Nike 2011 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2011 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

44 NIKE,INC.-Form10-K

PARTII

Note4Identifi able Intangible Assets, Goodwill and Umbro Impairment

NOTE4 Identifi able Intangible Assets, Goodwill and Umbro Impairment

Identifi ed Intangible Assets and Goodwill

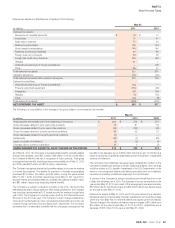

The following table summarizes the Company’s identifi able intangible asset balances as of May31,2011 and 2010:

(Inmillions)

May31,2011 May31,2010

Gross Carrying

Amount

Accumulated

Amortization

Net Carrying

Amount

Gross Carrying

Amount

Accumulated

Amortization

Net Carrying

Amount

Amortized intangible assets:

Patents $ 80 $ (24) $ 56 $ 69 $ (21) $ 48

Trademarks 44 (25) 19 40 (18) 22

Other 47 (22) 25 32 (18) 14

TOTAL $ 171 $ (71)$ 100 $ 141 $ (57)$84

Unamortized intangible assets—

Trademarks 387 383

IDENTIFIABLE INTANGIBLE

ASSETS, NET $ 487 $ 467

The effect of foreign exchange fl uctuations for the year ended May31,2011 increased unamortized intangible assets by approximately $4million.

Amortization expense, which is included in selling and administrative

expense, was $16million, $14million, and $12million fortheyears ended

May31,2011,2010, and 2009, respectively. The estimated amortization

expense for intangible assets subject to amortization for each of theyears

ending May31,2012 through May31,2016 are as follows:2012: $16million;

2013: $14million; 2014: $12million; 2015: $8million; 2016: $7million.

All goodwill balances are included in the Company’s “Other” category for segment reporting purposes. The following table summarizes the Company’s goodwill

balance as of May31,2011 and 2010:

(Inmillions)

Goodwill

Accumulated

Impairment Goodwill,net

May31,2009 $ 393 $ (199) $ 194

Other(1) (6) — (6)

May31,2010 387 (199) 188

Umbro France(2) 10 — 10

Other(1) 7 — 7

MAY31,2011 $ 404 $ (199) $ 205

(1) Other consists of foreign currency translation adjustments on Umbro goodwill.

(2) In March2011, Umbro acquired the remaining 51% of the exclusive licensee and distributor of the Umbro brand in France for approximately $15million.

Umbro Impairment in Fiscal 2009

The Company performs annual impairment tests on goodwill and intangible

assets with indefi nite lives in the fourth quarter of each fi scal year, or when events

occur or circumstances change that would, more likely than not, reduce the

fair value of a reporting unit or intangible assets with an indefi nite life below its

carrying value. As a result of a signifi cant decline in global consumer demand and

continued weakness in the macroeconomic environment, as well as decisions

by Company management to adjust planned investment in the Umbro brand,

the Company concluded suffi cient indicators of impairment existed to require the

performance of an interim assessment of Umbro’s goodwill and indefi nite lived

intangible assets as of February1,2009. Accordingly, the Company performed

the fi rst step of the goodwill impairment assessment for Umbro by comparing

the estimated fair value of Umbro to its carrying amount, and determined there

was a potential impairment of goodwill as the carrying amount exceeded the

estimated fair value. Therefore, the Company performed the second step of

the assessment which compared the implied fair value of Umbro’s goodwill to

the book value of goodwill. The implied fair value of goodwill is determined by

allocating the estimated fair value of Umbro to all of its assets and liabilities,

including both recognized and unrecognized intangibles, in the same manner

as goodwill was determined in the original business combination.

The Company measured the fair value of Umbro by using an equal weighting of

the fair value implied by a discounted cash fl ow analysis and by comparisons with

the market values of similar publicly traded companies. The Company believes the

blended use of both models compensates for the inherent risk associated with

either model if used on a stand-alone basis, and this combination is indicative

of the factors a market participant would consider when performing a similar

valuation. The fair value of Umbro’s indefi nite-lived trademark was estimated

using the relief from royalty method, which assumes that the trademark has

value to the extent that Umbro is relieved of the obligation to pay royalties for

the benefi ts received from the trademark. The assessments of the Company

resulted in the recognition of impairment charges of $199million and $181million

related to Umbro’s goodwill and trademark, respectively, for the year ended

May31,2009. A tax benefi t of $55million was recognized as a result of the

trademark impairment charge. In addition to the above impairment analysis, the

Company determined an equity investment held by Umbro was impaired, and

recognized a charge of $21million related to the impairment of this investment.

These charges are included in the Company’s “Other” category for segment

reporting purposes.

The discounted cash fl ow analysis calculated the fair value of Umbro using

management’s business plans and projections as the basis for expected cash

fl ows for the next 12years and a 3% residual growth rate thereafter. TheCompany

used a weighted average discount rate of 14% in its analysis, which was derived

primarily from published sources as well as our adjustment for increased

market risk given current market conditions. Other signifi cant estimates used

in the discounted cash fl ow analysis include the rates of projected growth and

profi tability of Umbro’s business and working capital effects. The market valuation

approach indicates the fair value of Umbro based on a comparison of Umbro

to publicly traded companies in similar lines of business. Signifi cant estimates

in the market valuation approach include identifying similar companies with

comparable business factors such as size, growth, profi tability, mix of revenue

generated from licensed and direct distribution, and risk of return on investment.

Holding all other assumptions constant at the test date, a 100 basis point increase

in the discount rate would reduce the adjusted carrying value of Umbro’s net

assets by an additional 12%.