creation expense. Demand creation expense remained fl at compared

to the prioryear, as increases in sports marketing and digital marketing

expenses were offset by reductions in advertising.

Excluding changes in exchange rates, operating overhead expense increased

4% compared to the prioryear due primarily to increases in performance-

based compensation and investments in our Direct to Consumer operations.

These increases were partially offset by reductions in compensation spending

in fi scal2010 as a result of restructuring activities that took place in the fourth

quarter of fi scal2009.