Nike 2011 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2011 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

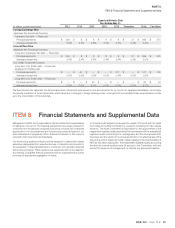

42 NIKE,INC.-Form10-K

PARTII

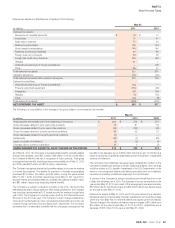

Note1Summary of Signifi cant Accounting Policies

change in the extent or manner in which an asset is used, a signifi cant adverse

change in legal factors or the business climate that could affect the value of

the asset, or a signifi cant decline in the observable market value of an asset,

among others. If such facts indicate a potential impairment, the Company

would assess the recoverability of an asset group by determining if the carrying

value of the asset group exceeds the sum of the projected undiscounted cash

fl ows expected to result from the use and eventual disposition of the assets

over the remaining economic life of the primary asset in the asset group.

Ifthe recoverability test indicates that the carrying value of the asset group is

not recoverable, the Company will estimate the fair value of the asset group

using appropriate valuation methodologies which would typically include an

estimate of discounted cash fl ows. Any impairment would be measured as

the difference between the asset groups carrying amount and its estimated

fair value.

Identifi able Intangible Assets and Goodwill

The Company performs annual impairment tests on goodwill and intangible

assets with indefi nite lives in the fourth quarter of each fi scal year, or when

events occur or circumstances change that would, more likely than not, reduce

the fair value of a reporting unit or an intangible asset with an indefi nite life

below its carrying value. Events or changes in circumstances that may trigger

interim impairment reviews include signifi cant changes in business climate,

operating results, planned investments in the reporting unit, or an expectation

that the carrying amount may not be recoverable, among other factors.

The impairment test requires the Company to estimate the fair value of its

reporting units. If the carrying value of a reporting unit exceeds its fair value,

the goodwill of that reporting unit is potentially impaired and the Company

proceeds to step two of the impairment analysis. In step two of the analysis,

the Company measures and records an impairment loss equal to the excess

of the carrying value of the reporting unit’s goodwill over its implied fair value

should such a circumstance arise.

The Company generally bases its measurement of fair value of a reporting

unit on a blended analysis of the present value of future discounted cash

fl ows and the market valuation approach. The discounted cash fl ows model

indicates the fair value of the reporting unit based on the present value of

the cash fl ows that the Company expects the reporting unit to generate in

the future. TheCompany’s signifi cant estimates in the discounted cash fl ows

model include: its weighted average cost of capital; long-term rate of growth

and profi tability of the reporting unit’s business; and working capital effects.

Themarket valuation approach indicates the fair value of the business based on

a comparison of the reporting unit to comparable publicly traded companies in

similar lines of business. Signifi cant estimates in the market valuation approach

model include identifying similar companies with comparable business factors

such as size, growth, profi tability, risk and return on investment, and assessing

comparable revenue and operating income multiples in estimating the fair

value of the reporting unit.

The Company believes the weighted use of discounted cash fl ows and the

market valuation approach is the best method for determining the fair value of

its reporting units because these are the most common valuation methodologies

used within its industry; and the blended use of both models compensates for

the inherent risks associated with either model if used on a stand-alone basis.

Indefi nite-lived intangible assets primarily consist of acquired trade names and

trademarks. In measuring the fair value for these intangible assets, theCompany

utilizes the relief-from-royalty method. This method assumes that trade names

and trademarks have value to the extent that their owner is relieved of the

obligation to pay royalties for the benefi ts received from them. Thismethod

requires the Company to estimate the future revenue for the related brands,

the appropriate royalty rate and the weighted average cost of capital.

Foreign Currency Translation and Foreign

Currency Transactions

Adjustments resulting from translating foreign functional currency fi nancial

statements into U.S. dollars are included in the foreign currency translation

adjustment, a component of accumulated other comprehensive income in

shareholders’ equity.

The Company’s global subsidiaries have various assets and liabilities, primarily

receivables and payables, that are denominated in currencies other than their

functional currency. These balance sheet items are subject to remeasurement,

the impact of which is recorded in other (income), net, within our consolidated

statement of income.

Accounting for Derivatives and Hedging

Activities

The Company uses derivative fi nancial instruments to limit exposure to

changes in foreign currency exchange rates and interest rates. All derivatives

are recorded at fair value on the balance sheet and changes in the fair value of

derivative fi nancial instruments are either recognized in other comprehensive

income (a component of shareholders’ equity), debt or net income depending

on the nature of the underlying exposure, whether the derivative is formally

designated as a hedge, and, if designated, the extent to which the hedge is

effective. TheCompany classifi es the cash fl ows at settlement from derivatives

in the same category as the cash fl ows from the related hedged items.

Forundesignated hedges and designated cash fl ow hedges, this is within

the cash provided by operations component of the consolidated statements

of cash fl ows. For designated net investment hedges, this is generally within

the cash used by investing activities component of the cash fl ow statement.

Asour fair value hedges are receive-fi xed, pay-variable interest rate swaps,

thecash fl ows associated with these derivative instruments are periodic interest

payments while the swaps are outstanding, which are refl ected in net income

within the cash provided by operations component of the cash fl ow statement.

See Note17— Risk Management and Derivatives for more information on

the Company’s risk management program and derivatives.

Stock-Based Compensation

The Company estimates the fair value of options and stock appreciation rights

granted under the NIKE,Inc. 1990 Stock Incentive Plan (the “1990 Plan”) and

employees’ purchase rights under the Employee Stock Purchase Plans (“ESPPs”)

using the Black-Scholes option pricing model. The Company recognizes this

fair value, net of estimated forfeitures, as selling and administrative expense

in the consolidated statements of income over the vesting period using the

straight-line method.

See Note11— Common Stock and Stock-Based Compensation for more

information on the Company’s stock programs.

Income Taxes

The Company accounts for income taxes using the asset and liability method.

This approach requires the recognition of deferred tax assets and liabilities

for the expected future tax consequences of temporary differences between

the carrying amounts and the tax basis of assets and liabilities. UnitedStates

income taxes are provided currently on fi nancial statement earnings of non-U.S.

subsidiaries that are expected to be repatriated. The Company determines

annually the amount of undistributed non-U.S. earnings to invest indefi nitely

in its non-U.S. operations. The Company recognizes interest and penalties

related to income tax matters in income tax expense.

See Note9— Income Taxes for further discussion.

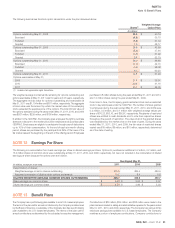

Earnings Per Share

Basic earnings per common share is calculated by dividing net income by

the weighted average number of common shares outstanding during the

year. Diluted earnings per common share is calculated by adjusting weighted

average outstanding shares, assuming conversion of all potentially dilutive

stock options and awards.

See Note12— Earnings Per Share for further discussion.