Walmart 2015 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2015 Walmart annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

|

|

50 2015 Annual Report

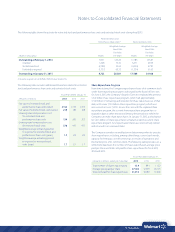

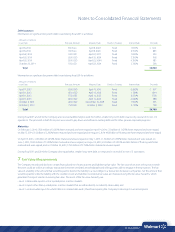

Recurring Fair Value Measurements

The Company holds derivative instruments that are required to be measured at fair value on a recurring basis. The fair values are the estimated

amounts the Company would receive or pay upon termination of the related derivative agreements as of the reporting dates. The fair values have

been measured using the income approach and Level 2 inputs, which include the relevant interest rate and foreign currency forward curves.

As of January 31, 2015 and 2014, the notional amounts and fair values of these derivatives were as follows:

January 31, 2015 January 31, 2014

(Amounts in millions) Notional Amount Fair Value Notional Amount Fair Value

Receive fixed-rate, pay variable-rate interest rate swaps

designated as fair value hedges $ 500 $ 12 $1,000 $ 5

Receive fixed-rate, pay fixed-rate cross-currency interest rate swaps

designated as net investment hedges 1,250 207 1,250 97

Receive fixed-rate, pay fixed-rate cross-currency interest rate swaps

designated as cash flow hedges 4,329 (317) 3,004 453

Receive variable-rate, pay fixed-rate interest rate swaps

designated as cash flow hedges 255 (1) 457 (2)

Receive variable-rate, pay fixed-rate forward starting interest rate swaps

designated as cash flow hedges — — 2,500 166

Total $6,334 $ (99) $8,211 $719

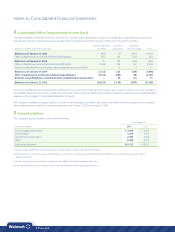

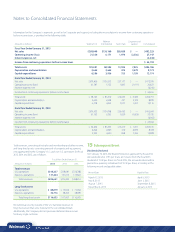

Nonrecurring Fair Value Measurements

In addition to assets and liabilities that are recorded at fair value on a recurring basis, the Company’s assets and liabilities are also subject to

nonrecurring fair value measurements. Generally, assets are recorded at fair value on a nonrecurring basis as a result of impairment charges.

The Company did not record any significant impairment charges to assets measured at fair value on a nonrecurring basis during the fiscal years

ended January 31, 2015, or 2014.

Other Fair Value Disclosures

The Company records cash and cash equivalents and short-term borrowings at cost. The carrying values of these instruments approximate their

fair value due to their short-term maturities.

The Company’s long-term debt is also recorded at cost. The fair value is estimated using Level 2 inputs based on the Company’s current incremental

borrowing rate for similar types of borrowing arrangements. The carrying value and fair value of the Company’s long-term debt as of January 31, 2015

and 2014, are as follows:

January 31, 2015 January 31, 2014

(Amounts in millions) Carrying Value Fair Value Carrying Value Fair Value

Long-term debt, including amounts due within one year $45,896 $56,237 $45,874 $50,757

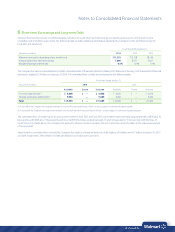

8 Derivative Financial Instruments

The Company uses derivative financial instruments for hedging and

non-trading purposes to manage its exposure to changes in interest and

currency exchange rates, as well as to maintain an appropriate mix of

fixed- and variable-rate debt. Use of derivative financial instruments in

hedging programs subjects the Company to certain risks, such as market

and credit risks. Market risk represents the possibility that the value of the

derivative financial instrument will change. In a hedging relationship, the

change in the value of the derivative financial instrument is offset to a

great extent by the change in the value of the underlying hedged item.

Credit risk related to a derivative financial instrument represents the pos-

sibility that the counterparty will not fulfill the terms of the contract. The

notional, or contractual, amount of the Company’s derivative financial

instruments is used to measure interest to be paid or received and does

not represent the Company’s exposure due to credit risk. Credit risk is

monitored through established approval procedures, including setting

concentration limits by counterparty, reviewing credit ratings and requiring

collateral (generally cash) from the counterparty when appropriate.

The Company only enters into derivative transactions with counterparties

rated “A-” or better by nationally recognized credit rating agencies.

Subsequent to entering into derivative transactions, the Company regu-

larly monitors the credit ratings of its counterparties. In connection with

various derivative agreements, including master netting arrangements,

the Company held cash collateral from counterparties of $323 million

and $641 million at January 31, 2015 and January 31, 2014, respectively.

The Company records cash collateral received as amounts due to the

counterparties exclusive of any derivative asset. Furthermore, as part

of the master netting arrangements with these counterparties, the

Company is also required to post collateral if the Company’s net

derivative liability position exceeds $150 million with any counterparty.

The Company did not have any cash collateral posted with counterparties

at January 31, 2015 or January 31, 2014. The Company records cash

collateral it posts with counterparties as amounts receivable from those

counterparties exclusive of any derivative liability.

Notes to Consolidated Financial Statements