America Online 2015 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2015 America Online annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

Other, net

The change in Other, net financing activities during 2013 was primarily

driven by higher distributions to Vodafone, which owned a 45% non-

controlling interest in Verizon Wireless as of December31, 2013.

Credit Facility

As of December31, 2015, the unused borrowing capacity under our

$8.0billion four-year credit facility was approximately $7.9billion. The

credit facility does not require us to comply with financial covenants

or maintain specified credit ratings, and it permits us to borrow even

if our business has incurred a material adverse change. We use the

credit facility for the issuance of letters of credit and for general

corporate purposes.

Common Stock

Common stock has been used from time to time to satisfy some

of the funding requirements of employee and shareholder plans,

including 22.6million, 18.2million and 6.9million common shares

issued from Treasury stock during 2015, 2014 and 2013, respectively,

which had aggregate values of $0.9billion, $0.7billion and $0.3billion,

respectively.

In February 2015, the Verizon Board of Directors authorized Verizon to

enter into an accelerated share repurchase (ASR) agreement to repur-

chase $5.0billion of the Company’s common stock. On February10,

2015, in exchange for an upfront payment totaling $5.0billion, Verizon

received an initial delivery of 86.2million shares having a value of

approximately $4.25billion. On June5, 2015, Verizon received an addi-

tional 15.4million shares as final settlement of the transaction under

the ASR agreement. In total, 101.6million shares were delivered under

the ASR at an average repurchase price of $49.21.

On March7, 2014, the Verizon Board of Directors approved a share

buyback program, which authorizes the repurchase of up to 100million

shares of Verizon common stock terminating no later than the close of

business on February28, 2017. The program permits Verizon to repur-

chase shares over time, with the amount and timing of repurchases

depending on market conditions and corporate needs. The Board also

determined that no additional shares were to be purchased under the

prior program. During 2015, we repurchased $0.1billion of our common

stock as part of our previously announced share buyback program.

There were no repurchases of common stock during 2014. During

2013, we repurchased $0.2billion of our common stock under our

previous share buyback program.

As a result of the Wireless Transaction, in February 2014, Verizon

issued approximately 1.27billion shares.

Credit Ratings

Verizon’s credit ratings did not change in 2015 or 2014.

During the third quarter of 2013, Verizon’s credit ratings were down-

graded by Moody’s Investors Service (Moody’s), Standard & Poor’s

Ratings Services (Standard & Poor’s) and Fitch Ratings (Fitch) as

a result of Verizon’s announcement of the agreement to acquire

Vodafone’s 45% noncontrolling interest in Verizon Wireless for

approximately $130billion including the incurrence of third-party

indebtedness to fund the cash portion of the purchase price for the

Wireless Transaction. Moody’s downgraded Verizon’s long-term debt

ratings one notch from A3 to Baa1, while Standard & Poor’s lowered

its corporate credit rating and senior unsecured debt rating one notch

from A- to BBB+ and Fitch lowered its long-term issuer default rating

and senior unsecured debt rating one notch from A to A-.

Securities ratings assigned by rating organizations are expressions of

opinion and are not recommendations to buy, sell or hold securities. A

securities rating is subject to revision or withdrawal at any time by the

assigning rating organization. Each rating should be evaluated inde-

pendently of any other rating.

Covenants

Our credit agreements contain covenants that are typical for large,

investment grade companies. These covenants include requirements

to pay interest and principal in a timely fashion, pay taxes, maintain

insurance with responsible and reputable insurance companies,

preserve our corporate existence, keep appropriate books and

records of financial transactions, maintain our properties, provide

financial and other reports to our lenders, limit pledging and dispo-

sition of assets and mergers and consolidations, and other similar

covenants. Additionally, our term loan credit agreement requires us to

maintain a leverage ratio (as such term is defined in those agreements)

not in excess of 3.50:1.00 until our credit ratings are equal to or higher

than A3 and A-. See Note7 to the consolidated financial statements for

additional details related to our term loan credit agreement.

We and our consolidated subsidiaries are in compliance with all of our

financial and restrictive covenants.

Increase (Decrease) In Cash and Cash Equivalents

Our Cash and cash equivalents at December31, 2015 totaled

$4.5billion, a $6.1billion decrease compared to Cash and cash

equivalents at December31, 2014 primarily as a result of the factors

discussed above. Our Cash and cash equivalents at December31,

2014 totaled $10.6billion, a $42.9billion decrease compared to Cash

and cash equivalents at December31, 2013 primarily as a result of

the cash payment made to Vodafone as part of the completion of the

Wireless Transaction.

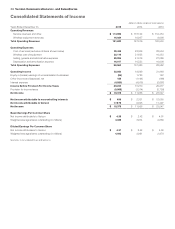

Free Cash Flow

Free cash flow is a non-GAAP financial measure that management

believes is useful to investors and other users of Verizon’s financial

information in evaluating cash available to pay debt and dividends.

Free cash flow is calculated by subtracting capital expenditures from

net cash provided by operating activities. The following table recon-

ciles net cash provided by operating activities to Free cash flow:

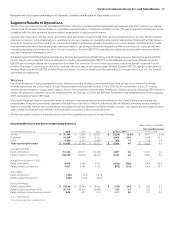

(dollars in millions)

Years Ended December31, 2015 2014 2013

Net cash provided by operating

activities $ 38,930 $ 30,631 $ 38,818

Less Capital expenditures

(including capitalized software) 17,775 17,191 16,604

Free cash ow $ 21,155 $ 13,440 $ 22,214

The changes in free cash flow during 2015, 2014 and 2013 were a

result of the factors described in connection with net cash provided by

operating activities and capital expenditures. During 2015, we received

$5.9billion of cash proceeds, net of remittances, related to the sale of

wireless device installment receivables as well as $2.4billion of cash

proceeds received related to the Tower Monetization Transaction

attributable to the portion of the towers for which the right-of-use has

passed to the tower operator. On February21, 2014, we completed the

Wireless Transaction which provides full access to the cash flows of

Verizon Wireless. The completion of the Wireless Transaction resulted

in an increase in income tax payments as well as an increase in interest

payments, which reduced our net cash provided by operating activities

during 2014 (see “Cash Flows Provided by Operating Activities”).

29Verizon Communications Inc. and Subsidiaries

Management’s Discussion and Analysis ofFinancialCondition and Results of Operations continued