Nike 2011 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2011 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

|

|

54 NIKE,INC.-Form10-K

PARTII

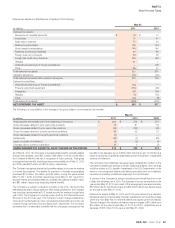

Note17Risk Management and Derivatives

Cash Flow Hedges

The purpose of the Company’s foreign currency hedging activities is to

protect the Company from the risk that the eventual cash fl ows resulting

from transactions in foreign currencies, including revenues, product costs,

selling and administrative expense, investments in U.S. dollar-denominated

available-for-sale debt securities and intercompany transactions, including

intercompany borrowings, will be adversely affected by changes in exchange

rates. It is the Company’s policy to utilize derivatives to reduce foreign exchange

risks where internal netting strategies cannot be effectively employed. Hedged

transactions are denominated primarily in Euros, British Pounds and Japanese

Yen. TheCompany hedges up to 100% of anticipated exposures typically

12months in advance, but has hedged as much as 34months in advance.

All changes in fair values of outstanding cash fl ow hedge derivatives, except

the ineffective portion, are recorded in other comprehensive income until net

income is affected by the variability of cash fl ows of the hedged transaction.

In most cases, amounts recorded in other comprehensive income will be

released to net income some time after the maturity of the related derivative.

The consolidated statement of income classifi cation of effective hedge results

is the same as that of the underlying exposure. Results of hedges of revenue

and product costs are recorded in revenue and cost of sales, respectively, when

the underlying hedged transaction affects net income. Results of hedges of

selling and administrative expense are recorded together with those costs when

the related expense is recorded. Results of hedges of forecasted purchases

of U.S. dollar-denominated available-for-sale securities are recorded in other

(income), net when the securities are sold. Results of hedges of forecasted

intercompany transactions are recorded in other (income), net when the

transaction occurs. The Company classifi es the cash fl ows at settlement from

these designated cash fl ow hedge derivatives in the same category as the

cash fl ows from the related hedged items, generally within the cash provided

by operations component of the cash fl ow statement.

Premiums paid on options are initially recorded as deferred charges.

TheCompany assesses the effectiveness of options based on the total cash

fl ows method and records total changes in the options’ fair value to other

comprehensive income to the degree they are effective.

As of May31,2011, $120million of deferred net losses (net of tax) on both

outstanding and matured derivatives accumulated in other comprehensive

income are expected to be reclassifi ed to net income during the next 12months

as a result of underlying hedged transactions also being recorded in net

income. Actual amounts ultimately reclassifi ed to net income are dependent

on the exchange rates in effect when derivative contracts that are currently

outstanding mature. As of May31,2011, the maximum term over which the

Company is hedging exposures to the variability of cash fl ows for its forecasted

and recorded transactions is 15months.

The Company formally assesses both at a hedge’s inception and on an ongoing

basis, whether the derivatives that are used in the hedging transaction have

been highly effective in offsetting changes in the cash fl ows of hedged items

and whether those derivatives may be expected to remain highly effective

in future periods. Effectiveness for cash fl ow hedges is assessed based on

forward rates. When it is determined that a derivative is not, or has ceased to

be, highly effective as a hedge, the Company discontinues hedge accounting.

The Company discontinues hedge accounting prospectively when (1)it

determines that the derivative is no longer highly effective in offsetting changes

in the cash fl ows of a hedged item (including hedged items such as fi rm

commitments or forecasted transactions); (2)the derivative expires or is

sold, terminated, or exercised; (3)it is no longer probable that the forecasted

transaction will occur; or (4)management determines that designating

thederivative as a hedging instrument is no longer appropriate.

