Walmart 2010 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2010 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

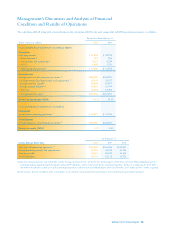

Off Balance Sheet Arrangements

In addition to the unrecorded contractual obligations discussed and

presented above, the company has made certain guarantees as discussed

below for which the timing of payment, if any, is unknown.

In connection with certain debt financing, we could be liable for

early termination payments if certain unlikely events were to occur.

At January 31, 2010, the aggregate termination payment would have

been $109 million. The two arrangements pursuant to which these

payments could be made will expire in fiscal 2011 and fiscal 2019.

In connection with the development of our grocery distribution network

in the United States, we have agreements with third parties which would

require us to purchase or assume the leases on certain unique equipment

in the event the agreements are terminated. These agreements, which

can be terminated by either party at will, cover up to a five-year period

and obligate the company to pay up to approximately $41 million upon

termination of some or all of these agreements.

The company has potential future lease commitments for land and

buildings for approximately 348 future locations. These lease commit-

ments have lease terms ranging from 1 to 40 years and provide for certain

minimum rentals. If executed, payments under operating leases would

increase by $59 million for fiscal 2011, based on current cost estimates.

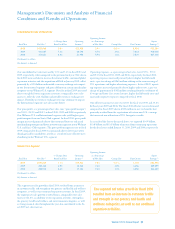

Market Risk

In addition to the risks inherent in our operations, we are exposed to

certain market risks, including changes in interest rates and changes in

currency exchange rates.

The analysis presented for each of our market risk sensitive instruments

is based on a 10% change in interest or currency exchange rates. These

changes are hypothetical scenarios used to calibrate potential risk and do

not represent our view of future market changes. As the hypothetical

figures discussed below indicate, changes in fair value based on the assumed

change in rates generally cannot be extrapolated because the relationship

of the change in assumption to the change in fair value may not be linear.

The effect of a variation in a particular assumption is calculated without

changing any other assumption. In reality, changes in one factor may result

in changes in another, which may magnify or counteract the sensitivities.

At January 31, 2010 and 2009, we had $37.3 billion and $37.2 billion,

respectively, of long-term debt outstanding. Our weighted-average

effective interest rate on long-term debt, after considering the effect

of interest rate swaps, was 4.5% and 4.4% at January 31, 2010 and 2009,

respectively. A hypothetical 10% increase in interest rates in effect at

January 31, 2010 and 2009 would have increased annual interest

expense on borrowings outstanding at those dates by $9 million and

$16 million, respectively.

At January 31, 2010 and 2009, we had $523 million and $1.5 billion,

respectively, of outstanding commercial paper and short-term borrowing

obligations. The weighted-average interest rate, including fees, on these

obligations at January 31, 2010 and 2009 was 1.8% and 0.9%, respectively.

A hypothetical 10% increase in these rates in effect at January 31, 2010 and

2009 would have increased the annual interest expense for the respective

outstanding balances by $1 million.

We enter into interest rate swaps to minimize the risks and costs associated

with financing activities, as well as to maintain an appropriate mix of

fixed- and floating-rate debt. Our preference is to maintain between 40%

and 60% of our debt portfolio, including interest rate swaps, in floating-

rate debt. The swap agreements are contracts to exchange fixed- or

variable-rates for variable- or fixed-interest rate payments periodically

over the life of the instruments. The aggregate fair value of these swaps

represented a gain of $240 million and $304 million at January 31, 2010

and 2009, respectively. A hypothetical increase or decrease of 10% in

interest rates from the level in effect at January 31, 2010, would have

resulted in a loss or gain in value of the swaps of $25 million and

$24 million, respectively. A hypothetical increase or decrease of 10%

in interest rates from the level in effect at January 31, 2009, would

have resulted in a loss or gain in value of the swaps of $17 million.

We hold currency swaps to hedge the currency exchange component of

our net investments in the United Kingdom. In fiscal 2010, we entered

into currency swaps to hedge the currency exchange rate fluctuation

exposure associated with the forecasted payments of principal and interest

of non-U.S. denominated debt. The aggregate fair value of these swaps

at January 31, 2010 and 2009 represented a gain of $475 million and

$526 million, respectively. A hypothetical 10% increase or decrease in

the currency exchange rates underlying these swaps from the market

rate would have resulted in a loss or gain in the value of the swaps of

$58 million and $150 million at January 31, 2010 and January 31, 2009,

respectively. A hypothetical 10% change in interest rates underlying

these swaps from the market rates in effect at January 31, 2010 would

have resulted in a loss or gain in value of the swaps of $11 million and

$30 million, respectively, on the value of the swaps.

In addition to currency swaps, we have designated debt of approximately

£3.0 billion as of January 31, 2010 and 2009, as a hedge of our net

investment in the United Kingdom. At January 31, 2010, a hypothetical

10% increase or decrease in value of the U.S. dollar relative to the British

pound would have resulted in a gain or loss in the value of the debt of

$480 million. At January 31, 2009, a hypothetical 10% increase or decrease

in value of the U.S. dollar relative to the British pound would have

resulted in a gain or loss in the value of the debt of $440 million. In

addition, we have designated debt of approximately ¥437.4 billion as of

January 31, 2010 and 2009, as a hedge of our net investment in Japan.

At January 31, 2010, a hypothetical 10% increase or decrease in value

of the U.S. dollar relative to the Japanese yen would have resulted in a

gain or loss in the value of the debt of $485 million. At January 31, 2009,

a hypothetical 10% increase or decrease in value of the U.S. dollar rela-

tive to the Japanese yen would have resulted in a gain or loss in the value

of the debt of $443 million.

Management’s Discussion and Analysis of Financial

Condition and Results of Operations

26 Walmart 2010 Annual Report