Proctor and Gamble 2014 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2014 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

The Procter & Gamble Company 41

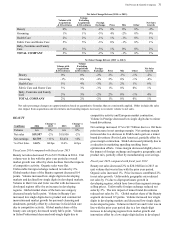

rates consistent with our long-term business plans. Changes

to or a failure to achieve these business plans or a further

deterioration of the macroeconomic conditions could result

in a valuation that would trigger an additional impairment of

the goodwill and intangible assets of these businesses.

The results of our annual goodwill impairment testing during

fiscal 2014 indicated a decline in the fair value of the

Batteries reporting unit due to lower long-term market

growth assumptions in certain key geographies. The

estimated fair value of Batteries continues to exceed its

underlying carrying value, but the fair value cushion has

been reduced to about 5%. As of June 30, 2014, the

Batteries business has goodwill of $2.6 billion and intangible

assets of $2.4 billion. The actual Batteries business results

for the year ended June 30, 2014 were in line with the 2014

projections used in our annual goodwill and intangible asset

impairment testing.

The business unit valuations used to test goodwill and

intangible assets for impairment are dependent on a number

of significant estimates and assumptions, including

macroeconomic conditions, overall category growth rates,

competitive activities, cost containment and margin

expansion and Company business plans. We believe these

estimates and assumptions are reasonable. However, actual

events and results of the Batteries reporting unit could differ

substantially from those used in our valuations. To the

extent such factors result in a further reduction of the level

of projected cash flows used to estimate the Batteries

reporting unit fair value, we may need to record non-cash

impairment charges in the future.

In addition, in the fourth quarter of the year ended June 30,

2014, a key competitor announced its intent to split its

consolidated business into two separate companies during

2015. One of those companies would operate primarily in

the batteries category. While this proposed transaction has

not been consummated, initial independent third party

estimates of the competitor’s stand-alone batteries business

valuation are well below the earnings multiple implied from

the valuation of our batteries business. We attribute the

implied valuation differences to our more favorable business

trends, primarily organic net sales and share growth, along

with scale dis-synergies, general market uncertainty

regarding the capabilities and competitiveness of a stand-

alone company and lack of a control premium. In addition,

the Company conducts a regular portfolio review of its

businesses to assess long-term strategic fit. If our portfolio

review process were to result in a decision to divest the

batteries business, a divestiture could result in a loss that

could be material if potential acquirers utilize valuations

consistent with those indicated above for the key competitor.

See Note 2 to our Consolidated Financial Statements for

additional discussion on goodwill and intangible asset

impairment testing results.

New Accounting Pronouncements

In May 2014, the FASB issued ASU 2014-09, “Revenue

from Contracts with Customers (Topic 606).” This guidance

outlines a single, comprehensive model for accounting for

revenue from contracts with customers. We will adopt the

standard on July 1, 2017. We are evaluating the impact, if

any, that the standard will have on our financial statements.

No other new accounting pronouncement issued or effective

during the fiscal year had or is expected to have a material

impact on the Consolidated Financial Statements.

OTHER INFORMATION

Hedging and Derivative Financial Instruments

As a multinational company with diverse product offerings,

we are exposed to market risks, such as changes in interest

rates, currency exchange rates and commodity prices. We

evaluate exposures on a centralized basis to take advantage

of natural exposure correlation and netting. Except within

financing operations, we leverage the Company's broadly

diversified portfolio of exposures as a natural hedge and

prioritize operational hedging activities over financial

market instruments. To the extent we choose to further

manage volatility associated with the net exposures, we enter

into various financial transactions which we account for

using the applicable accounting guidance for derivative

instruments and hedging activities. These financial

transactions are governed by our policies covering

acceptable counterparty exposure, instrument types and

other hedging practices. Note 5 to the Consolidated

Financial Statements includes a detailed discussion of our

accounting policies for financial instruments.

Derivative positions can be monitored using techniques

including market valuation, sensitivity analysis and value-at-

risk modeling. The tests for interest rate, currency rate and

commodity derivative positions discussed below are based

on the CorporateManager™ value-at-risk model using a one-

year horizon and a 95% confidence level. The model

incorporates the impact of correlation (the degree to which

exposures move together over time) and diversification

(from holding multiple currency, commodity and interest

rate instruments) and assumes that financial returns are

normally distributed. Estimates of volatility and correlations

of market factors are drawn from the RiskMetrics™ dataset

as of June 30, 2014. In cases where data is unavailable in

RiskMetrics™, a reasonable proxy is included.

Our market risk exposures relative to interest rates, currency

rates and commodity prices, as discussed below, have not

changed materially versus the previous reporting period. In

addition, we are not aware of any facts or circumstances that

would significantly impact such exposures in the near term.

Interest Rate Exposure on Financial Instruments. Interest

rate swaps are used to hedge exposures to interest rate

movement on underlying debt obligations. Certain interest

rate swaps denominated in foreign currencies are designated

to hedge exposures to currency exchange rate movements on