When the Company discontinues hedge accounting because it is no longer

probable that the forecasted transaction will occur in the originally expected

period, but is expected to occur within an additional two-month period of

time thereafter, the gain or loss on the derivative remains in accumulated other

comprehensive income and is reclassifi ed to net income when the forecasted

transaction affects net income. However, if it is probable that a forecasted

transaction will not occur by the end of the originally specifi ed time period or

within an additional two-month period of time thereafter, the gains and losses

that were accumulated in other comprehensive income will be recognized

immediately in net income. In all situations in which hedge accounting is

discontinued and the derivative remains outstanding, the Company will carry

the derivative at its fair value on the balance sheet, recognizing future changes

in the fair value in other (income), net. For the year ended May31,2011 an

immaterial amount of ineffectiveness was recorded to other (income), net.

Fortheyears ended May31,2010 and 2009, the Company recorded in other

(income), net $5million gain and an immaterial amount of ineffectiveness from

cash fl ow hedges, respectively.

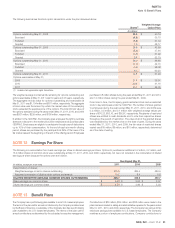

Fair Value Hedges

The Company is also exposed to the risk of changes in the fair value of certain

fi xed-rate debt attributable to changes in interest rates. Derivatives currently

used by the Company to hedge this risk are receive-fi xed, pay-variable

interest rate swaps. As of May31,2011, all interest rate swap agreements are

designated as fair value hedges of the related long-term debt and meet the

shortcut method requirements under the accounting standards for derivatives

and hedging. Accordingly, changes in the fair values of the interest rate swap

agreements are exactly offset by changes in the fair value of the underlying

long-term debt. The cash fl ows associated with the Company’s fair value hedges

are periodic interest payments while the swaps are outstanding, which are

refl ected in net income within the cash provided by operations component of

the cash fl ow statement. No ineffectiveness has been recorded to net income

related to interest rate swaps designated as fair value hedges for theyears

ended May31,2011,2010, and 2009.

In fi scal 2003, the Company entered into a receive-fl oating, pay-fi xed interest

rate swap agreement related to a Japanese Yen denominated intercompany

loan with one of the Company’s Japanese subsidiaries. This interest rate

swap was not designated as a hedge under the accounting standards for

derivatives and hedging.

Accordingly, changes in the fair value of the swap were recorded to net income

each period through maturity as a component of interest expense (income),

net. Both the intercompany loan and the related interest rate swap matured

during the year ended May31,2009.

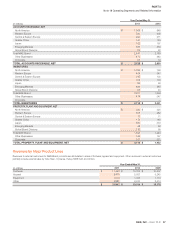

Net Investment Hedges

The Company also hedges the risk of variability in foreign-currency-denominated

net investments in wholly-owned international operations. All changes in

fair value of the derivatives designated as net investment hedges, except

ineffective portions, are reported in the cumulative translation adjustment

component of other comprehensive income along with the foreign currency

translation adjustments on those investments. The Company classifi es the

cash fl ows at settlement of its net investment hedges within the cash used

by investing component of the cash fl ow statement. The Company assesses

hedge effectiveness based on changes in forward rates. The Company

recorded no ineffectiveness from its net investment hedges for theyears

ended May31,2011,2010, and 2009.

Credit Risk

The Company is exposed to credit-related losses in the event of non-performance

by counterparties to hedging instruments. The counterparties to all derivative

transactions are major fi nancial institutions with investment grade credit ratings.

However, this does not eliminate the Company’s exposure to credit risk with

these institutions. This credit risk is limited to the unrealized gains in such

contracts should any of these counterparties fail to perform as contracted.

To manage this risk, the Company has established strict counterparty credit

guidelines that are continually monitored and reported to senior management

according to prescribed guidelines. The Company also utilizes a portfolio of

fi nancial institutions either headquartered or operating in the same countries

the Company conducts its business.

The Company’s derivative contracts contain credit risk related contingent

features aiming to protect against signifi cant deterioration in counterparties’

creditworthiness and their ultimate ability to settle outstanding derivative

contracts in the normal course of business. The Company’s bilateral credit related

contingent features require the owing entity, either the Company or the derivative